Auditing in accounting is a systematic and independent examination of financial statements, records, and other documentation to determine whether they fairly and accurately represent the financial position and performance of an entity. It serves as a critical pillar of financial transparency and accountability, providing stakeholders—investors, creditors, regulators, and management—with confidence in the reliability of reported financial information. Far from being a mere compliance exercise, a robust audit process offers profound insights into an organization’s financial health, operational efficiency, and adherence to established accounting principles and regulatory standards.

At its core, auditing is about verification and validation. It involves scrutinizing transactions, internal controls, and overall financial reporting to uncover material misstatements, whether due to error or fraud. The independent nature of the auditor is paramount; their objectivity ensures an unbiased assessment, lending credibility to the financial data upon which crucial economic decisions are made. In an increasingly complex global economy, the role of auditing has expanded beyond traditional financial statement reviews to encompass operational, compliance, and even information technology audits, reflecting the multifaceted risks and demands organizations face.

The discipline of auditing is underpinned by a rigorous set of professional standards, ethical guidelines, and legal frameworks, such as Generally Accepted Auditing Standards (GAAS) in the U.S. or International Standards on Auditing (ISAs) globally. These standards dictate the planning, execution, and reporting phases of an audit, ensuring consistency, quality, and thoroughness. As businesses evolve and technology reshapes financial processes, auditing methodologies are also constantly adapting, leveraging data analytics, artificial intelligence, and other innovations to enhance effectiveness and efficiency.

The Foundational Principles and Purpose of Auditing

Auditing is not a random check but a structured process guided by specific principles designed to achieve its overarching purpose: to provide reasonable assurance that financial statements are free from material misstatement. This assurance is crucial for maintaining trust in capital markets and enabling informed decision-making.

Independence and Objectivity: Cornerstones of Trust

The bedrock of any credible audit is the auditor’s independence and objectivity. Independence refers to the auditor’s ability to act impartially and without bias, free from any financial or personal interests that could compromise their professional judgment. This includes being independent in fact (mindset) and in appearance (how others perceive them). Objectivity, closely related, demands that auditors approach their work with a neutral and unbiased perspective, letting the evidence guide their conclusions rather than predispositions. Without these two qualities, the auditor’s opinion would lack credibility, undermining the entire purpose of the audit. Regulatory bodies and professional organizations enforce strict rules regarding auditor independence, often requiring rotation of audit partners and prohibiting certain non-audit services to preserve this critical attribute.

Materiality and Audit Risk

Two fundamental concepts that guide an auditor’s judgment are materiality and audit risk. Materiality refers to the significance of an omission or misstatement of financial information that, individually or in aggregate, could influence the economic decisions of users made on the basis of the financial statements. Auditors establish a materiality threshold early in the audit planning phase to focus their efforts on areas most likely to contain significant errors. Items below this threshold are generally considered immaterial. Audit risk, on the other hand, is the risk that the auditor expresses an inappropriate audit opinion when the financial statements are materially misstated. It comprises inherent risk (susceptibility of an assertion to misstatement), control risk (risk that internal controls won’t prevent/detect misstatement), and detection risk (risk that the auditor’s procedures won’t detect a material misstatement). Auditors design their procedures to keep audit risk at an acceptably low level.

Professional Skepticism

Professional skepticism is an attitude that includes a questioning mind and a critical assessment of audit evidence. It means auditors should not accept information at face value but should instead critically evaluate evidence, question management’s assertions, and be alert to conditions that may indicate possible misstatement due to error or fraud. This mindset is vital for uncovering subtle discrepancies, challenging assumptions, and preventing complacency. It drives auditors to seek corroborating evidence and carefully consider the implications of inconsistent findings.

Types of Audits and Their Specific Applications

While financial statement audits are the most common, the field of auditing encompasses various specialized types, each serving a distinct purpose and focusing on different aspects of an organization’s operations.

