A MICR account number is a crucial piece of information that enables the automated processing of checks and other financial transactions. MICR stands for Magnetic Ink Character Recognition. This technology uses specially printed characters on checks to allow machines to read and interpret the account information quickly and accurately. Understanding what a MICR account number is, where to find it, and how it functions is essential for anyone managing personal or business finances.

The Evolution and Technology Behind MICR

The development of MICR was a significant advancement in financial processing, moving away from slower, manual methods. Its adoption streamlined operations for banks and businesses, reducing errors and speeding up transaction times. The core of MICR lies in its unique ink and character set.

Magnetic Ink and Character Set

The characters that make up the MICR account number are printed using a special magnetic ink. This ink contains iron oxide particles, which can be magnetized. When a check passes through a MICR reader, the magnetic properties of the ink allow the machine to detect the shape of each character. This magnetic signature is then translated into a digital signal that the processing system can understand.

There are two primary fonts used in MICR: E-13B and CMC-7. E-13B is the most common font used in North America and the UK, while CMC-7 is prevalent in Europe and South America. Both fonts consist of a set of 14 characters: the digits 0 through 9, and four special symbols. These symbols are used to separate different parts of the MICR line and to provide formatting for the reader. The distinct shapes and magnetic properties of these characters are specifically designed to be easily and reliably read by machines, even if the check is slightly smudged or creased.

How MICR Readers Work

MICR readers, also known as Magnetic Ink Character Readers, are sophisticated machines that scan checks. When a check is fed into a MICR reader, it passes through a magnetic head, similar to a tape recorder head. This head magnetizes the iron oxide particles in the ink, and as the magnetized particles pass over a sensing coil, they generate an electrical signal. The pattern of these signals corresponds to the shape of the characters. Complex algorithms then decode these patterns into recognizable digits and symbols.

The accuracy of MICR technology is remarkably high, typically exceeding 99% for properly printed checks. This reliability is critical for financial institutions that process millions of checks daily. The speed at which MICR readers can process checks is also impressive, allowing for rapid clearing and settlement of funds. The integration of MICR technology with optical character recognition (OCR) in some advanced systems can further enhance processing by providing a fallback for any characters that may not be perfectly read by magnetic ink alone.

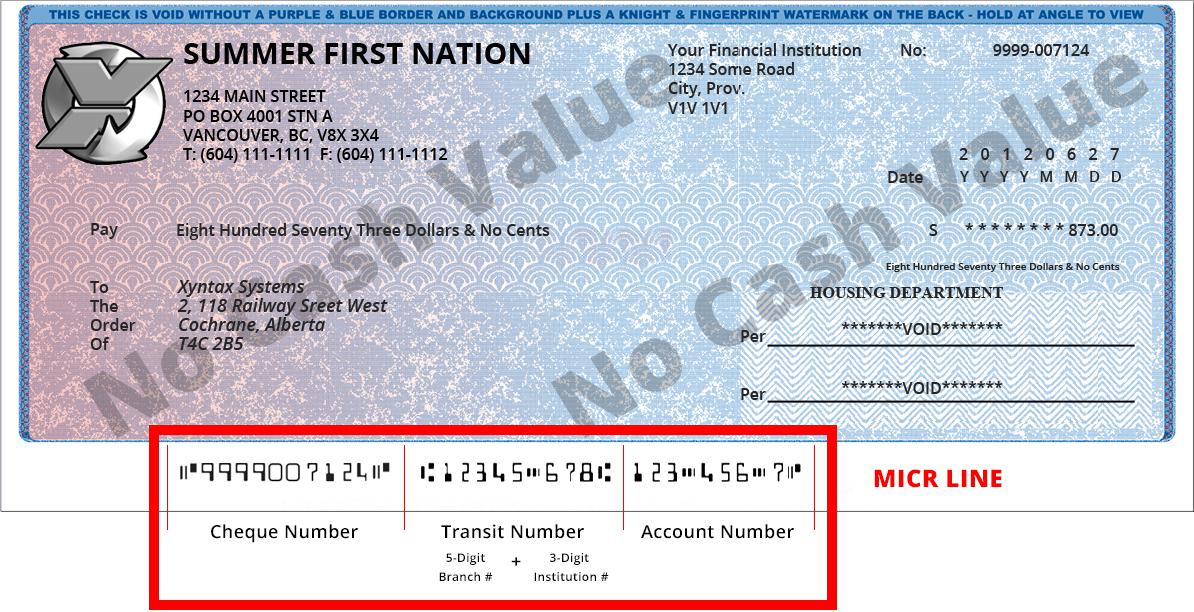

Components of the MICR Line

The MICR line is not just a random string of numbers; it’s a carefully structured sequence of information that facilitates financial transactions. It typically appears at the bottom of a check and contains three main components, each serving a distinct purpose.

Routing Transit Number (RTN)

The Routing Transit Number, often referred to as the ABA (American Bankers Association) number, is a nine-digit number that identifies the financial institution where the account is held. The first four digits represent the Federal Reserve routing symbol, indicating the specific Federal Reserve district and office responsible for the bank. The next four digits identify the specific bank within that district. The final digit is a check digit, used for error detection. The RTN is crucial for directing funds correctly between different banks during the check clearing process. It essentially tells the banking system where to send the money.

Account Number

This is the unique identifier for a specific customer’s account at a particular bank. The length and format of the account number can vary significantly from one bank to another. It’s essential that the account number is accurately printed in the MICR line to ensure that funds are debited or credited to the correct account. Banks typically have internal systems to manage and validate account numbers, ensuring their uniqueness and proper formatting for MICR processing. When you receive a new checkbook, your account number is pre-printed in the MICR line.

