The world of auto insurance can often feel like navigating a complex maze. Amidst terms like premiums, comprehensive coverage, and collision, the concept of a “deductible” frequently arises. Understanding what this means is crucial for any vehicle owner, as it directly impacts your financial responsibility in the event of a claim. In essence, your auto insurance deductible is the amount of money you agree to pay out-of-pocket before your insurance company begins to cover the remaining costs of a covered loss. It’s a fundamental component of your insurance policy, acting as a shared risk between you and your insurer.

The Mechanics of the Deductible

When you file a claim for damage to your vehicle, whether it’s due to a collision, theft, or another covered event, the deductible comes into play. Imagine you have a fender bender that results in $5,000 worth of damage. If your insurance policy has a $500 deductible, you will be responsible for paying that initial $500. Your insurance company will then cover the remaining $4,500. This arrangement is designed to provide a balance. The insurer assumes the bulk of the financial burden for significant losses, while you contribute a smaller, predetermined amount.

Types of Deductibles

It’s important to recognize that not all deductibles are created equal. The type of deductible you have often depends on the type of coverage. The most common types are associated with collision and comprehensive insurance.

Collision Deductible

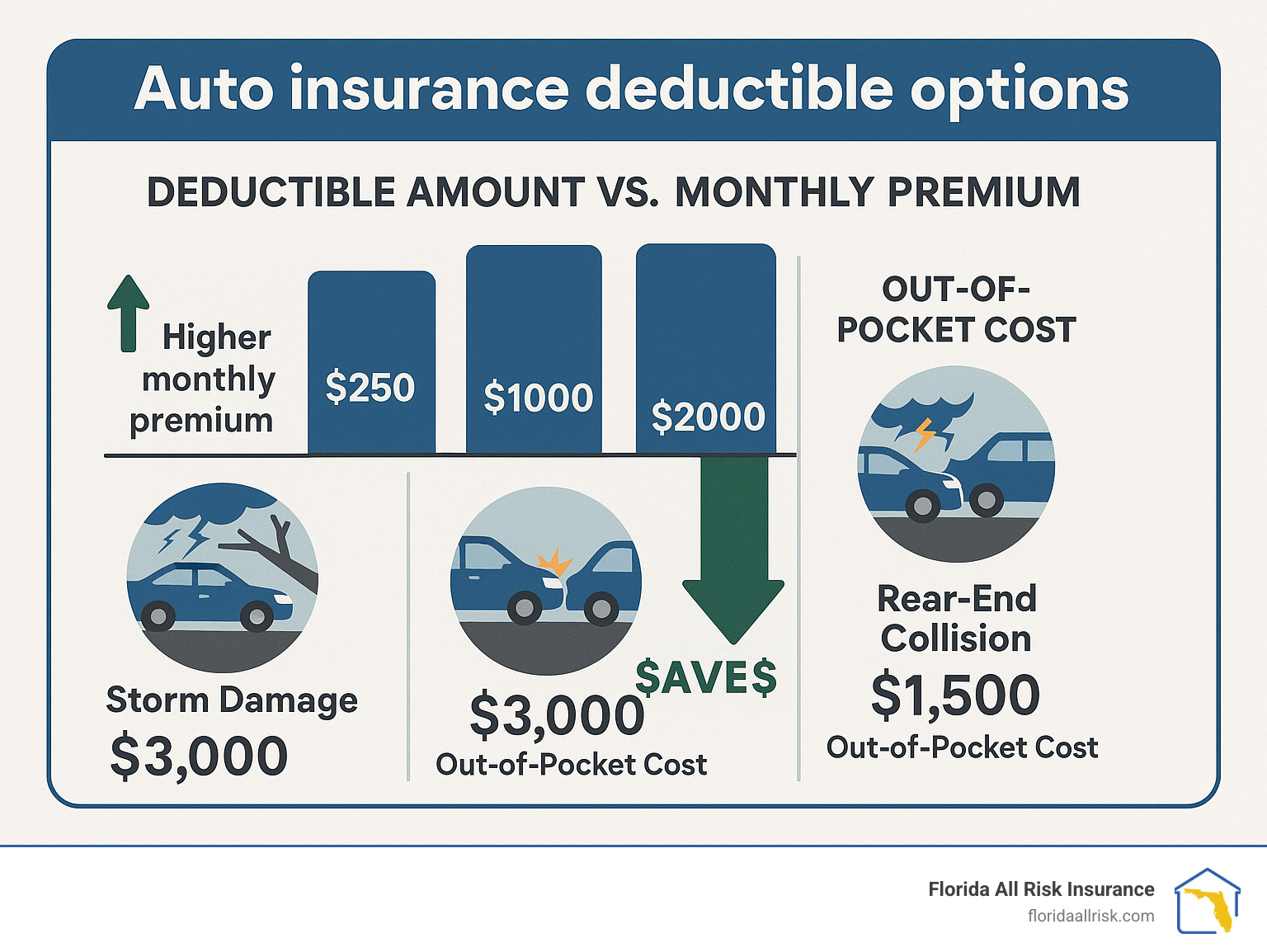

This deductible applies specifically when your vehicle is damaged in a collision, regardless of who is at fault. This could include accidents with other vehicles, objects, or even single-vehicle accidents where you hit a stationary object like a tree or a guardrail. The amount you choose for your collision deductible will directly influence your premium. A higher deductible generally leads to a lower premium, and vice versa.

Comprehensive Deductible

Comprehensive coverage, often referred to as “other than collision,” covers damages to your vehicle that are not caused by a collision. This can include a wide range of events such as theft, vandalism, fire, natural disasters (hail, flood, windstorm), falling objects, or hitting an animal. Similar to the collision deductible, your comprehensive deductible is the amount you pay before the insurer covers the rest of the costs. Again, a higher comprehensive deductible will typically result in a lower premium.

Separate Deductibles for Different Coverages

