A voluntary repossession is a situation where a borrower, unable to meet their loan obligations, chooses to return the secured property to the lender. This contrasts with an involuntary repossession, where the lender seizes the property due to default. While it might seem counterintuitive to willingly give up an asset, a voluntary repossession can offer significant advantages to borrowers facing financial distress, primarily by mitigating further financial penalties and damage to their credit score.

The concept of a voluntary repossession is rooted in the underlying agreement of a secured loan. When you take out a loan to purchase an asset – be it a vehicle, heavy machinery, or even specialized equipment used in various technological fields – that asset typically serves as collateral. This means the lender has a legal claim to the property if you fail to make your payments. In a default scenario, an involuntary repossession can involve towing, legal proceedings, and potentially a deficiency balance, where you still owe the difference between the sale price of the repossessed item and the outstanding loan amount. A voluntary repossession, however, aims to avoid these escalating consequences.

Understanding the Mechanics of Voluntary Repossession

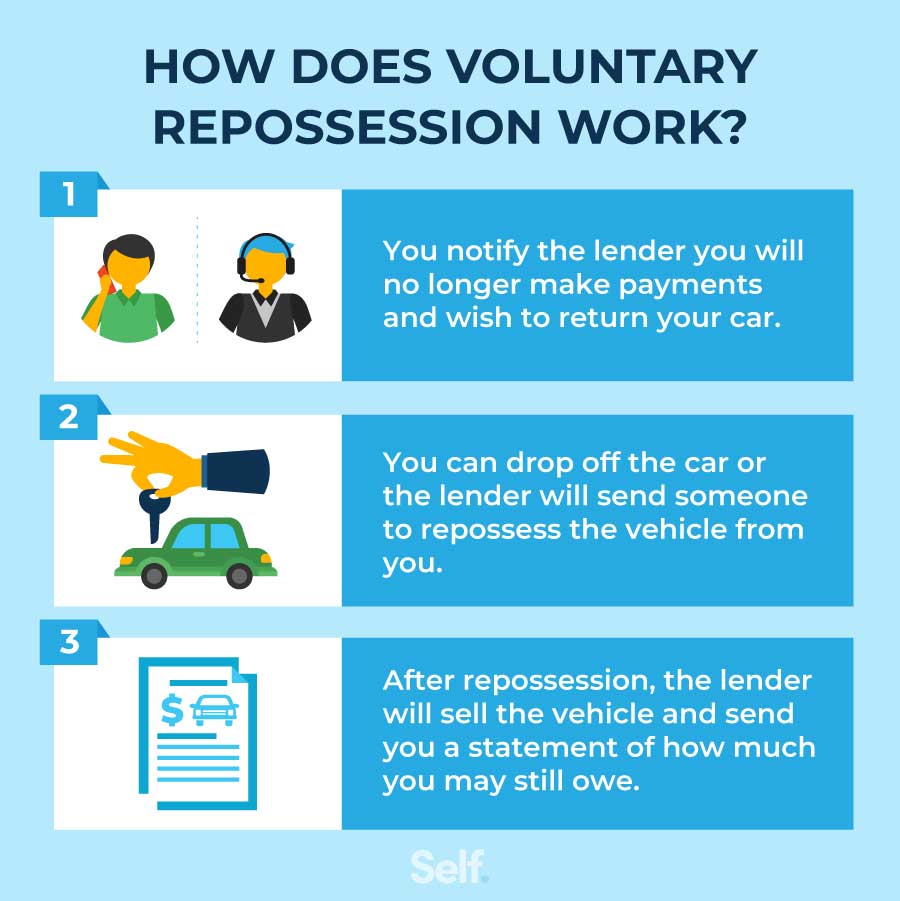

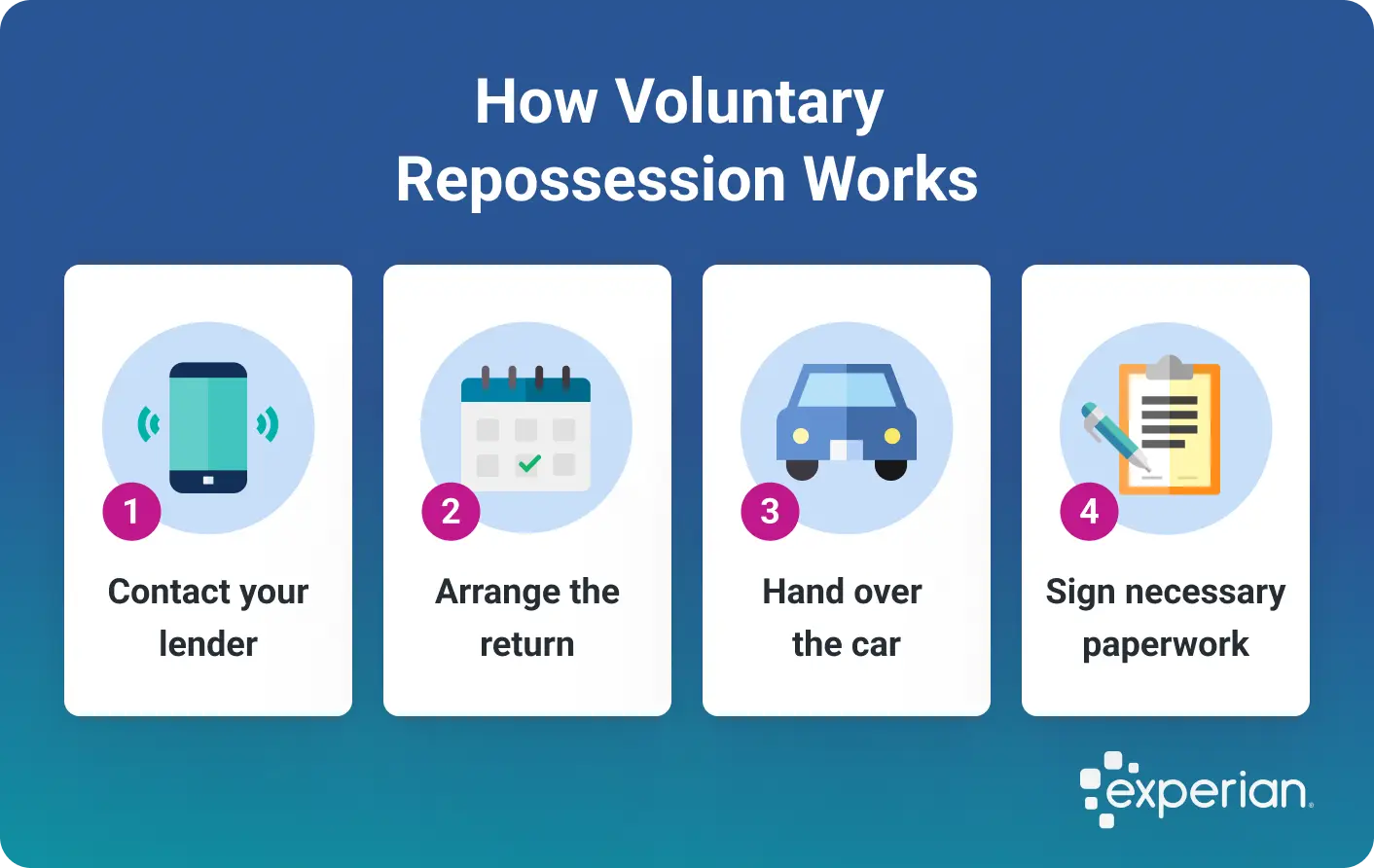

The process of a voluntary repossession begins with the borrower recognizing their inability to continue payments. This might stem from a sudden loss of income, unexpected medical expenses, or a significant change in business operations that impacts cash flow. Instead of waiting for the lender to initiate legal action, the borrower proactively contacts the lender to discuss options.

Initiation and Communication

The first step for a borrower considering a voluntary repossession is to reach out to their lender. This communication should be clear, direct, and honest about the financial predicament. Lenders often prefer a voluntary surrender because it saves them time, legal fees, and the costs associated with locating and repossessing the asset. During this conversation, the borrower can inquire about the specific procedures for voluntary repossession, including the necessary paperwork, the condition in which the asset should be returned, and any potential implications for their credit report.

