For many entrepreneurs and business owners, the journey from a nascent idea to a thriving enterprise is paved with complex decisions, particularly concerning legal structure and tax implications. Among the various organizational forms available, the Limited Liability Company (LLC) and the S Corporation status represent two distinct yet often intertwined concepts. Understanding what constitutes an S Corporation LLC is crucial for optimizing business operations, managing tax liabilities effectively, and ensuring long-term growth. This article aims to demystify this hybrid structure, exploring its benefits, drawbacks, and the considerations necessary for choosing it.

Understanding the Fundamentals: LLCs and S Corporations

Before delving into the specifics of an S Corporation LLC, it’s essential to grasp the individual characteristics of both an LLC and an S Corporation. These foundational elements will illuminate why a business might opt to combine aspects of both.

The Limited Liability Company (LLC)

An LLC is a popular business structure that offers a blend of the liability protection of a corporation and the pass-through taxation of a partnership or sole proprietorship.

Liability Protection

One of the primary advantages of forming an LLC is the limited liability it provides to its owners, known as members. This means that the personal assets of the members are generally protected from business debts and lawsuits. If the LLC incurs debt or faces legal action, creditors and litigants can typically only pursue the assets of the business, not the personal savings, homes, or vehicles of the owners. This separation of personal and business liabilities is a significant draw for entrepreneurs seeking to mitigate personal risk.

