Cost accounting, a vital discipline within the broader field of accounting, focuses on identifying, measuring, analyzing, accumulating, allocating, and controlling costs. Unlike financial accounting, which is geared towards external stakeholders like investors and creditors, cost accounting is primarily for internal management use. Its core purpose is to provide detailed cost information that helps businesses make informed decisions, improve efficiency, and enhance profitability. This internal focus allows for a more granular examination of expenses, tracing them back to specific products, services, departments, or projects.

The insights derived from cost accounting are instrumental in strategic planning, operational control, and performance evaluation. By understanding the true cost of operations, businesses can set appropriate prices, manage inventory effectively, identify areas of waste, and make strategic choices about resource allocation. In essence, cost accounting bridges the gap between financial reporting and the operational realities of a business, providing the data necessary for informed management action.

The Fundamental Principles of Cost Accounting

At its heart, cost accounting is about understanding where money is spent and what value is derived from that expenditure. This involves a systematic approach to classifying, recording, and analyzing costs. The principles are designed to provide clarity and accuracy, enabling management to gain a comprehensive view of the economic implications of their decisions.

Cost Classification

A fundamental aspect of cost accounting is the classification of costs. This allows for a more nuanced understanding of how different types of expenses behave and impact the business. Common classifications include:

Direct vs. Indirect Costs

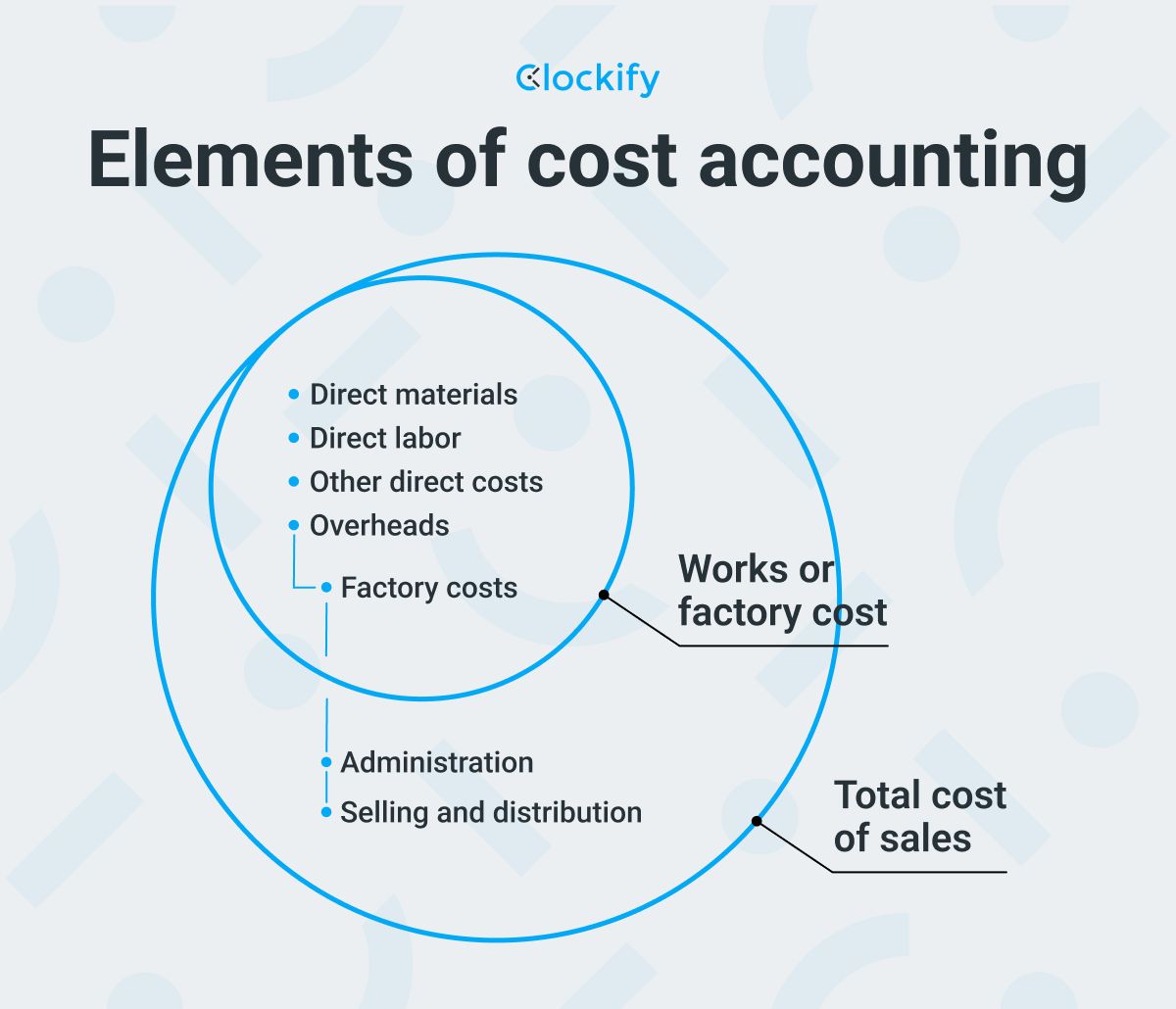

- Direct Costs: These are costs that can be easily and directly traced to a specific cost object, such as a product, service, or project. For a manufacturing company, direct material costs (e.g., the wood used to make a table) and direct labor costs (e.g., the wages of the carpenter assembling the table) are prime examples.