Check Number (Serial Number)

The check number, also known as the serial number, is a sequential number assigned to each check in a checkbook. It helps in tracking individual checks and reconciling bank statements. This number typically appears on the right side of the MICR line and is often also printed in the upper right corner of the check itself. While not as critical for the core routing and crediting of funds as the RTN and account number, the check number is vital for record-keeping and fraud prevention. It allows for easy identification and referencing of specific checks that have been issued or cashed.

Where to Find Your MICR Account Number

Locating your MICR account number is straightforward, as it’s a standard feature on most checks. If you don’t have checks readily available, other banking documents can also provide this information.

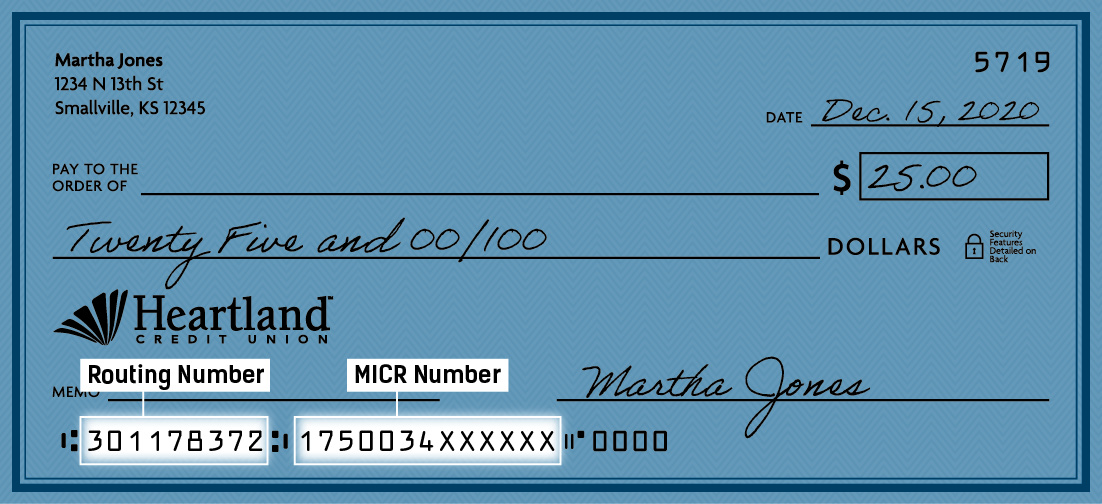

On Your Checks

The most common place to find your MICR account number is on the checks provided by your bank. Look at the bottom of the check. You will see a series of numbers printed in a distinct font. This is the MICR line. Typically, the MICR line begins with the Routing Transit Number, followed by your account number, and ends with the check number. It’s important to distinguish the MICR line from other numbers that might appear on the check, such as the printed check number in the upper right corner. The MICR font is usually a specific style, often referred to as “E-13B,” which is slightly different from standard printing fonts.

Through Your Bank’s Online Portal or Mobile App

If you do not have a check handy, you can often access your MICR information through your bank’s online banking portal or mobile application. After logging in, navigate to your account details. Most banks will provide a section that displays your account number and may also list the Routing Transit Number. While they might not explicitly label it as the “MICR account number,” the information presented is precisely what constitutes the MICR line on your checks. This is a secure and convenient way to retrieve your banking details when needed.

By Contacting Your Bank

For direct confirmation or if you are unable to locate the information through other means, contacting your bank directly is always an option. You can visit a branch in person or call their customer service line. When you contact your bank, be prepared to verify your identity through security questions or other authentication methods. They will then be able to provide you with your account number and the corresponding Routing Transit Number, which together form the essential components of your MICR account number.

The Importance and Function of MICR in Modern Banking

Despite the rise of digital transactions, MICR technology remains a vital component of the financial ecosystem. Its reliability and efficiency continue to support a significant volume of financial operations, ensuring smooth and accurate processing.

Automated Check Processing

MICR is the backbone of automated check processing. When a check is deposited or cashed, it is scanned by MICR readers at the bank. The machine reads the MICR line, extracting the routing number and account number. This information is then transmitted electronically to the clearinghouse, which facilitates the transfer of funds from the payer’s bank to the payee’s bank. This automated process dramatically reduces the time and effort required to clear checks, enabling faster access to funds for individuals and businesses. Without MICR, check processing would revert to manual methods, leading to significant delays and increased operational costs for financial institutions.

Fraud Prevention and Security

The MICR line plays a role in fraud prevention. The magnetic ink and specific font are difficult to counterfeit perfectly. Attempts to alter the MICR line on a check often result in the magnetic ink being disturbed, making it unreadable by MICR machines or flagging it for further inspection. Banks employ sophisticated algorithms and verification processes to detect discrepancies or anomalies in the MICR data. While not a foolproof system against all forms of fraud, the unique characteristics of MICR contribute to a layered security approach in check handling. Furthermore, the structured format of the MICR line allows for automated validation of certain data points, helping to catch obvious errors or potential fraudulent entries early in the processing cycle.

The Role of MICR in Digital Transactions

While many transactions are now digital, checks are still widely used, especially in business-to-business transactions, for certain payments, and by individuals who prefer them. The MICR system seamlessly integrates with modern digital banking infrastructure. Even when a check is initially deposited via a mobile app (which uses an image of the check), the MICR information is still critical for the backend processing and clearing of that check. The image is captured, and the MICR data is extracted and used for the electronic transfer of funds. This bridge between physical checks and digital systems ensures continuity and efficiency in the overall payment landscape. As financial technology continues to evolve, the principles of accurate data capture and automated processing, pioneered by MICR, remain fundamental to the efficiency and security of all financial transactions.