Pass-Through Taxation

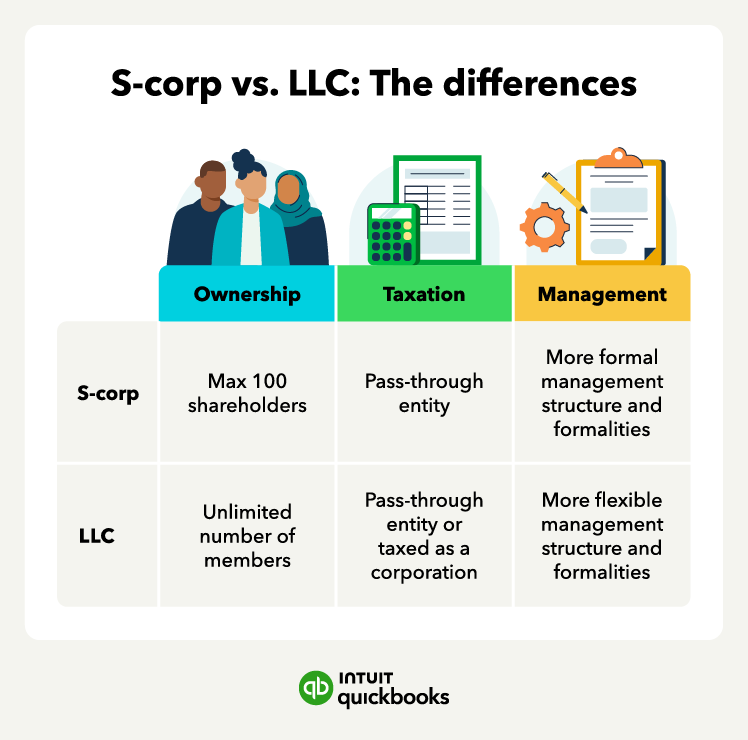

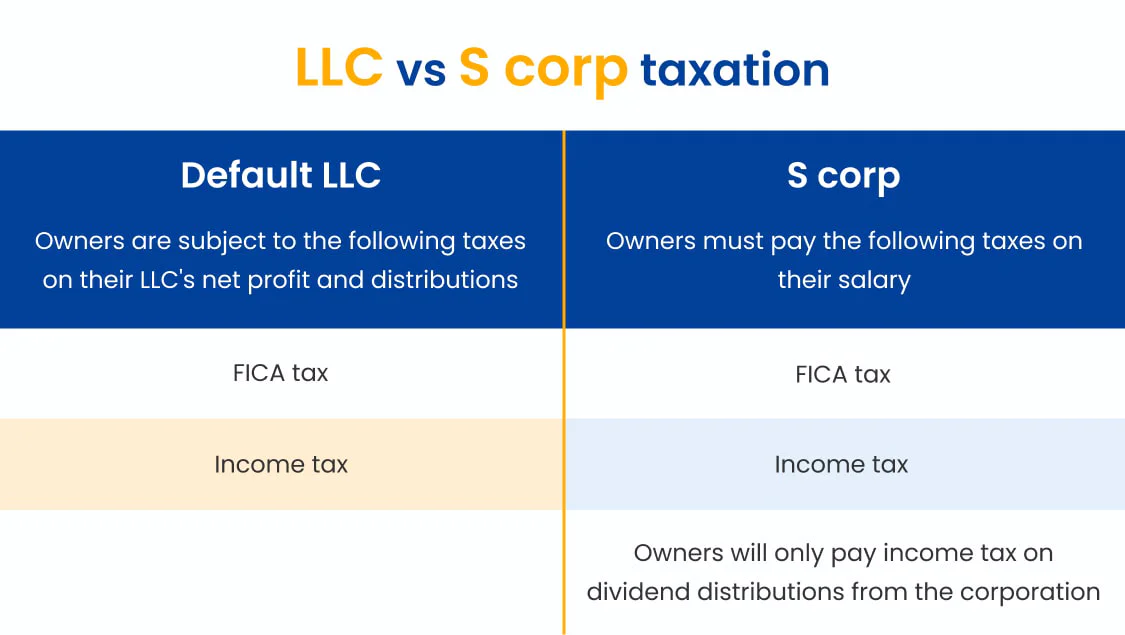

By default, an LLC is treated as a pass-through entity for tax purposes. This means that the business itself does not pay federal income taxes. Instead, the profits and losses of the LLC are “passed through” to its members, who then report this income or loss on their individual tax returns. This avoids the “double taxation” that can occur with C Corporations, where profits are taxed at the corporate level and then again when distributed to shareholders as dividends. For single-member LLCs, they are taxed like sole proprietorships, and for multi-member LLCs, they are taxed like partnerships.

Operational Flexibility

LLCs offer a high degree of operational flexibility. They are not subject to the stringent record-keeping requirements and corporate formalities often associated with traditional corporations. Decision-making processes can be tailored to the needs of the business, and ownership structures can be more adaptable.

The S Corporation Status

An S Corporation is not a business structure in itself, but rather a tax election made with the Internal Revenue Service (IRS) by an eligible LLC or corporation. This election allows the business to be taxed under Subchapter S of the Internal Revenue Code.

The Pass-Through Advantage (with a Twist)

Similar to LLCs, S Corporations are pass-through entities, meaning profits and losses are reported on the owners’ individual tax returns. However, the key difference lies in how owners are compensated and how that compensation is taxed. Owners who actively work for the S Corporation are considered employees and must be paid a “reasonable salary” as an employee. This salary is subject to payroll taxes (Social Security and Medicare). Any remaining profits can then be distributed as dividends, which are not subject to self-employment taxes.

Avoiding Self-Employment Taxes

This distinction in taxation is the primary driver for many businesses to elect S Corporation status. By paying a reasonable salary and then taking distributions, owners can potentially reduce their overall tax burden, as distributions are not subject to the 15.3% self-employment tax that applies to all net earnings from self-employment for LLCs taxed as sole proprietorships or partnerships.

Eligibility Requirements

To qualify for S Corporation status, a business must meet several criteria. These include being a domestic entity, having only allowable shareholders (U.S. citizens or resident aliens, certain trusts, and estates), having no more than 100 shareholders, and having only one class of stock.

The S Corporation LLC: A Hybrid Approach

When an LLC elects to be taxed as an S Corporation, it essentially combines the operational flexibility and liability protection of an LLC with the tax advantages of S Corporation status. This fusion offers a unique set of benefits for business owners.

The Synergy of Structure and Taxation

The core appeal of an S Corporation LLC lies in its ability to leverage the strengths of both legal structures. The LLC framework provides a robust legal shield, separating personal assets from business liabilities. Simultaneously, the S Corporation tax election offers a potential avenue for tax savings by allowing owners to manage their income through both salary and distributions.

Enhanced Tax Efficiency

The most compelling reason for an LLC to elect S Corporation status is the potential for significant tax savings. As previously mentioned, by paying a reasonable salary and taking the remainder of the profits as distributions, business owners can reduce their liability for self-employment taxes. This can translate into thousands of dollars saved annually, particularly for businesses with substantial profits.

- Reasonable Salary Determination: A critical aspect of this tax strategy is the determination of a “reasonable salary.” The IRS requires that shareholder-employees be paid a salary commensurate with their services and the value of their contributions to the business. This salary should reflect what the owner would earn if they were an independent employee in a similar role. Failure to establish a reasonable salary can lead to IRS scrutiny and penalties.

- Distribution Strategy: Once a reasonable salary is paid, any remaining profits can be distributed to the owners as dividends. These dividends are not subject to self-employment taxes, offering a direct tax advantage over a standard LLC where all net earnings are subject to these taxes.

Continued Operational Simplicity

While electing S Corporation status introduces more formality concerning payroll and owner compensation, the underlying LLC structure generally retains its operational flexibility. This means that business owners can often continue to manage their day-to-day operations with a degree of freedom that might be constrained by a traditional C Corporation. The operating agreement of the LLC still governs internal management, and the lines of reporting and decision-making can be less rigid than in a corporate setting.

Considerations and Potential Drawbacks

While the S Corporation LLC offers attractive benefits, it’s not a universally ideal solution for every business. Several factors must be carefully weighed before making this election.

