While seemingly a straightforward question, understanding the nuances of your debit card’s account number is crucial for both security and practical transaction management. This number, often confused with other card identifiers, plays a distinct and vital role in connecting your plastic payment tool to your underlying bank account. This article will demystify the account number associated with your debit card, differentiating it from other prominent numbers and explaining its significance in the digital and physical realms of commerce.

Differentiating Your Debit Card Numbers

It is common to encounter a variety of numbers on or associated with your debit card. To truly grasp the function of the account number, it’s imperative to distinguish it from other key identifiers.

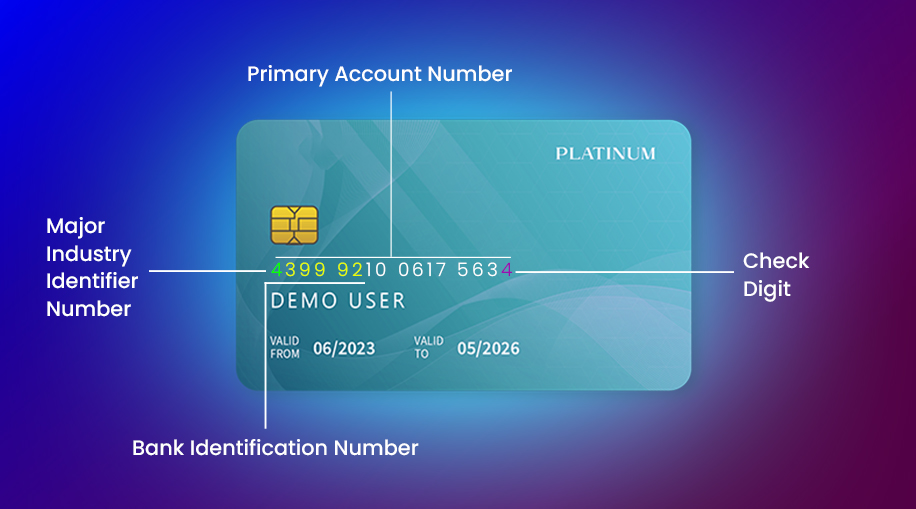

The Primary Card Number (PAN)

The most prominent number displayed on the face of your debit card is the Primary Account Number, or PAN. This is typically a 16-digit number, often embossed or printed in raised font. The PAN is unique to your specific debit card and is used for most point-of-sale transactions and online purchases. When you swipe or insert your card, or enter its details online, it is this PAN that the payment network (like Visa or Mastercard) uses to identify the transaction request. It’s a critical piece of information for authorizing payments and ensuring funds are debited from your account.

However, the PAN is not your bank account number. While it’s intrinsically linked to your account, it serves as a proxy for initiating transactions rather than a direct gateway to your funds. If your card is lost or stolen, the PAN is a primary piece of information that needs to be protected and reported. Cancelling the card associated with a specific PAN effectively severs its connection to your bank account, preventing unauthorized transactions using that particular card.

The Expiration Date

Another critical piece of information on your debit card is the expiration date, usually presented in a MM/YY format. This date signifies when the card will no longer be valid for transactions. Once a card expires, it must be replaced by your bank with a new card, which will likely have a new PAN and potentially a new security code. The expiration date is essential for online and phone transactions, as it helps merchants verify that the card is still active.

The Security Code (CVV/CVC)

The Card Verification Value (CVV) or Card Verification Code (CVC) is a 3 or 4-digit number found on the back of most debit cards (or on the front of some American Express cards). This code is an additional security measure, particularly for “card-not-present” transactions (online or over the phone). Merchants are generally prohibited from storing CVV/CVC information after authorization, making it a more secure piece of data to transmit for transactions where physical card presentation isn’t possible. It helps to confirm that the person making the purchase is in physical possession of the card.

The Bank Account Number

This is where the distinction becomes critical. The bank account number is the unique identifier assigned to your specific deposit account (checking or savings) at your financial institution. Unlike the PAN, which is associated with the physical card, the account number is tied directly to your financial holdings. It is not typically printed on the debit card itself for security reasons.