- Indirect Costs (Overhead): These are costs that cannot be directly traced to a specific cost object and are incurred for the benefit of multiple cost objects. Examples include factory rent, utilities, depreciation of machinery, and the salaries of factory supervisors. Indirect costs are often allocated to cost objects using predetermined overhead rates.

Fixed vs. Variable Costs

- Fixed Costs: These costs remain constant in total amount over a relevant range of activity, regardless of the volume of production or sales. Examples include rent, salaries of administrative staff, and insurance premiums. While the total fixed cost remains the same, the fixed cost per unit decreases as production volume increases.

- Variable Costs: These costs change in total amount in direct proportion to the volume of activity. Examples include direct materials, direct labor (if paid per unit produced), and sales commissions. The variable cost per unit remains constant, while the total variable cost increases with higher production volumes.

Product vs. Period Costs

- Product Costs: These are costs that are directly associated with the production of goods. They are included in the cost of inventory and are recognized as an expense (Cost of Goods Sold) only when the product is sold. Product costs include direct materials, direct labor, and manufacturing overhead.

- Period Costs: These are costs that are not directly associated with the production of goods and are expensed in the period in which they are incurred. They are not inventoried. Examples include selling expenses (e.g., advertising, sales salaries) and administrative expenses (e.g., office rent, accounting salaries).

Cost Accumulation Methods

Once costs are classified, they need to be accumulated in a way that allows for their traceability and allocation to cost objects. Various methods are employed depending on the nature of the business and its operations.

