Understanding your home’s equity can unlock significant financial opportunities. When you’ve built up substantial equity in your property, you have access to two primary ways to leverage it: a Home Equity Line of Credit (HELOC) and a Home Equity Loan. While both tap into your home’s value, they function differently and are suited for distinct financial needs. Deciding between a HELOC and a home equity loan hinges on your borrowing needs, repayment preferences, and risk tolerance.

Understanding Home Equity

Before diving into the specifics of HELOCs and home equity loans, it’s crucial to grasp the concept of home equity. Your home equity is the difference between your home’s current market value and the outstanding balance on your mortgage. For instance, if your home is appraised at $400,000 and you owe $200,000 on your mortgage, you have $200,000 in home equity. Lenders allow you to borrow against this equity, effectively converting a portion of your home’s value into accessible cash. This is often referred to as borrowing “against your home” or “tapping into your equity.”

The amount you can borrow is typically determined by your Loan-to-Value (LTV) ratio. Lenders generally allow you to borrow up to a certain percentage of your home’s value, often around 80% to 85%, including your existing mortgage. So, in our example, if a lender offers an 80% LTV, you could potentially borrow up to $320,000 (80% of $400,000). After accounting for your existing $200,000 mortgage, you would have $120,000 of available equity to borrow against.

Home Equity Loans: A Lump Sum Approach

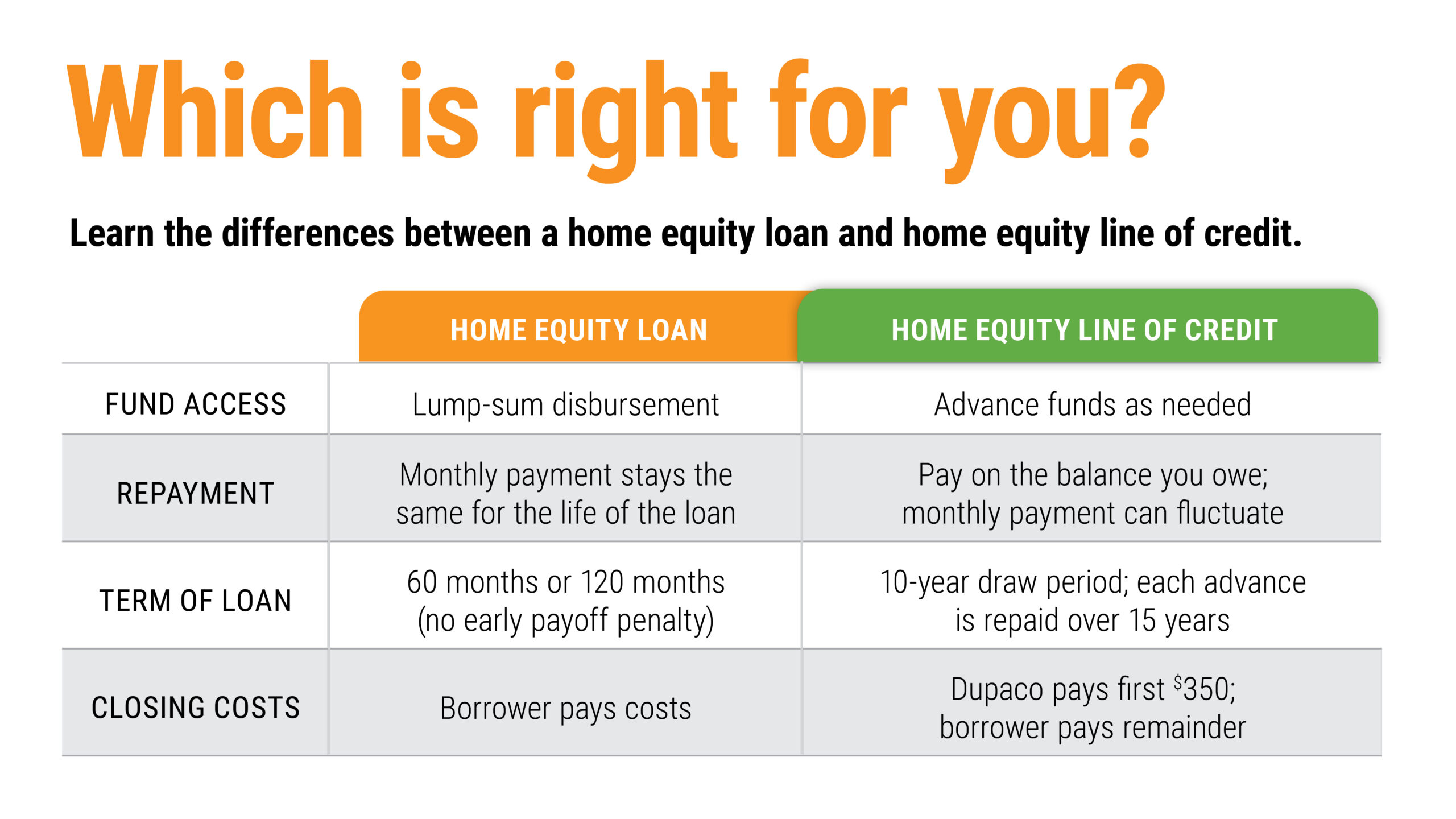

A home equity loan, often called a “second mortgage,” provides a lump sum of cash that you receive upfront. This fixed amount is then repaid over a set period, typically 5 to 30 years, with a fixed interest rate.

How It Works

- Application and Approval: You apply for a home equity loan with a lender, similar to a traditional mortgage. The lender will assess your creditworthiness, income, and the equity in your home.

- Lump Sum Disbursement: Upon approval, you receive the entire loan amount in a single disbursement.

- Fixed Repayments: You begin making regular monthly payments that include both principal and interest. Because the interest rate is fixed, your monthly payments remain consistent throughout the loan’s term, making budgeting easier.

- Fixed Term: The loan has a predetermined repayment schedule. Once you’ve made all the payments, the loan is fully repaid.

Pros of Home Equity Loans

- Predictable Payments: The fixed interest rate means your monthly payments are consistent, simplifying budgeting and financial planning. This is particularly beneficial in a rising interest rate environment, as your payments won’t increase.

