The world of retirement savings can feel like navigating a complex maze, especially when life circumstances change or initial decisions need to be revisited. Among the various strategies available to optimize retirement accounts, an IRA recharacterization stands out as a powerful, albeit sometimes overlooked, tool. This process allows individuals to effectively “undo” a contribution to one type of IRA and move it to another, offering flexibility and potential tax advantages. Understanding when and how to utilize an IRA recharacterization is crucial for any investor seeking to maximize their retirement nest egg and adapt to evolving financial landscapes.

Understanding the Fundamentals of IRA Recharacterization

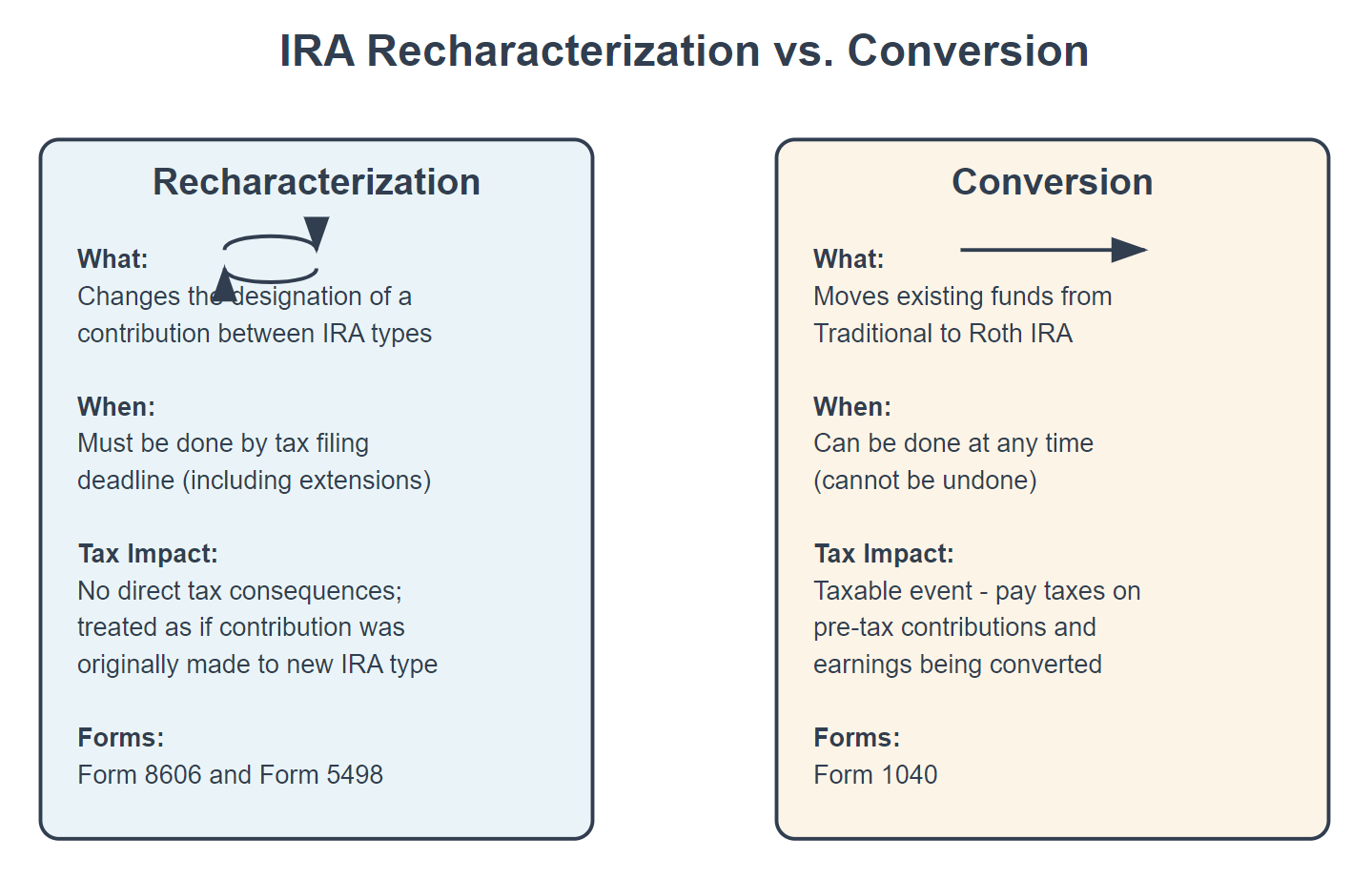

At its core, an IRA recharacterization involves reclassifying a contribution made to one Individual Retirement Arrangement (IRA) as if it had been made to a different type of IRA from the outset. This is not the same as a simple rollover or a conversion, which have distinct purposes and rules. Instead, recharacterization is a retroactive correction, allowing a contribution to be treated as though it was initially intended for a different IRA.