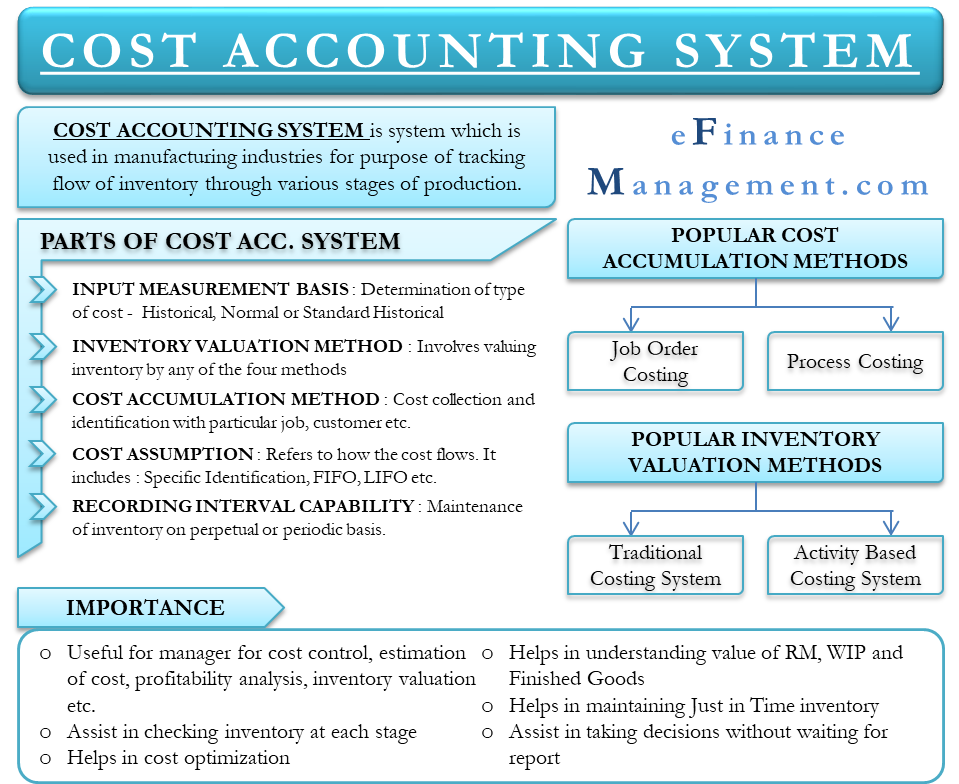

Job Costing

Job costing is used when products or services are unique or produced in distinct batches. Costs are accumulated for each individual job or project. This method is common in industries like construction, custom manufacturing, and professional services where each undertaking has its own specific requirements and associated costs.

Process Costing

Process costing is applied when identical or similar products are manufactured in a continuous flow through a series of production processes. Costs are accumulated for each department or process over a specific period and then averaged over the units produced. This method is typically used in industries like chemicals, food processing, and petroleum refining.

Cost Allocation

Cost allocation is the process of assigning indirect costs (overhead) to cost objects. Since indirect costs cannot be directly traced, a systematic and rational basis for allocation is required.

Allocation Bases

The selection of an appropriate allocation base is crucial for accurate cost allocation. Common allocation bases include direct labor hours, direct labor costs, machine hours, or a predetermined overhead rate. The goal is to choose a base that has a strong causal relationship with the incurrence of the overhead costs.

Predetermined Overhead Rates

In manufacturing environments, it is often impractical to allocate actual overhead costs to products as they are incurred. Instead, predetermined overhead rates are used. These rates are calculated at the beginning of an accounting period by dividing the estimated total manufacturing overhead by an estimated total allocation base (e.g., estimated direct labor hours). This allows for more timely cost assignment to products throughout the period.

Key Objectives and Applications of Cost Accounting

The overarching goal of cost accounting is to support effective management decision-making. This translates into several critical objectives that drive the application of its principles and techniques.

Product and Service Costing

One of the most fundamental applications of cost accounting is determining the cost of producing individual products or delivering specific services. This information is vital for:

Pricing Decisions

Knowing the precise cost of a product or service allows management to set prices that ensure profitability. A thorough understanding of direct and indirect costs, along with desired profit margins, forms the basis for competitive yet sustainable pricing strategies.

Profitability Analysis

By calculating the cost of goods sold and comparing it with revenue, companies can assess the profitability of individual products, product lines, or customer segments. This helps in identifying high-margin offerings and areas that may require improvement or discontinuation.

Inventory Valuation

Cost accounting plays a critical role in valuing inventory for financial reporting purposes. Product costs accumulated through cost accounting methods are used to determine the cost of raw materials, work-in-progress, and finished goods. This directly impacts the balance sheet and the cost of goods sold reported on the income statement.

Budgeting and Planning

Cost accounting data provides the foundation for creating accurate budgets. By analyzing historical cost patterns and forecasting future activity levels, businesses can develop realistic budgets for production, labor, and overhead. This facilitates financial planning and resource allocation.

