The concept of “auto equity” is a term that often arises in discussions surrounding vehicle financing and ownership. While it might sound like a technical jargon exclusive to the automotive industry, understanding auto equity can be incredibly beneficial for consumers looking to leverage their vehicle’s value. At its core, auto equity refers to the difference between the current market value of a vehicle and the outstanding balance owed on any loans secured by that vehicle. It represents the portion of the vehicle’s value that the owner truly possesses, free and clear of debt. This concept is crucial for anyone looking to sell their car, trade it in, refinance their loan, or even secure a personal loan using their vehicle as collateral.

The Fundamentals of Auto Equity

To truly grasp the significance of auto equity, it’s essential to break down its components and understand how it is calculated and influenced. This involves looking at both the value of the vehicle and the remaining debt.

Vehicle Value: The Driving Force

The market value of a vehicle is not static; it depreciates over time due to factors such as age, mileage, wear and tear, and market demand. Several resources can help determine a vehicle’s current worth.

Depreciation: The Inevitable Decline

Depreciation is the most significant factor affecting a vehicle’s value. New cars experience the steepest depreciation in their first few years. As a car ages, the rate of depreciation typically slows down. High mileage, a lack of maintenance, cosmetic damage, and mechanical issues will further accelerate depreciation. Conversely, well-maintained vehicles, especially those with lower mileage and in high-demand models, may depreciate at a slower rate. Understanding depreciation is key to accurately assessing your vehicle’s market value.

Market Conditions: Supply and Demand Dynamics

The broader automotive market plays a substantial role in determining a vehicle’s value. During periods of high demand for used cars, such as when new car production is disrupted, the market value of existing vehicles can increase. Conversely, an oversupply of a particular model or a general economic downturn can lead to lower market values. Factors like fuel prices (affecting demand for SUVs versus sedans) and regional preferences also contribute to market conditions.

Loan Balance: The Reducing Factor

The outstanding loan balance is the amount of money still owed to the lender for the vehicle. This is a straightforward calculation based on the amortization schedule of the loan.

Outstanding Debt: What You Still Owe

Each month, a portion of your car payment goes towards reducing the principal loan balance. Auto equity is directly impacted by this reduction. The lower the outstanding balance, the higher the auto equity, assuming the vehicle’s value remains constant. Conversely, if you owe more on your loan than the car is worth, you have negative equity.

Interest and Fees: Added Costs

It’s important to remember that interest charges and any associated loan fees contribute to the total amount you owe. While these don’t directly reduce the vehicle’s value, they do increase the outstanding debt, thus impacting the equity calculation. Early in a loan term, a larger portion of your payment typically goes towards interest, meaning the principal balance reduces more slowly, and therefore, equity builds up at a slower pace.

Calculating and Understanding Your Auto Equity

Once you understand the two primary components, calculating auto equity becomes a simple subtraction. However, the implications of having positive, zero, or negative equity are significant and dictate various financial decisions.

The Equity Equation: Value Minus Debt

The formula for calculating auto equity is straightforward:

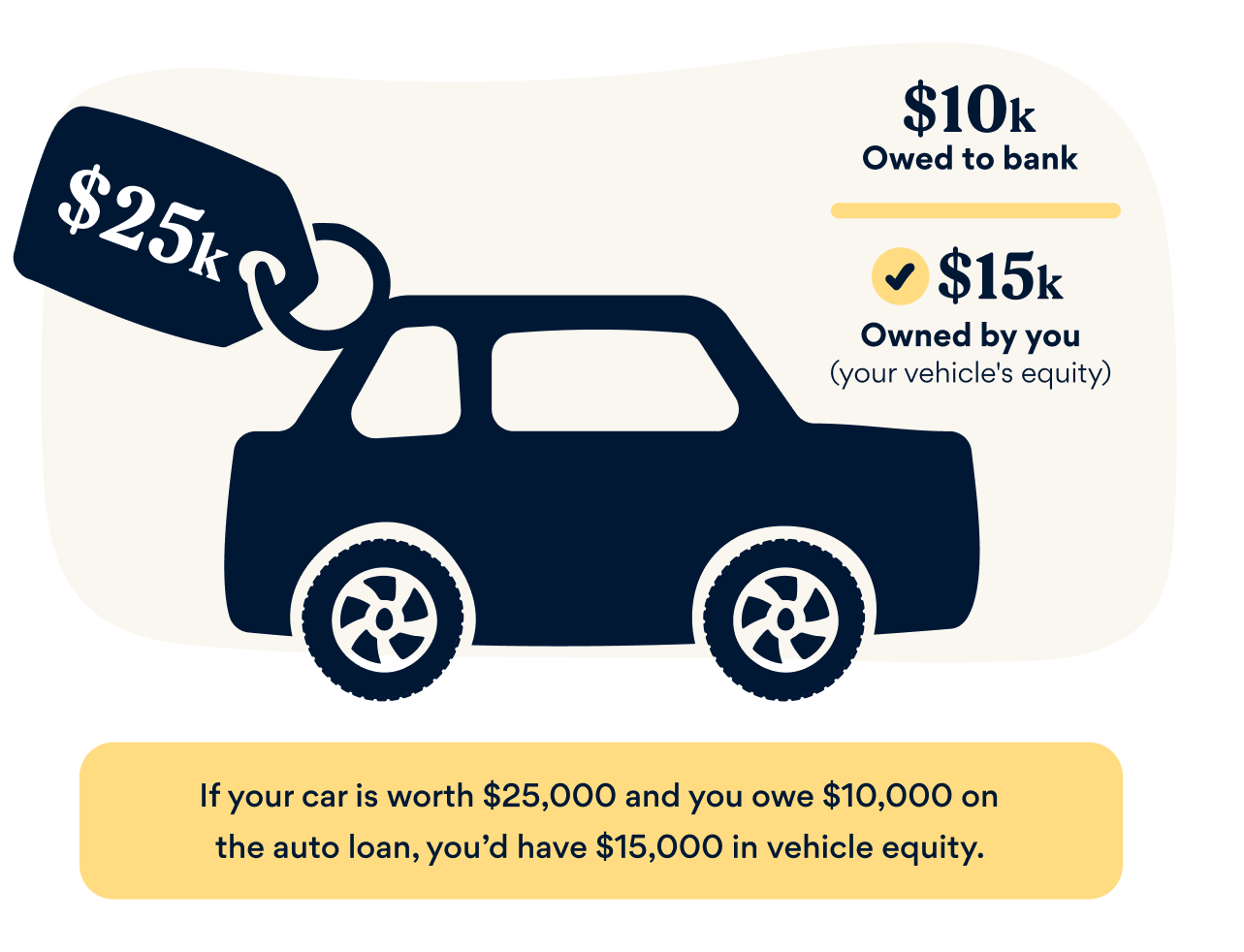

Auto Equity = Current Market Value of Vehicle – Outstanding Loan Balance

For example, if your car is currently valued at $15,000 and you owe $10,000 on your car loan, you have $5,000 in positive auto equity. If your car is valued at $12,000 and you owe $15,000, you have -$3,000 in negative equity.

Positive Equity: A Valuable Asset

Positive auto equity signifies that you own more of your car than you owe. This is a desirable financial position.

Benefits of Positive Equity

Having positive equity offers several advantages. It makes selling your car easier, as you can use the equity to pay off your loan and potentially have money left over. When trading in your vehicle, positive equity reduces the amount you need to finance on a new car. Furthermore, lenders are more willing to offer favorable terms for auto equity loans or refinancing when there is a substantial positive equity buffer. It essentially represents a tangible asset that can be leveraged.

Leveraging Positive Equity

Positive equity can be a powerful financial tool. You can use it to:

- Sell or Trade-In: As mentioned, it simplifies the process and can put cash in your pocket.

- Refinance Your Loan: You might qualify for a lower interest rate or a different loan term on your existing car loan, saving you money over time.

- Secure a Loan: Auto equity loans (also known as car title loans, though this term can carry negative connotations due to high-interest rates and predatory practices) allow you to borrow money using your car’s equity as collateral. This can be useful for unexpected expenses or debt consolidation.

Negative Equity: The “Upside Down” Scenario

Negative equity, often referred to as being “upside down” on your loan, occurs when the outstanding loan balance exceeds the vehicle’s market value. This is a common situation, especially in the early years of a car loan.