Financial Audits

The most prevalent type, financial audits, focus on the veracity and fair presentation of an organization’s financial statements (balance sheet, income statement, statement of cash flows, and statement of changes in equity). The objective is to provide an independent opinion on whether these statements are prepared, in all material respects, in accordance with an applicable financial reporting framework (e.g., GAAP or IFRS). This involves examining accounting records, internal control systems, and corroborating evidence, leading to the auditor’s report that accompanies the financial statements. Financial audits are mandatory for publicly traded companies and often required for privately held entities by lenders or investors.

Compliance Audits

Compliance audits evaluate an organization’s adherence to specific laws, regulations, policies, and procedures. This could include tax laws, environmental regulations, industry-specific standards, or internal company policies. For example, a compliance audit might verify whether a company is meeting its regulatory obligations under Sarbanes-Oxley (SOX) for internal controls over financial reporting or adhering to data privacy regulations like GDPR. The aim is to identify areas of non-compliance, assess the associated risks, and recommend corrective actions to prevent legal penalties, fines, or reputational damage.

Operational Audits

Operational audits are forward-looking and aim to assess the efficiency and effectiveness of an organization’s operational activities and processes. Unlike financial audits, which focus on historical data, operational audits evaluate whether an organization’s resources are being utilized optimally to achieve its objectives. This could involve reviewing production processes, supply chain management, marketing strategies, or human resource functions. The outcome is typically a report identifying areas for improvement, cost savings, and enhanced productivity, making it a valuable tool for management in strategic planning and performance enhancement.

Forensic Audits

Forensic audits are specialized investigations into specific financial anomalies or allegations of fraud. They are conducted when there is suspicion of criminal activity, such as embezzlement, money laundering, or asset misappropriation. Forensic auditors possess not only accounting and auditing skills but also investigative expertise, often working closely with legal professionals. Their objective is to gather evidence that can be used in a court of law or for insurance claims. The output is a detailed report outlining the findings, evidence, and often quantification of financial losses, supporting legal proceedings.

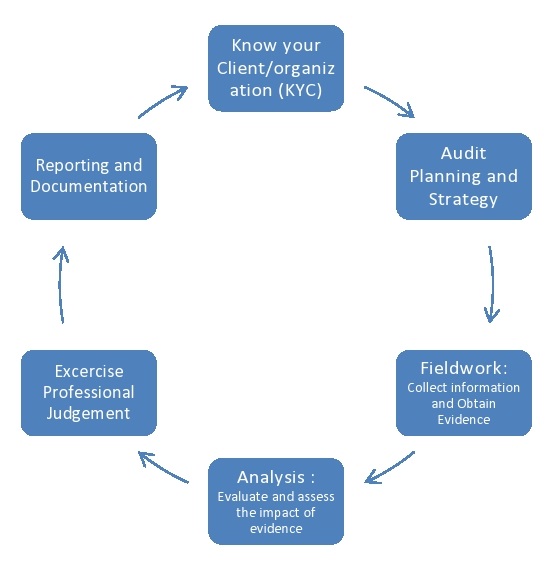

The Audit Process: A Systematic Approach

An audit is a systematic process broken down into several distinct phases, each with specific objectives and activities designed to achieve the overall audit goal.

Planning and Risk Assessment

The initial and arguably most critical phase is planning. Auditors begin by gaining a comprehensive understanding of the client’s business, industry, regulatory environment, and internal control systems. This involves discussions with management, review of prior audit documentation, and analytical procedures. A key output of this phase is the risk assessment, where auditors identify and evaluate inherent risks (risks specific to the business) and control risks (risks that internal controls will fail). This assessment helps determine the scope of the audit, the appropriate materiality levels, and the necessary audit procedures to be performed, allowing for efficient allocation of audit resources to areas of highest risk.

Fieldwork and Evidence Gathering

During the fieldwork phase, auditors execute the planned audit procedures to gather sufficient appropriate audit evidence. This involves a variety of techniques, including:

- Inspection: Examining records, documents (internal and external), and tangible assets.

- Observation: Watching processes or procedures being performed by others.

- Inquiry: Seeking information from knowledgeable persons within or outside the entity.