- Large, Single Sum: Ideal for large, one-time expenses where you know the exact cost, such as a major home renovation, consolidating high-interest debt, or covering significant medical bills.

- Simplicity: The structure of a home equity loan is straightforward. You borrow a set amount, repay it over time with fixed payments.

Cons of Home Equity Loans

- Less Flexibility: Once you receive the lump sum, you cannot borrow more funds without reapplying. If your initial estimate for a project was too low, you’d need to seek additional financing.

- Higher Initial Interest Rates (Potentially): While fixed, the interest rate on a home equity loan might sometimes be slightly higher than the initial rates offered on a HELOC.

- Immediate Repayment Obligation: You begin repaying the entire borrowed amount immediately, including principal and interest, from the moment you receive the funds.

When to Choose a Home Equity Loan

A home equity loan is an excellent choice when you:

- Have a specific, large expense with a known cost.

- Prefer predictable, fixed monthly payments.

- Want to consolidate debt into a single, manageable payment.

- Are looking for a straightforward borrowing and repayment structure.

Home Equity Lines of Credit (HELOCs): A Flexible Revolving Credit

A HELOC functions more like a credit card secured by your home equity. It provides access to a revolving credit line that you can draw from as needed over a specific period, often called the “draw period.”

How It Works

- Establishing a Credit Line: You apply for a HELOC, and upon approval, the lender sets a maximum credit limit based on your home’s equity and your financial qualifications.

- Draw Period: During this initial phase (typically 5-10 years), you can borrow funds up to your credit limit. You only pay interest on the amount you actually draw.

- Repayment Period: After the draw period ends, you enter the repayment period (also typically 5-20 years). During this phase, you can no longer draw funds, and you must repay the outstanding principal balance plus interest. Payments during this period usually consist of both principal and interest, amortizing the remaining balance over the loan term.

- Interest Rate Fluctuations: Most HELOCs have variable interest rates, meaning your monthly payments can change as market interest rates fluctuate.

Pros of HELOCs

- Flexibility: The revolving nature of a HELOC allows you to borrow, repay, and re-borrow funds as needed up to your credit limit during the draw period. This is ideal for ongoing projects or unexpected expenses that may arise over time.