Performance Measurement and Control

Cost accounting systems provide the data needed to monitor performance and control costs. By comparing actual costs to budgeted costs or standard costs, management can identify variances and investigate their causes. This enables prompt corrective action to be taken, improving operational efficiency and cost containment.

Decision Making

Cost accounting provides essential information for a wide range of strategic and operational decisions, including:

Make-or-Buy Decisions

When a company needs a component or service, cost accounting helps determine whether it is more cost-effective to produce it internally or purchase it from an external supplier. This involves comparing the relevant costs of each alternative.

Special Order Decisions

If a customer requests a special order at a price below the normal selling price, cost accounting analysis can help determine if accepting the order would be profitable, considering only the incremental costs involved.

Product Mix Decisions

For companies with multiple products, cost accounting data can help in determining the optimal mix of products to offer to maximize profitability, especially when faced with constraints such as limited machine capacity or labor hours.

Advanced Cost Accounting Techniques

Beyond the fundamental principles, cost accounting employs more sophisticated techniques to provide deeper insights and support complex decision-making in modern business environments.

Activity-Based Costing (ABC)

Activity-based costing is a more sophisticated method of allocating overhead costs. Instead of using a single plant-wide overhead rate or departmental rates based on volume, ABC identifies specific activities that drive costs and assigns overhead to cost objects based on their consumption of these activities. This approach generally leads to more accurate product costs, especially in companies with a diverse range of products and complex overhead structures. ABC recognizes that indirect costs are not solely driven by production volume but by a multitude of activities.

Standard Costing

Standard costing involves setting predetermined or “standard” costs for materials, labor, and overhead for each unit of output. Actual costs are then compared to these standard costs, and any differences are analyzed as variances. This system helps in:

- Cost Control: By highlighting deviations from expected costs.

- Performance Evaluation: Measuring the efficiency of operations.

- Simplified Record-Keeping: Facilitating product costing and inventory valuation.

- Budgeting: Providing a basis for setting performance targets.

Cost-Volume-Profit (CVP) Analysis

CVP analysis, also known as break-even analysis, examines the relationships between costs, sales volume, and profit. It helps businesses understand:

- Break-Even Point: The level of sales volume at which total revenue equals total costs, resulting in zero profit.

- Target Profit Analysis: The sales volume required to achieve a specific profit target.

- Margin of Safety: The difference between actual or planned sales and the break-even sales, indicating the extent to which sales can decline before losses occur.

- Impact of Cost Structure: How changes in fixed and variable costs affect profitability.

Lean Accounting

Lean accounting is an approach that adapts cost accounting principles to organizations that have adopted lean manufacturing principles. It aims to simplify cost accounting by focusing on value streams rather than traditional departments and by reducing the emphasis on complex cost allocations. The goal is to provide timely and relevant financial information that supports continuous improvement and waste reduction, aligning financial metrics with operational goals.

The Strategic Importance of Cost Accounting

In today’s competitive business landscape, effective cost accounting is no longer a mere compliance exercise; it is a strategic imperative. Businesses that master their cost structures are better positioned to navigate market fluctuations, innovate, and achieve sustainable growth.

Driving Efficiency and Profitability

By providing granular insights into costs, cost accounting empowers management to identify inefficiencies, eliminate waste, and optimize resource utilization. This direct impact on operational efficiency translates into improved profitability and a stronger competitive advantage.

Supporting Informed Decision-Making

The data generated by cost accounting systems is the bedrock of sound business decision-making. From pricing strategies to investment decisions, a clear understanding of costs ensures that choices are grounded in economic reality, leading to more predictable and favorable outcomes.

Fostering a Cost-Conscious Culture

When cost accounting information is effectively communicated throughout an organization, it can foster a culture of cost-consciousness. Employees at all levels can gain a better understanding of how their actions impact the company’s bottom line, encouraging responsible resource management and innovation in cost reduction.

In conclusion, cost accounting is an indispensable tool for any business seeking to understand its financial performance, manage its operations effectively, and make strategic decisions that drive long-term success. Its principles and techniques provide the clarity needed to transform raw data into actionable insights, making it a cornerstone of effective management.