Challenges of Negative Equity

Negative equity presents several challenges. Selling your car will result in a loss because the sale proceeds won’t be enough to cover the loan balance. You will need to pay the difference out of pocket or roll it into a new loan, which often leads to even higher payments and more negative equity. Trading in a car with negative equity means that the deficit will be added to the loan for your next vehicle, increasing your overall debt and monthly payments. Refinancing options are also limited, and lenders may be hesitant to approve new loans.

Addressing Negative Equity

If you find yourself in negative equity, there are a few strategies to consider:

- Continue Paying the Loan: The most straightforward, albeit slow, method is to continue making your regular payments. As you pay down the principal and the car depreciates, you will eventually reach a point of zero or positive equity.

- Pay Extra Towards Principal: Making extra payments specifically towards the principal balance can accelerate the reduction of your debt, helping you exit negative equity faster.

- Wait for Market Shifts: In some cases, the used car market may rebound, increasing your vehicle’s value and reducing your negative equity. This is not a strategy to rely on but can be a fortunate outcome.

- Save for a Down Payment: If you plan to buy a new car, saving a significant down payment can help offset negative equity and ensure you start your next loan with a more favorable loan-to-value ratio.

The Role of Auto Equity in Financial Decisions

Understanding your auto equity is not just an academic exercise; it directly influences critical financial decisions related to your vehicle and beyond.

Selling or Trading In Your Vehicle

When you decide to sell your car privately or trade it in at a dealership, your auto equity is a primary consideration.

Private Sale vs. Dealership Trade-In

In a private sale, you aim to sell the car for its fair market value. If you have positive equity, the sale proceeds will cover your loan, and any remaining amount is yours. With negative equity, you’ll need to cover the difference between the sale price and the loan balance. A dealership trade-in often simplifies the process. The dealer will offer you a value for your car, which they will apply towards the purchase of a new vehicle. If you have positive equity, it reduces the amount you need to finance on the new car. If you have negative equity, the dealership may roll that deficit into the new loan, which can lead to higher monthly payments and a larger overall debt.

Negotiating Your Trade-In Value

Knowing your car’s market value and your outstanding loan balance empowers you during trade-in negotiations. You can confidently discuss the equity you have and ensure you are getting a fair offer that reflects both your car’s worth and your financial position.

Refinancing and Auto Equity Loans

Auto equity can be a gateway to better loan terms or even accessing cash.

Refinancing Your Car Loan

If you have positive equity and your credit score has improved since you took out your original loan, you may qualify to refinance your car loan. This process involves taking out a new loan to pay off your old one, potentially with a lower interest rate, a shorter term, or a more manageable monthly payment. The lender will assess your car’s value and your equity to determine your loan-to-value ratio, which influences their decision and the terms they offer.

Utilizing Auto Equity Loans

An auto equity loan allows you to borrow money using the equity in your car as collateral. These loans can be useful for various purposes, such as consolidating high-interest debt, covering unexpected medical expenses, or funding home improvements. However, it’s crucial to approach auto equity loans with caution. They are secured loans, meaning if you default, the lender can repossess your vehicle. Interest rates and fees can vary significantly, and it’s essential to compare offers and understand the full cost of borrowing.

The Importance of Regular Assessment

Given that vehicle value depreciates and loan balances decrease over time, your auto equity is not a fixed number. It changes continuously.

Tracking Depreciation and Loan Payoff

Regularly checking your car’s estimated market value and comparing it to your outstanding loan balance allows you to stay informed about your equity position. This proactive approach can help you make timely financial decisions, such as deciding when it might be advantageous to sell or refinance. Resources like Kelley Blue Book, Edmunds, and NADA Guides can provide reliable estimates for your vehicle’s value.

Planning for Future Purchases

Understanding your current auto equity is vital when planning for your next vehicle purchase. If you have significant positive equity, it can serve as a substantial down payment, reducing your financing needs and monthly payments on a new car. Conversely, if you’re in negative equity, you’ll need to factor in the cost of covering that deficit when budgeting for a new purchase. This foresight can prevent you from getting into a cycle of accumulating debt and negative equity with each new vehicle.