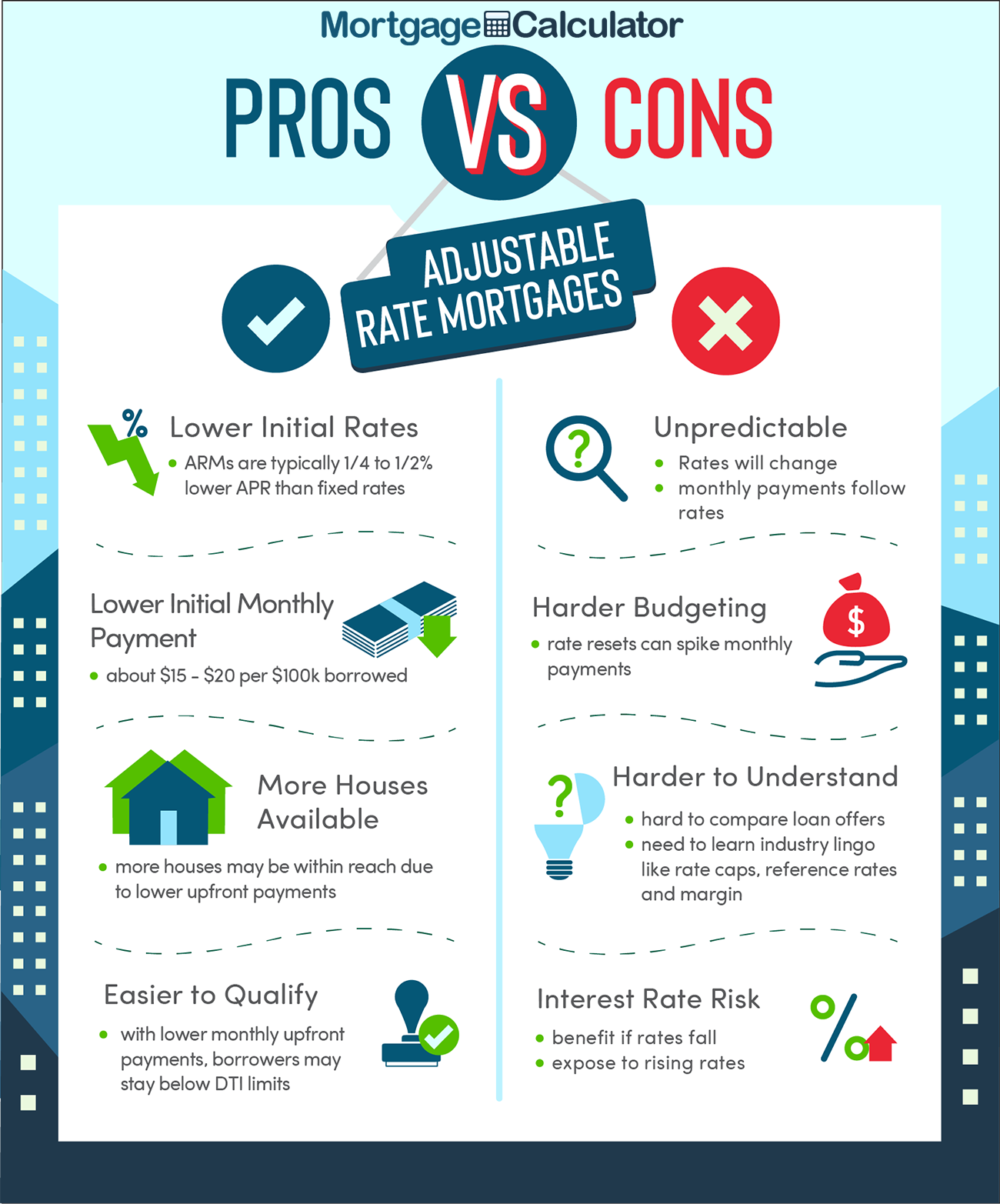

An Adjustable Rate Mortgage (ARM) is a type of home loan where the interest rate can change periodically, unlike a fixed-rate mortgage where the rate remains the same for the entire loan term. This inherent variability is often perceived as a risk, but it also presents a distinct advantage for certain borrowers: lower initial interest rates and, consequently, lower initial monthly payments.

This primary advantage stems from the way lenders price ARMs. Lenders generally offer ARMs with a lower introductory interest rate compared to fixed-rate mortgages. This is because they are transferring some of the interest rate risk to the borrower. If market interest rates rise, the borrower’s rate will also likely rise, increasing their monthly payments. Conversely, if market rates fall, the borrower could benefit from lower payments. For borrowers who anticipate moving, refinancing, or experiencing a significant income increase within the initial fixed period of the ARM, this lower starting cost can be a substantial financial benefit.