Increased Administrative Burden

Electing S Corporation status introduces a new layer of administrative complexity. The business will need to:

- Run Payroll: Establish a formal payroll system to pay shareholder-employees their salaries and withhold appropriate taxes. This often involves working with a payroll service.

- File Additional Tax Returns: The business will need to file IRS Form 1120-S, U.S. Income Tax Return for an S Corporation, in addition to the individual tax returns of the owners.

- Strict Record-Keeping: Maintain meticulous records regarding salaries, distributions, and other financial transactions to support the tax election and ensure compliance.

Eligibility Requirements and Restrictions

As mentioned earlier, S Corporations have specific eligibility requirements that an LLC must meet. The most common hurdles include:

- Number of Shareholders: An LLC electing S Corporation status cannot have more than 100 shareholders.

- Shareholder Types: Only certain types of entities and individuals can be shareholders, excluding partnerships, corporations, and most non-resident aliens.

- One Class of Stock: The business can only have one class of stock, meaning all shares must confer the same rights to dividends and liquidation preferences. While LLCs don’t issue stock, this translates to all members having equal rights to profits and distributions.

The “Reasonable Salary” Scrutiny

The IRS closely scrutinizes the “reasonable salary” paid to shareholder-employees. If the salary is deemed too low, the IRS may reclassify distributions as wages, subjecting them to payroll taxes and potentially leading to back taxes, penalties, and interest. This requires careful planning and potentially consultation with tax professionals to establish and maintain appropriate salary levels.

When is an S Corporation LLC the Right Choice?

The decision to elect S Corporation status for an LLC is a strategic one, best suited for businesses that meet specific criteria and have a clear understanding of the associated responsibilities.

Key Indicators for Consideration

Several factors suggest that an S Corporation LLC might be an advantageous structure:

- Profitable Businesses: The tax savings associated with S Corporation status are most impactful for businesses that generate significant profits beyond what is needed for a reasonable owner salary. Businesses operating at a loss or with minimal profits will likely not see substantial tax benefits.

- Desire to Optimize Self-Employment Taxes: If reducing self-employment tax liability is a primary financial goal, and the business is structured as an LLC, exploring the S Corporation election is a logical step.

- Owner Involvement: The S Corporation election is most beneficial for owners who are actively involved in the business and can draw a reasonable salary. It is not intended for passive investors.

- Commitment to Administrative Compliance: Business owners must be prepared for the increased administrative requirements, including payroll processing and more detailed tax filings.

Situations Where It Might Not Be Ideal

Conversely, an S Corporation LLC may not be the best fit in certain scenarios:

- New or Unprofitable Businesses: The added administrative costs and complexity may outweigh any potential tax benefits for businesses that are just starting or are not yet consistently profitable.

- Businesses with Complex Ownership Structures: If the business has many owners, foreign investors, or a desire for multiple classes of stock (e.g., different voting rights), an S Corporation election might not be feasible.

- Businesses Prioritizing Absolute Simplicity: For entrepreneurs who prioritize the utmost simplicity in business administration, the added requirements of S Corporation status might be a deterrent.

Navigating the Election and Ongoing Compliance

Making the decision to elect S Corporation status is only the first step. Understanding the process and maintaining ongoing compliance are vital for realizing the full benefits and avoiding potential pitfalls.

The Election Process

To elect S Corporation status, an eligible LLC must file IRS Form 2553, Election by a Small Business Corporation. This form must be filed within a specific timeframe: generally, no later than 2 months and 15 days after the beginning of the tax year the election is to take effect, or at any time during the tax year preceding the tax year it is to take effect. Timeliness is crucial, as missing the deadline can mean waiting until the next tax year to make the election.

Maintaining Compliance

Once the S Corporation election is made, ongoing compliance is paramount:

- Payroll and Taxation: Consistently run payroll for shareholder-employees, ensuring that all federal and state payroll taxes are paid on time.

- Accurate Record-Keeping: Maintain detailed and accurate financial records, including all salary payments, distributions, and business expenses.

- Timely Tax Filings: File the annual S Corporation tax return (Form 1120-S) and ensure that individual owners accurately report their share of income and distributions on their personal tax returns.

- Regular Review of Salary: Periodically review the “reasonable salary” to ensure it remains appropriate given market conditions and the owner’s contributions.

Conclusion

The S Corporation LLC represents a sophisticated strategy for business owners looking to balance liability protection with tax efficiency. By electing S Corporation status, an LLC can leverage the pass-through taxation system while potentially mitigating self-employment taxes through a combination of reasonable salary and distributions. However, this powerful tool comes with increased administrative responsibilities and strict eligibility requirements. A thorough understanding of these aspects, coupled with careful planning and professional guidance, is essential to determine if the S Corporation LLC is the optimal structure for your business’s success.