The Mechanics of Recharacterization

The ability to recharacterize a contribution is a specific provision offered by the IRS for IRAs. It primarily applies to Traditional IRAs and Roth IRAs. For example, if you contribute to a Roth IRA but later realize you would have been better off contributing to a Traditional IRA due to income limitations or anticipated future tax rates, you can recharacterize the Roth contribution as a Traditional contribution. Conversely, if you contribute to a Traditional IRA and then decide a Roth IRA is more suitable, you can recharacterize the Traditional contribution to a Roth IRA.

The process typically involves two main steps:

- Removing the original contribution: The funds are first withdrawn from the IRA where they were initially deposited.

- Contributing to the new IRA: The withdrawn funds are then contributed to the intended IRA type.

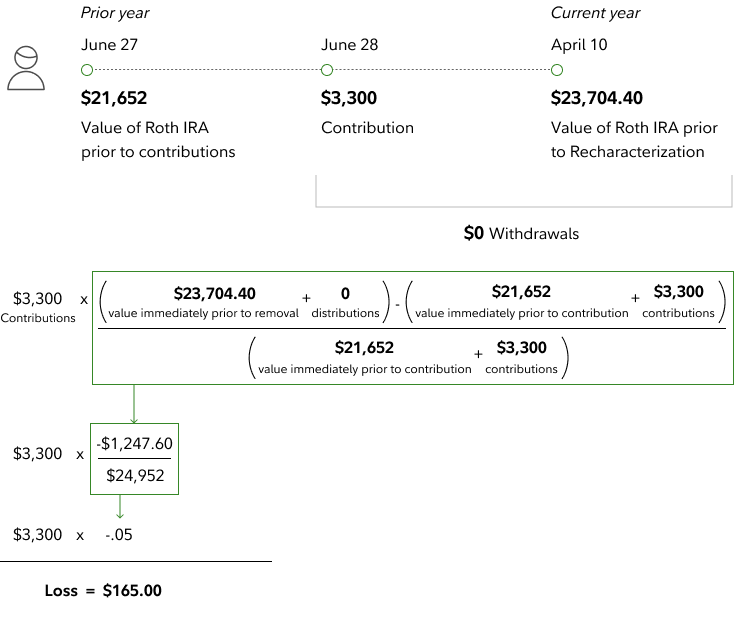

Crucially, when you recharacterize, any earnings or losses that occurred in the original IRA between the time of the contribution and the recharacterization must also be transferred. This ensures that the contribution is treated as if it was in the new IRA all along, including any growth or decline in value.

Key Distinctions: Recharacterization vs. Rollover vs. Conversion

It’s important to differentiate recharacterization from other common IRA transactions:

- Rollover: A rollover involves moving funds from one retirement account to another of the same type. For instance, moving funds from one Traditional IRA to another Traditional IRA, or from a 401(k) to a Traditional IRA. There are specific time limits (usually 60 days) for direct rollovers, and most people are limited to one IRA rollover per 12-month period.

- Conversion: A conversion involves moving funds from a Traditional IRA (or a pre-tax employer-sponsored plan) to a Roth IRA. This is a taxable event, as the pre-tax funds are taxed in the year of conversion. Unlike recharacterization, a conversion is not a retroactive correction but a deliberate election to move assets to a Roth structure.

- Recharacterization: As previously discussed, recharacterization allows you to change the type of IRA a contribution was initially made to, effectively undoing the original classification. It is often done to correct an initial error or to take advantage of changing circumstances.

Who Benefits from Recharacterization?

