An insurance producer license is a fundamental requirement for individuals who wish to sell, solicit, or negotiate insurance policies in a particular state. This license, often referred to as an insurance agent license, signifies that the holder has met the necessary educational and examination requirements established by the state’s department of insurance. It is a legal authorization granted by a state government that permits individuals to act as intermediaries between insurance companies and consumers. Without this license, engaging in any insurance-related sales activities would be considered illegal and subject to significant penalties. The licensing process is designed to ensure that only competent and ethical individuals are allowed to advise the public on matters of insurance, protecting consumers from fraud and misrepresentation.

The role of an insurance producer extends beyond merely selling policies. Licensed producers are expected to understand the nuances of various insurance products, assess the needs of their clients, and recommend suitable coverage. This often involves a deep dive into risk management principles, policy provisions, and regulatory compliance. The insurance industry is heavily regulated to safeguard policyholders, and the producer license is a key component of this regulatory framework. It establishes a level of accountability and professionalism within the industry, fostering trust between consumers and those who provide insurance solutions.

Understanding the Role and Responsibilities of an Insurance Producer

The primary function of an insurance producer is to connect individuals and businesses with appropriate insurance coverage that meets their specific needs and risk profiles. This involves a multifaceted approach that includes client consultation, needs assessment, product knowledge, policy explanation, and ongoing client service.

Client Consultation and Needs Assessment

A crucial first step for any insurance producer is to engage in thorough consultation with potential clients. This process involves actively listening to the client’s concerns, understanding their current situation, and identifying potential risks they may face. For individuals, this could involve assessing life circumstances, financial goals, and family responsibilities. For businesses, it requires understanding the nature of their operations, assets, liabilities, and industry-specific risks. A skilled producer uses this information to conduct a comprehensive needs assessment, pinpointing the exact types and levels of coverage required. This is not a one-size-fits-all approach; rather, it demands a personalized strategy tailored to each client’s unique circumstances.

Product Knowledge and Recommendation

Once the needs are understood, the producer must leverage their extensive knowledge of the diverse range of insurance products available. This includes, but is not limited to, life insurance, health insurance, property and casualty insurance (such as auto, home, and business liability), and specialized lines like disability or long-term care insurance. Each product has its own set of features, benefits, limitations, and exclusions. The producer’s responsibility is to explain these details clearly to the client, ensuring they comprehend what they are purchasing. Based on the needs assessment, the producer then recommends the most suitable policies, often comparing options from different insurance carriers to find the best value and coverage. This recommendation must be made in the client’s best interest, free from undue influence or pressure to sell a particular product for personal gain.

Policy Explanation and Administration

Beyond the initial sale, insurance producers play a vital role in explaining the intricacies of the purchased policy. This includes clarifying policy terms, conditions, definitions, deductibles, premiums, and claim procedures. Many clients may find insurance contracts complex, and it is the producer’s duty to demystify this information, ensuring the client understands their rights and obligations. Furthermore, producers often assist with the administrative aspects of insurance, such as submitting applications, coordinating with underwriting departments, and facilitating policy delivery. They may also handle policy endorsements or changes requested by the client over time and are often the first point of contact for clients experiencing a claim, guiding them through the claims process and advocating on their behalf.

The Licensing Process: Requirements and Examinations

Obtaining an insurance producer license is not a simple matter of applying. It involves a structured process designed to verify an individual’s qualifications and commitment to ethical conduct. This process typically involves pre-licensing education, a rigorous examination, and the submission of an application to the state’s regulatory body.

Pre-Licensing Education

Most states mandate that prospective insurance producers complete a specific number of hours of pre-licensing education. These courses cover fundamental insurance principles, state-specific insurance laws and regulations, ethics, and the various types of insurance products that the applicant intends to sell. The curriculum is designed to provide a solid foundation of knowledge necessary to pass the licensing exam and to operate competently in the insurance marketplace. The required hours can vary by state and by the specific lines of authority the applicant seeks (e.g., life, health, property, casualty). Some states may offer exemptions from pre-licensing education for individuals who hold certain professional designations or have prior relevant experience, though this is not universal.