A key point to understand is that you can, and often do, have separate deductibles for collision and comprehensive coverage. For instance, you might have a $1,000 deductible for collision and a $500 deductible for comprehensive. This means if your car is stolen and recovered with $3,000 worth of damage, you would pay $500, and the insurer would cover $2,500. If you were to be involved in a collision resulting in $10,000 worth of damage, you would pay $1,000, and the insurer would cover $9,000. It’s crucial to review your policy documents carefully to understand the specific deductible amounts for each coverage type you have.

Choosing Your Deductible: A Balancing Act

The decision of how much to set your deductible at is a significant one, and it involves a careful assessment of your financial situation and risk tolerance. There’s no universally “right” answer, as it depends on individual circumstances.

The Impact of Deductible on Premiums

As mentioned, there’s an inverse relationship between your deductible and your insurance premium. Insurers view higher deductibles as a sign of lower risk for them. If you’re willing to absorb more of the initial cost of a claim, they are less likely to have to pay out on smaller claims, making your policy less of a financial liability for them. Consequently, policies with higher deductibles generally come with lower annual or monthly premiums. Conversely, opting for a lower deductible means you’re asking the insurer to shoulder more of the immediate financial burden, which they offset with higher premiums.

Financial Preparedness

The most critical factor in determining your deductible is your ability to comfortably afford to pay it. If you choose a $1,000 deductible but would struggle to come up with that amount in an emergency, you might be setting yourself up for financial strain. Before selecting a deductible, honestly assess your emergency savings. Can you readily access $500, $1,000, or even $2,000 without jeopardizing your other financial obligations? It’s far better to have a slightly higher premium and a deductible you can manage than a lower premium and a deductible that would cause hardship in a claim scenario.

Risk Tolerance

Your personal tolerance for risk also plays a role. Some individuals are naturally more risk-averse and prefer to pay a higher premium for the peace of mind that comes with a lower deductible. They might see the lower deductible as a form of insurance against unexpected and significant out-of-pocket expenses. Others might be more comfortable taking on a bit more risk, opting for a higher deductible to save money on premiums, believing that major, costly incidents are less likely to occur or that they have sufficient savings to cover the deductible if they do.