Several scenarios can make an IRA recharacterization a beneficial strategy:

1. Eligibility for Roth IRA Contributions

Perhaps the most common reason for recharacterizing a contribution is to correct an inadvertent contribution to a Roth IRA when the individual’s income exceeds the Roth IRA contribution limits for that tax year.

- High Earners and Roth IRAs: The IRS sets income limitations for direct Roth IRA contributions. If an individual contributes to a Roth IRA and later realizes their Modified Adjusted Gross Income (MAGI) for that year was above the allowable threshold, they are ineligible to make that direct contribution.

- The Recharacterization Solution: By recharacterizing the Roth IRA contribution into a Traditional IRA, the individual effectively corrects the mistake. The contribution is then treated as if it were made to a Traditional IRA. If the individual is eligible for a tax deduction on the Traditional IRA contribution (based on their income and whether they are covered by a retirement plan at work), they can claim that deduction. If they are not eligible for a deduction, the contribution becomes a non-deductible Traditional IRA contribution.

2. Strategic Tax Planning and Future Tax Expectations

Recharacterization can also be a valuable tool for strategic tax planning, particularly when anticipating future changes in tax brackets or when considering the benefits of tax-free growth offered by a Roth IRA.

- Shifting to a Tax-Advantaged Account: Imagine contributing to a Traditional IRA, but then realizing that tax rates are expected to be higher in retirement than they are now. In such a scenario, it might be more advantageous to have those funds in a Roth IRA, where qualified withdrawals in retirement are tax-free. A recharacterization allows for this shift without triggering immediate taxes on the principal, unlike a Roth conversion.

- Correcting Incorrect Assumptions: Individuals might initially contribute to a Traditional IRA based on the assumption they will be able to deduct the contributions. However, if their income situation changes, or if they are covered by a workplace retirement plan and their income is above certain levels, those deductions may be limited or eliminated. Recharacterizing to a Roth IRA might then be more appealing for the future tax-free growth.

3. Avoiding Penalties on Excess Contributions

If an individual accidentally contributes more to an IRA than they are allowed, they face a 6% penalty tax each year on the excess amount until it is removed.

- The Recharacterization Escape: Recharacterizing an excess contribution to a different IRA type can sometimes be a way to avoid this penalty, provided the recharacterization occurs before the tax filing deadline for that year (including extensions). This allows the individual to move the excess funds to an account where they are properly allocated, or to a different account if the excess was due to making contributions to both a Traditional and Roth IRA when only one was permissible at that income level.

The Timeframe for Recharacterization

The window of opportunity for recharacterizing an IRA contribution is critical. Generally, you have until the tax filing deadline for that year, including any extensions, to recharacterize a contribution.

- Contribution Year vs. Tax Year: It’s important to note that you are recharacterizing a contribution for a specific tax year. For example, if you are recharacterizing a contribution made in 2023, you have until October 15, 2024 (assuming you filed for an extension), to complete the recharacterization.

- No Extensions for Recharacterization Itself: While you might have filed an extension for your tax return, the recharacterization transaction must be completed by the extended deadline. It’s not a matter of filing an extension for the recharacterization itself.

- Consulting with a Financial Professional: Given the strict deadlines and the potential for errors, it is highly advisable to consult with a tax advisor or financial planner well before the deadline to ensure the recharacterization is executed correctly and in your best interest.

The Process of Recharacterization: A Step-by-Step Guide

While the specifics can vary slightly depending on the financial institution holding your IRAs, the general process for recharacterizing a contribution is as follows:

Step 1: Determine Your Eligibility and Desired Outcome

Before initiating the process, confirm that you are eligible for recharacterization and clearly define your goal. Are you correcting an income eligibility issue for a Roth IRA? Are you strategically shifting your retirement savings? Understanding your objective will guide the entire process.

Step 2: Contact Your IRA Custodians

You will need to work with the financial institutions where your IRAs are held.

- Custodian of the Original IRA: Contact the custodian of the IRA to which you made the initial contribution. You will inform them that you wish to recharacterize a specific contribution. They will guide you through their internal procedures for withdrawing the funds and any associated earnings/losses.

- Custodian of the New IRA: Simultaneously, or shortly thereafter, contact the custodian of the IRA to which you intend to recharacterize the funds. They will provide instructions on how to accept the incoming contribution.