Licensing Examinations

Following the completion of pre-licensing education, candidates must pass a comprehensive licensing examination administered by the state or a designated testing service. These exams are designed to test the applicant’s understanding of the material covered in the pre-licensing courses, as well as their knowledge of state insurance laws and regulations. The exams typically consist of multiple-choice questions and are timed. Passing scores are set by the state and vary depending on the specific exam. Failing an exam usually requires retaking the course or parts of it, and then retaking the exam, often with additional fees. The difficulty of these examinations underscores the importance of thorough preparation and a strong grasp of insurance principles.

Application and Background Checks

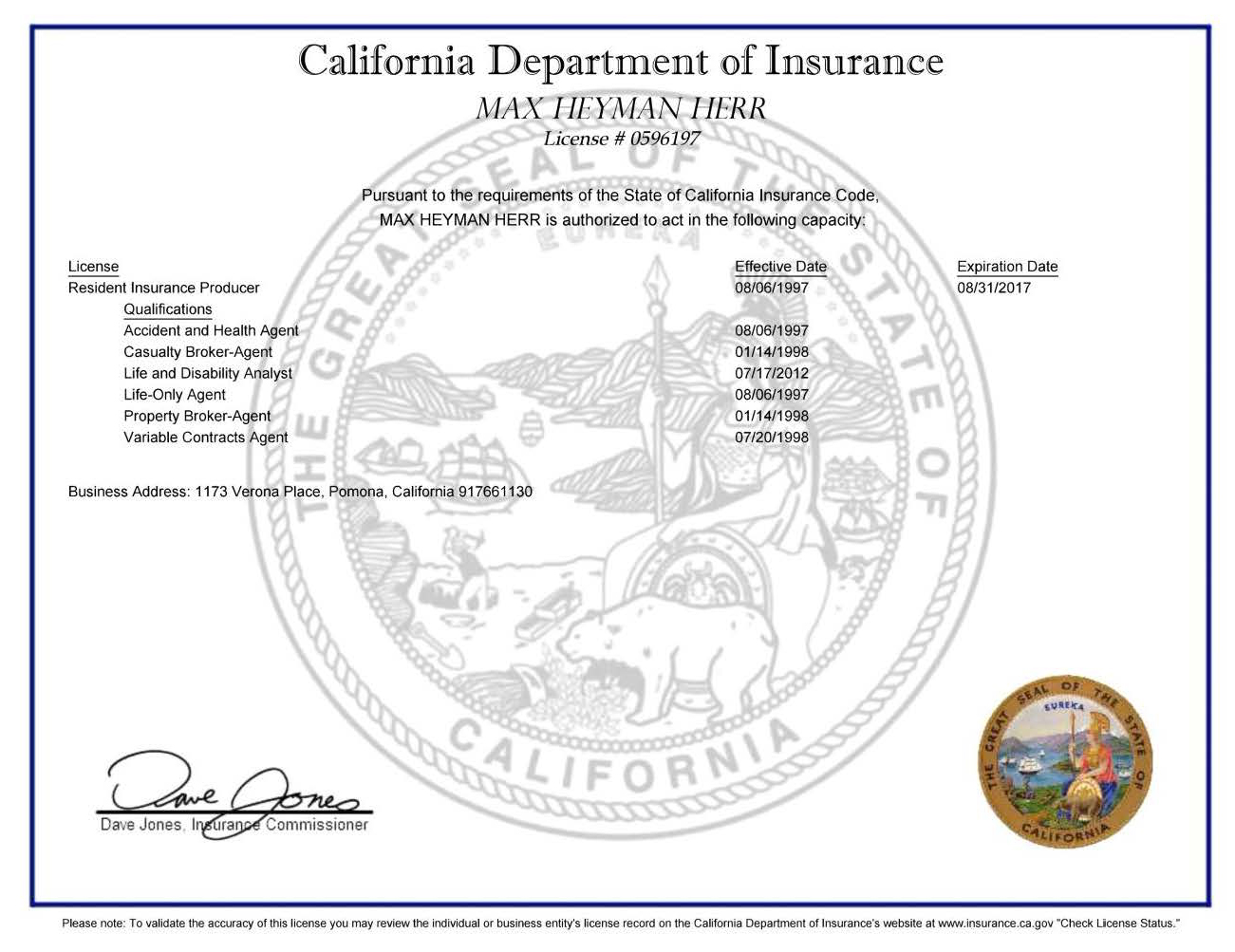

Once the applicant has successfully passed the examination, they must submit a formal application for an insurance producer license to the state’s department of insurance. This application typically requires personal information, details about any criminal history, and disclosure of any professional licenses held in other states. Most states conduct a background check, including fingerprinting and a review of criminal records, to ensure the applicant meets the character and fitness requirements for holding a license. Honesty and transparency in the application process are paramount, as any misrepresentation can lead to denial of the license or disciplinary action if discovered later.

Types of Insurance Producer Licenses and Lines of Authority

The insurance industry is diverse, and the type of license an individual obtains generally corresponds to the specific types of insurance they are authorized to sell. These are often referred to as “lines of authority.”