- Confirmation: Obtaining direct communication from third parties (e.g., banks, customers, vendors) regarding account balances or transactions.

- Recalculation: Checking the arithmetical accuracy of documents or records.

- Re-performance: Independent execution of procedures or controls that were originally performed by the entity’s internal control system.

- Analytical Procedures: Evaluating financial information through analysis of plausible relationships among both financial and non-financial data, often used to identify unusual fluctuations or relationships.

The evidence gathered must be sufficient in quantity and appropriate in quality (relevant and reliable) to support the auditor’s conclusions.

Reporting and Opinion Formulation

The final stage of the audit process culminates in the issuance of the auditor’s report. Based on the evidence gathered, auditors formulate an opinion on whether the financial statements are presented fairly, in all material respects, in accordance with the applicable financial reporting framework. The most desirable outcome is an unmodified (or clean) opinion, indicating that the financial statements are free from material misstatement. However, if material misstatements exist and are not corrected, or if there are scope limitations, the auditor may issue a modified opinion:

- Qualified Opinion: Financial statements are generally presented fairly, but there is a material misstatement that is not pervasive to the financial statements, or a scope limitation that is not pervasive.

- Adverse Opinion: Financial statements are materially misstated and pervasive, meaning they do not present fairly the financial position or results of operations.

- Disclaimer of Opinion: The auditor is unable to express an opinion due to a significant scope limitation or uncertainty, where insufficient appropriate audit evidence was obtained.

The auditor’s report provides essential credibility to the financial statements, allowing stakeholders to make informed decisions with a higher degree of confidence.

The Evolving Landscape of Auditing

The auditing profession is dynamic, continually adapting to technological advancements, changes in regulatory environments, and evolving stakeholder expectations.

Technology’s Impact on Audit Methodologies

Technology is profoundly reshaping how audits are conducted. Data analytics tools allow auditors to process vast amounts of data, identify patterns, anomalies, and potential risks much more efficiently than manual methods. Artificial intelligence (AI) and machine learning (ML) are being integrated to automate routine tasks, enhance risk assessment, and provide deeper insights by analyzing complex datasets. Blockchain technology, with its immutable ledger, presents both opportunities for enhanced data integrity and challenges for audit verification. Cloud computing facilitates real-time data access and collaboration, while robotic process automation (RPA) streamlines repetitive audit procedures. These technologies are not only increasing audit efficiency but also expanding the scope and depth of analysis, moving towards more continuous auditing models.

Focus on Environmental, Social, and Governance (ESG) Factors

Beyond traditional financial reporting, there’s a growing demand for assurance on Environmental, Social, and Governance (ESG) information. Investors, regulators, and the public are increasingly concerned with a company’s sustainability practices, social impact, and governance structures. This has led to the emergence of ESG audits or assurance engagements, where auditors provide independent verification of non-financial data, such as carbon emissions, labor practices, or board diversity metrics. While frameworks for ESG reporting and assurance are still developing, this area represents a significant expansion of the auditor’s role, requiring specialized knowledge and methodologies.

Regulatory Changes and Enhanced Scrutiny

The regulatory landscape for auditing is constantly evolving, driven by high-profile corporate scandals and the need to bolster investor confidence. Regulations like Sarbanes-Oxley Act (SOX) introduced stringent requirements for internal controls over financial reporting, significantly impacting audit scope. International standards are also continuously refined to address emerging risks and improve audit quality. Regulators are increasingly scrutinizing audit firms themselves, emphasizing audit quality control, professional skepticism, and the effective application of auditing standards. This heightened scrutiny ensures that audit firms maintain the highest levels of integrity and competence, reinforcing the public trust placed in the auditing profession.

In conclusion, auditing in accounting is a fundamental function that underpins the integrity of financial information and the stability of capital markets. It is a rigorous, principle-driven process conducted by independent professionals to provide assurance on financial statements and other critical data. As the business world grows more complex and technologically advanced, the auditing profession continues to evolve, embracing new tools and expanding its scope to meet the multifaceted demands of a globalized and digitally interconnected economy.