When you use your debit card, the PAN, in conjunction with other security protocols, directs the transaction request to your bank. Your bank then uses its internal systems to link that transaction to your specific bank account number to debit the necessary funds. In essence, the debit card is a convenient access tool to your bank account, and the account number is the fundamental address of that account.

Where to Find Your Debit Card Account Number

Given that the bank account number is not usually displayed on the debit card itself, you might wonder how to locate it when necessary. Fortunately, there are several reliable methods.

Online Banking Portals

The most common and convenient way to find your bank account number is through your bank’s online banking portal or mobile app. After logging in securely, you can usually navigate to a section detailing your account information. Often, this will prominently display your full account number for checking and savings accounts linked to your debit card. Banks provide this access for legitimate purposes, such as setting up direct deposits or bill payments.

Bank Statements

Your physical or electronic bank statements are another reliable source for your account number. Each statement will clearly list the account number to which it pertains. This is a traditional method and remains effective for retrieving the information. If you receive paper statements, it’s advisable to store them securely, and if you opt for electronic statements, ensure your digital storage is protected.

Visiting a Branch or Calling Customer Service

For those who prefer or require direct assistance, visiting a local branch of your bank is a surefire way to obtain your account number. A teller or customer service representative can verify your identity and provide you with the necessary information. Similarly, calling your bank’s official customer service line and undergoing their verification process will allow you to retrieve your account number over the phone. Always ensure you are speaking with an official representative and providing sensitive information only through secure channels.

The Significance of Your Account Number

The bank account number associated with your debit card is more than just a string of digits; it’s the key to your financial domicile. Its significance extends to various aspects of financial management and security.

Direct Deposit and Electronic Fund Transfers (EFTs)

Your account number is fundamental for receiving funds electronically. Employers use it for direct deposit of salaries, government agencies for benefits, and tax refunds. Similarly, when you initiate electronic bill payments from your bank account or receive money via services like Zelle or Venmo, your account number (often alongside your bank’s routing number) is the essential identifier for the transfer.

Setting Up Recurring Payments

Many subscription services, utility companies, and other billers allow you to set up automatic payments directly from your bank account. This requires providing your account number and routing number. This simplifies financial management by ensuring bills are paid on time, avoiding late fees and service interruptions.

Security and Fraud Prevention

While your debit card offers a layer of protection, your bank account number is a more sensitive piece of information. It represents direct access to your funds. Therefore, it’s crucial to protect your account number vigilantly. Sharing it only with trusted institutions and individuals, and being wary of phishing attempts or unsolicited requests for this information, is paramount. Banks employ sophisticated fraud detection systems that monitor transactions linked to your account number.

Linking Accounts

Your account number is also used when linking your bank account to other financial services, such as investment platforms, loan applications, or third-party payment processors. This allows for seamless money movement between different financial entities.

Protecting Your Debit Card and Account Number

The distinction between your debit card PAN and your bank account number underscores the importance of a multi-layered approach to financial security.

Protecting Your Debit Card

- Keep it Secure: Treat your debit card like cash. Don’t leave it unattended and be mindful of who sees you use it.

- Report Lost or Stolen Cards Immediately: Contact your bank as soon as you realize your card is missing. Most banks offer 24/7 hotlines for this purpose.

- Monitor Transactions: Regularly review your bank statements and online transaction history for any unauthorized activity.

- Use PINs Wisely: Choose a strong, memorable PIN and avoid easily guessable combinations (e.g., birthdays, sequential numbers). Don’t share your PIN with anyone.

Protecting Your Account Number

- Limit Sharing: Only provide your account number to trusted entities and when absolutely necessary.

- Be Wary of Phishing: Never share your account number in response to unsolicited emails, text messages, or phone calls. Verify the legitimacy of any request.

- Secure Online Access: Use strong, unique passwords for your online banking and enable two-factor authentication whenever available.

- Shred Financial Documents: Dispose of old bank statements and other financial documents securely by shredding them.

In conclusion, understanding the difference between your debit card number and your bank account number is fundamental to managing your finances safely and effectively. While your debit card facilitates convenient access, your bank account number is the direct link to your deposited funds. By safeguarding both pieces of information and utilizing the secure methods provided by your bank, you can confidently navigate the digital and physical landscapes of modern commerce.