Life and Health Insurance Producer Licenses

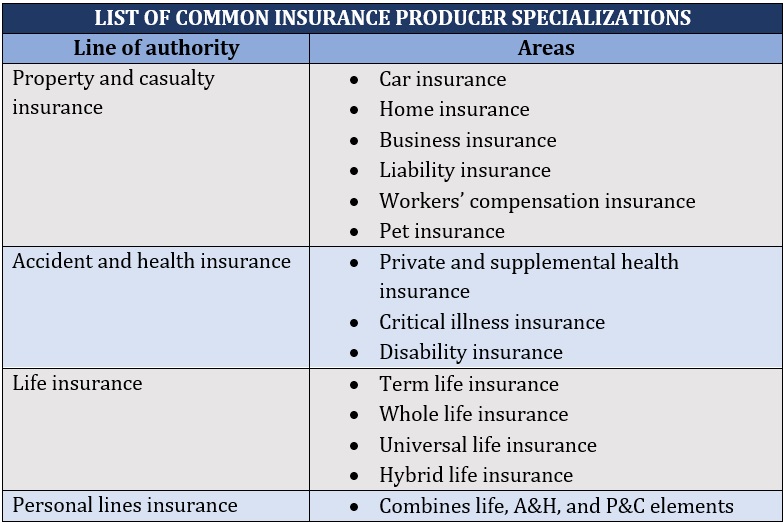

A producer licensed for life insurance is authorized to sell policies that provide death benefits to beneficiaries upon the death of the insured. This includes term life, whole life, universal life, and other permanent life insurance products. A health insurance producer license permits the sale of policies that cover medical expenses, hospitalization, prescription drugs, and other healthcare-related costs. This also includes individual and group health insurance plans, as well as critical illness and long-term care insurance that has a health component. Often, states allow producers to obtain a combined Life and Health license, enabling them to offer both types of coverage.

Property and Casualty Insurance Producer Licenses

This category covers a broad spectrum of insurance products designed to protect tangible assets and cover liability. A property insurance license allows producers to sell policies that protect against damage or loss to real property (like homes and commercial buildings) and personal property (like vehicles and valuable possessions). Casualty insurance, often bundled with property insurance as “Property and Casualty” (P&C), deals with liability. This includes auto insurance, homeowners insurance (which includes both property and liability components), business liability insurance, workers’ compensation insurance, and umbrella policies that provide additional liability coverage. Producers often specialize in either personal lines (serving individual consumers) or commercial lines (serving businesses).