- Interest Paid Only on What You Use: You only accrue and pay interest on the amount you’ve actually borrowed, not the entire credit line. This can be more cost-effective if you don’t need all the funds at once or if you plan to repay portions of the loan and re-borrow later.

- Potential for Lower Initial Rates: HELOCs often start with introductory or variable rates that may be lower than fixed rates offered on home equity loans, especially in a declining interest rate environment.

Cons of HELOCs

- Variable Interest Rates: The primary drawback is the variable interest rate. If interest rates rise, your monthly payments will increase, potentially making budgeting more challenging and increasing the overall cost of borrowing.

- Payment Shock: At the end of the draw period, when you transition to the repayment period, your payments will likely increase significantly as you begin to repay the principal in addition to interest.

- Complexity: The two-stage nature (draw and repayment periods) and variable rates can make HELOCs seem more complex than home equity loans.

When to Choose a HELOC

A HELOC is a suitable option when you:

- Are undertaking a home improvement project that will take time and may have costs that emerge incrementally.

- Need ongoing access to funds for unpredictable expenses.

- Are comfortable with potentially fluctuating monthly payments.

- Want to pay interest only on the funds you actively use.

- Are confident in your ability to manage variable interest rates and future payment increases.

Key Differences Summarized

| Feature | Home Equity Loan | HELOC (Home Equity Line of Credit) |

|---|---|---|

| Disbursement | Lump sum received upfront | Revolving line of credit; draw as needed |

| Interest Rate | Typically fixed | Typically variable |

| Repayment | Amortized payments (principal + interest) from start | Interest-only payments during draw period; P+I during repayment |

| Flexibility | Limited; no re-borrowing after disbursement | High; can borrow, repay, and re-borrow during draw period |

| Payment Predictability | High | Lower (due to variable rates) |

| Best For | Large, one-time expenses; debt consolidation | Ongoing projects; unpredictable expenses; flexible access |

| Risk | Lower risk of payment increases | Higher risk of payment increases if rates rise |

Making the Right Choice for Your Financial Goals

The decision between a HELOC and a home equity loan is not a one-size-fits-all answer. It requires careful consideration of your specific financial situation and future needs.

Assess Your Spending Needs

- Do you have a single, large expense with a defined cost? A home equity loan might be the simpler and more predictable choice. For example, if you’re buying a car for $30,000 or planning a $50,000 kitchen remodel with a clear budget, a home equity loan provides the full amount upfront.

- Do you have an ongoing project or anticipate multiple expenses over time? A HELOC offers the flexibility to draw funds as needed, potentially saving you money on interest if you don’t use the entire line of credit at once. This is ideal for major home renovations that might stretch over a year or for funding a business that requires fluctuating capital.

Evaluate Your Comfort with Risk and Predictability

- Do you prioritize stable, predictable monthly payments? A home equity loan with its fixed rate offers this peace of mind, making budgeting straightforward. This is especially important if your income is fixed or you have other financial obligations that require a consistent outlay.

- Are you comfortable with potential payment fluctuations? A HELOC’s variable rate means your payments could go up or down. If you have a strong financial buffer and are confident in managing potential increases, a HELOC might still be attractive for its flexibility.

Consider the Interest Rate Environment

- If interest rates are low and expected to rise: A fixed-rate home equity loan can lock in a favorable rate for the life of the loan, protecting you from future increases.

- If interest rates are high and expected to fall: A variable-rate HELOC might offer a lower initial rate, and if rates decrease, your payments could eventually go down. However, this comes with the risk that rates could also rise.

Understand the Repayment Structure

- Home Equity Loan: You’ll start paying back principal and interest from the first payment. This means you’ll own more of your home faster, but your initial monthly payments will be higher.

- HELOC: During the draw period, you might only pay interest. This results in lower initial payments, but you won’t be reducing your principal balance, and you’ll still owe the full amount at the end of the draw period, leading to higher payments during the repayment phase.

Ultimately, both HELOCs and home equity loans are powerful tools for leveraging your home’s equity. By understanding their distinct mechanisms, benefits, and drawbacks, you can make an informed decision that aligns with your financial goals and provides the most advantageous path forward. Consulting with a financial advisor can also offer personalized guidance tailored to your unique circumstances.