Factors to Consider When Setting Your Deductible

- Emergency Fund: Do you have a robust emergency fund that can cover the deductible amount?

- Monthly Budget: Can you comfortably afford the higher premium associated with a lower deductible, or would a lower premium with a higher deductible be more manageable for your monthly budget?

- Vehicle Value: While not directly tied to the deductible amount itself, the value of your vehicle can influence your overall insurance costs and your perception of risk. For very expensive vehicles, you might feel more inclined to have a lower deductible to minimize your personal contribution to repairs.

- Driving Habits: Your driving habits and the typical conditions you drive in can also influence your perceived risk. If you drive in high-traffic areas or have a history of accidents, you might lean towards a lower deductible for greater protection.

When Does Your Deductible Apply?

Your deductible is only applicable when you make a claim that is covered by your auto insurance policy and results in a payout from the insurer. It does not apply to every interaction with your insurance company.

Filing a Claim

When you experience a covered event, such as a collision or theft, you will file a claim with your insurance provider. After assessing the damage and determining the cost of repairs or replacement, the insurance company will inform you of the applicable deductible. You will then be responsible for paying this amount directly to the repair shop or as part of the settlement process. The insurance company will then pay the remaining balance up to the policy limits.

Situations Where the Deductible Might Not Apply

- Not at Fault Accidents: In some states, if you are involved in an accident where the other driver is clearly at fault and their insurance company accepts liability, your insurance company might waive your deductible, or you may be able to recover it directly from the at-fault driver’s insurer. However, this process can sometimes be complex and may require you to initially pay your deductible and then seek reimbursement. It’s essential to understand your state’s specific laws and your policy’s terms regarding uninsured or underinsured motorists and subrogation.

- Minor Incidents: If the damage to your vehicle is minor and the repair cost is less than or equal to your deductible, it often makes financial sense not to file a claim. For example, if your deductible is $500 and the repairs will cost $400, filing a claim would mean you pay the full $400 out-of-pocket anyway, and you might also see an increase in your premium for making a claim, even if it wasn’t covered by insurance.

- Liability Claims Against You: If you cause an accident and are found to be at fault, your liability coverage will pay for the damages to the other party’s vehicle or property, and their medical expenses. Your deductible does not apply to these payouts; it only applies to damage to your vehicle.

Adjusting Your Deductible Over Time

Your insurance needs and financial circumstances can change over the years. It’s wise to periodically review your auto insurance policy, including your deductible.

When to Consider Adjusting Your Deductible

- Financial Changes: If your income has increased and you have built a more substantial emergency fund, you might feel comfortable increasing your deductible to lower your premiums. Conversely, if you’ve experienced a financial setback, you might consider lowering your deductible, even if it means a slightly higher premium, to ensure you can manage any repair costs.

- Vehicle Age and Value: As your vehicle ages, its market value typically decreases. If the value of your car is approaching or has fallen below your deductible amount, it may no longer be economically sensible to carry collision or comprehensive coverage with a high deductible. In such cases, you might consider dropping this coverage altogether, which would, of course, eliminate the deductible associated with it.

- Changes in Driving Habits: If your driving patterns have changed significantly – perhaps you’re commuting less or driving in safer areas – you might feel your risk profile has decreased, potentially influencing your comfort level with a higher deductible.

How to Adjust Your Deductible

Adjusting your deductible is typically a straightforward process. You will need to contact your insurance agent or the insurance company directly. They will guide you through the necessary paperwork and explain how the change will affect your premium. It’s crucial to ensure the adjustment is made official and reflected in your updated policy documents.

In conclusion, understanding your auto insurance deductible is not merely a technicality; it’s a cornerstone of responsible car ownership and effective financial planning. By grasping its implications, choosing wisely based on your circumstances, and periodically reviewing your policy, you can ensure your auto insurance serves its intended purpose – protecting you from significant financial loss while remaining an affordable and manageable part of your budget.