Other Specialized Licenses

Beyond the primary categories, there are other specialized insurance producer licenses. For example, a producer might obtain a license for Variable Life and Variable Annuities, which requires not only an insurance license but also a securities license (such as a Series 6 or Series 7) from the Financial Industry Regulatory Authority (FINRA). This is because these products involve investment components. Other specialized licenses can include those for title insurance, surplus lines insurance (for risks that standard insurers won’t cover), crop insurance, or specific types of risk management services. The need for these specialized licenses arises from the unique nature and regulatory requirements of the insurance products they cover.

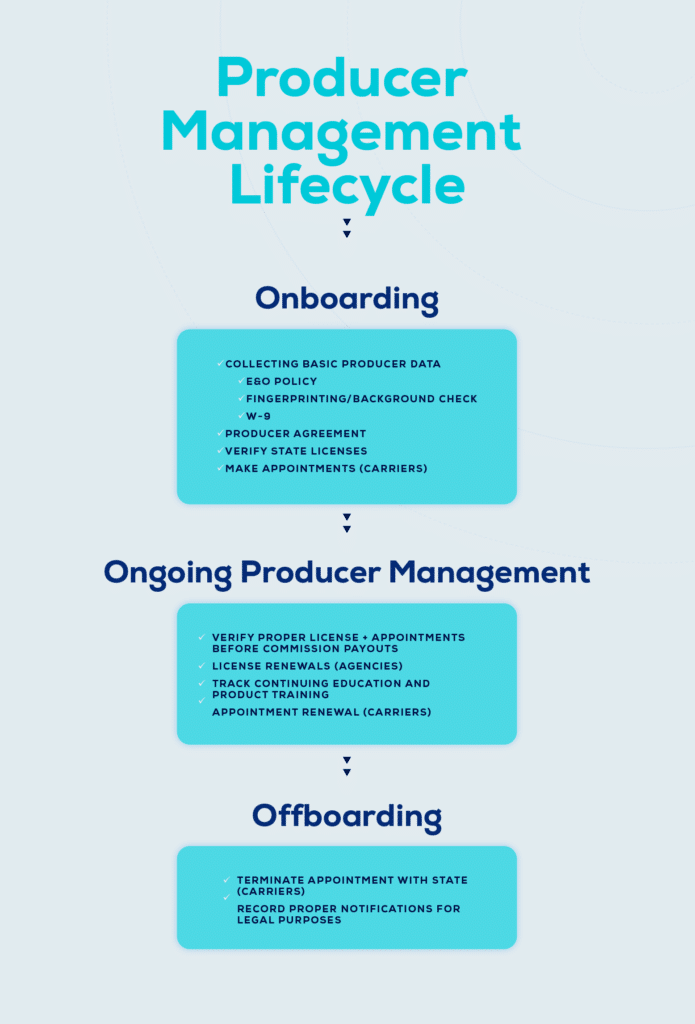

Maintaining and Renewing an Insurance Producer License

Holding an insurance producer license is not a permanent grant. It requires ongoing commitment to professional development and adherence to regulatory standards. Producers must actively maintain their licenses through continuing education and timely renewals.

Continuing Education (CE) Requirements

To ensure that licensed producers remain knowledgeable about evolving insurance products, regulations, and industry best practices, states mandate continuing education. After obtaining their initial license, producers are required to complete a certain number of CE hours within a specified period, typically every two years. These courses cover a variety of topics, including ethics, state laws, new product developments, and risk management. Completing CE hours is a prerequisite for license renewal. Failure to meet these requirements can lead to a lapse in licensure, requiring the producer to go through the full licensing process again.

License Renewal and Compliance

Insurance producer licenses have an expiration date, and they must be renewed periodically, usually every two years. The renewal process typically involves submitting a renewal application, paying a fee, and demonstrating completion of the required continuing education hours. Beyond renewal, producers must also maintain compliance with all state insurance laws and regulations. This includes adhering to ethical sales practices, maintaining accurate records, and responding promptly to client inquiries and complaints. Violations of these regulations can result in disciplinary actions from the state department of insurance, ranging from fines to license suspension or revocation. Staying current with industry trends and ethical standards is crucial for long-term success and maintaining the integrity of the insurance profession.