Step 3: Transfer the Funds

The funds from the original IRA will need to be transferred to the new IRA. This typically involves:

- Withdrawal from the Original IRA: The custodian of the original IRA will process a withdrawal of the contribution amount plus any accrued earnings (or minus any losses).

- Direct Transfer (Trustee-to-Trustee): The most straightforward and recommended method is a trustee-to-trustee transfer. This involves the custodian of the original IRA directly sending the funds to the custodian of the new IRA. This avoids you personally taking possession of the funds, which can sometimes trigger unwanted tax implications or complicate the process.

- Indirect Transfer (Rolling Over to Yourself): In some cases, you might receive a check made out to you. If this occurs, you must ensure that the funds are deposited into the new IRA within 60 days to avoid it being treated as a taxable withdrawal. However, this method can be more prone to error and is generally less preferred than a direct transfer.

Step 4: Report the Recharacterization on Your Tax Return

This is a crucial step that many individuals overlook.

- IRS Form 8606: For recharacterizations involving Traditional or Roth IRAs, you will need to file IRS Form 8606, “Nondeductible IRAs.” Even if your Traditional IRA contributions were deductible, this form is used to report Roth IRA contributions and conversions, and therefore recharacterizations.

- Accurate Reporting: You must accurately report the recharacterization on your tax return for the year in which the original contribution was made. This includes detailing the amount of the contribution, the original IRA type, the new IRA type, and any earnings or losses transferred. Failure to report the recharacterization correctly can lead to confusion and potential issues with the IRS.

What Happens to Earnings and Losses During Recharacterization?

When you recharacterize a contribution, any investment gains or losses that occurred in the original IRA between the date of the contribution and the date of the recharacterization must be transferred along with the principal.

- Transfer of Net Income/Loss: If the original IRA experienced growth, the earnings are transferred to the new IRA. If it incurred losses, the losses are deducted from the contribution amount before it is recharacterized. The entire net amount is then treated as if it was contributed to the new IRA from the beginning.

- Taxation of Earnings/Losses: Generally, the earnings or losses are considered part of the contribution itself and are not taxed separately at the time of recharacterization. Their tax treatment will depend on the tax status of the new IRA. For example, if you recharacterize into a Roth IRA, any earnings transferred will eventually be eligible for tax-free withdrawal along with other Roth IRA earnings.

Limitations and Considerations

While IRA recharacterization offers significant flexibility, there are important limitations and considerations to keep in mind:

1. The End of Recharacterization for Roth Conversions

A significant change occurred for tax year 2018 and beyond: recharacterization is no longer permitted for Roth conversions. This means that once you convert funds from a Traditional IRA (or other eligible retirement plan) to a Roth IRA, you cannot recharacterize that conversion back to a Traditional IRA. This prohibition underscores the importance of carefully considering Roth conversions, as the decision is now generally irreversible.

2. Contribution Limits Still Apply

Recharacterization does not allow you to exceed the annual IRA contribution limits. If you have already contributed the maximum allowed for a given year to both Traditional and Roth IRAs combined, you cannot use recharacterization to circumvent this limit. It simply allows you to change the classification of a contribution that was already made within the permissible limits.

3. Avoiding the 60-Day Rollover Rule

As mentioned earlier, a trustee-to-trustee transfer is the preferred method for recharacterization. If you take a distribution from one IRA and then contribute it to another, you generally have 60 days to complete the process to avoid it being treated as a taxable distribution and potentially subject to early withdrawal penalties. Recharacterization inherently involves moving funds from one IRA to another, and using a direct transfer bypasses the complexities and risks associated with the 60-day rule.

4. Consult a Professional

The rules surrounding IRAs and recharacterizations can be intricate. Mistakes can be costly. It is always prudent to consult with a qualified tax advisor or financial planner before initiating a recharacterization. They can help you assess your specific situation, determine if recharacterization is the right strategy for you, and ensure that the process is executed accurately and in compliance with all IRS regulations.

In conclusion, an IRA recharacterization is a powerful but specialized financial tool. It offers a mechanism to correct initial IRA contribution errors or to strategically adjust your retirement savings based on evolving circumstances or tax expectations. By understanding the mechanics, timing, and implications, individuals can leverage recharacterization to optimize their retirement planning and navigate the complexities of their IRA investments with greater confidence.