The Mechanics of an Adjustable Rate Mortgage

To fully appreciate the advantage of an ARM, understanding its structure is crucial. ARMs are characterized by an initial fixed-rate period followed by a period where the interest rate adjusts. The terms of an ARM are typically presented with a series of numbers, such as 5/1 ARM or 7/1 ARM. The first number indicates the number of years the initial interest rate is fixed, and the second number (always ‘1’ in common ARMs) indicates how often the rate will adjust after the fixed period. For instance, a 5/1 ARM has an interest rate that is fixed for the first five years and then adjusts annually thereafter.

Initial Fixed-Rate Period

During the initial fixed-rate period, the interest rate on the ARM remains constant, providing a predictable monthly principal and interest payment. This predictability is a significant comfort for many homeowners, especially during the early years of homeownership when budgets are often tight. The key advantage here is that this initial rate is typically lower than what would be offered on a comparable fixed-rate mortgage at the same point in time. This lower rate translates directly into a lower monthly housing expense.

Adjustment Period and Rate Caps

Once the initial fixed-rate period concludes, the interest rate on the ARM begins to adjust. These adjustments are tied to a specific financial index, such as the Secured Overnight Financing Rate (SOFR) or the U.S. Treasury Constant Maturity Rate. The lender then adds a “margin” to this index to determine the new interest rate. Crucially, ARMs come with rate caps that limit how much the interest rate can increase at each adjustment and over the lifetime of the loan.

- Periodic Adjustment Cap: This cap limits how much the interest rate can increase or decrease at each adjustment period. For example, a common cap might be 2%, meaning the rate cannot increase by more than 2 percentage points at any single adjustment.

- Lifetime Cap: This is the maximum interest rate the loan can ever reach over its entire term. This provides a ceiling on potential payment increases, offering a degree of long-term certainty, albeit at a higher potential rate.

These caps are vital for risk management and are a key feature that makes ARMs more palatable to borrowers. They prevent unpredictable and potentially crippling spikes in monthly payments.

Why Lower Initial Payments Matter

The advantage of lower initial monthly payments with an ARM is multifaceted and can significantly impact a borrower’s financial situation, especially in the short to medium term.

Increased Affordability

For many individuals and families, the ability to secure a home loan with a lower initial payment can be the deciding factor in their homeownership journey. A lower monthly payment frees up cash flow, which can be allocated to other important financial goals, such as saving for retirement, investing, paying down other debts, or covering the unexpected costs associated with homeownership. This increased affordability can allow borrowers to purchase a more desirable home or a home in a more sought-after location than they might otherwise be able to afford with a higher fixed-rate payment.

Financial Flexibility and Strategic Planning

Borrowers who anticipate significant life changes within the first few years of their mortgage often find ARMs particularly advantageous. These changes could include:

- Relocation: If a borrower expects to move for a job or other reasons within the initial fixed-rate period of the ARM, they can benefit from the lower payments for the duration they own the home and then sell the property before the rate begins to adjust.

- Refinancing: A borrower might take out an ARM with the intention of refinancing into a fixed-rate mortgage later, perhaps after their income has increased or if interest rates decline significantly. The lower initial rate allows them to build equity or save money during this interim period.

- Income Growth: Individuals with rapidly growing careers may find that their income will increase substantially before the ARM’s adjustment period begins. This anticipated income growth can make them comfortable with the potential for future payment increases, as they will be better positioned to handle them.

The initial savings from a lower ARM rate can be reinvested, accelerating wealth accumulation or providing a financial cushion for these anticipated transitions.

Potential for Benefit if Rates Decline

While the primary advantage is the lower initial rate, ARMs also offer the potential to benefit from falling interest rates. If market interest rates decrease after the initial fixed period, the borrower’s interest rate on the ARM will also likely decrease, leading to lower monthly payments. This is a significant departure from a fixed-rate mortgage, where the borrower is locked into their current rate even if market rates fall. In such a scenario, the ARM holder could see their housing costs decrease, further enhancing their financial flexibility.

Who Benefits Most from an ARM’s Advantage?

The advantage of an ARM is not universal. It is most beneficial for borrowers who are:

- Short-Term Homeowners: Individuals who plan to sell their home within the initial fixed-rate period can take full advantage of the lower payments without ever facing the risk of rate increases.

- Confident in Future Income Growth: Those who expect their income to rise significantly before the ARM’s adjustment period can comfortably absorb potential payment increases.

- Savvy Investors: Borrowers who plan to strategically refinance their mortgage or reinvest the savings from lower initial payments can leverage the ARM to their financial advantage.

- Seeking Maximum Initial Affordability: For those whose purchasing power is stretched, the lower initial payments of an ARM can make homeownership attainable.

It is crucial for potential borrowers to carefully assess their personal financial situation, future income projections, and housing plans before opting for an ARM. A thorough understanding of the ARM’s structure, including its caps and adjustment triggers, is paramount to making an informed decision and truly capitalizing on the advantage of lower initial payments.