Asset Condition and Return

The condition of the returned asset is a crucial element in a voluntary repossession. While wear and tear consistent with normal use is generally expected, significant damage caused by neglect or misuse could still lead to financial repercussions. Lenders will typically inspect the asset upon return. It is advisable for borrowers to ensure the property is in the best possible condition to minimize any potential claims for damage beyond normal depreciation. The logistics of returning the asset will also be arranged with the lender, often involving the borrower transporting the item to a designated location or the lender arranging for its pickup.

Paperwork and Legal Release

A formal agreement is typically drawn up to document the voluntary repossession. This document outlines the terms of the surrender, including the release of the borrower from further financial obligations related to the loan, provided all conditions of the surrender are met. It’s essential for the borrower to understand that a voluntary repossession is still a form of loan default, and it will be reflected on their credit report. However, the notation might be less severe than an involuntary repossession, and the absence of further penalties can be a significant benefit. Borrowers should carefully review all documentation before signing and may consider seeking legal counsel to ensure they fully comprehend the terms and their rights.

Advantages of a Voluntary Repossession

While the decision to voluntarily surrender an asset is rarely an easy one, it can present several advantages over an involuntary repossession, particularly for individuals or businesses operating within sectors that rely on specialized equipment or significant capital investment.

Avoiding Further Financial Penalties

One of the primary benefits of a voluntary repossession is the potential to avoid a deficiency balance. In many involuntary repossessions, the proceeds from the sale of the repossessed asset at auction may not cover the full outstanding loan amount. The borrower is then liable for the difference, known as the deficiency balance. By voluntarily surrendering the property, borrowers can sometimes negotiate with the lender to waive or reduce this deficiency, especially if the lender believes they can recover a more favorable price through a private sale or if the asset’s market value is still relatively high. This can significantly lessen the long-term financial burden.

Mitigating Credit Score Damage

Both voluntary and involuntary repossessions will negatively impact a borrower’s credit score. However, the severity of the impact can differ. An involuntary repossession, often perceived as a more adversarial action by the lender, can leave a more significant and lasting scar on a credit report. A voluntary repossession, while still a negative mark, can sometimes be viewed by future lenders as a sign of responsibility and proactivity in addressing financial difficulties. The absence of further legal actions and collection efforts associated with a voluntary surrender can also contribute to a slightly less damaging credit report overall. Furthermore, by avoiding a deficiency balance and subsequent collection activities, the borrower may be able to address the negative mark on their credit report more effectively and rebuild their credit standing sooner.

Control Over the Process

Opting for a voluntary repossession grants the borrower a degree of control over a difficult situation. Instead of waiting for the lender to take action, the borrower can initiate the process, choose the timing of the surrender (within reason and in consultation with the lender), and potentially have a say in how the asset is handled post-repossession. This control can be psychologically empowering during a financially stressful period. It allows the borrower to proactively manage their exit from the loan agreement, rather than being subjected to the lender’s timeline and methods.

When Might a Voluntary Repossession Be Considered?

The decision to pursue a voluntary repossession is highly situational and depends on a thorough assessment of the borrower’s financial standing and the nature of the secured asset. For individuals or businesses reliant on specific types of equipment, understanding the implications is paramount.

Vehicle Loans

Perhaps the most common scenario for voluntary repossession involves vehicle loans. When a car payment becomes unmanageable, and selling the vehicle privately would result in a loss that cannot be absorbed, a voluntary repossession might be considered. This is especially true if the borrower anticipates further financial hardship and wants to avoid escalating costs like late fees, collection charges, and potential legal judgments. The borrower might also opt for this route if they have another vehicle or alternative transportation and the primary vehicle is depreciating rapidly.

Business Equipment and Machinery

Businesses that finance specialized equipment, such as manufacturing machinery, construction vehicles, or high-tech computing hardware, may also find themselves in a position where a voluntary repossession is the most prudent course of action. If the equipment is no longer essential to the business’s operations, is too costly to maintain, or if the business is downsizing, surrendering the equipment can free up capital and eliminate ongoing loan payments. For example, a drone photography company that invested in expensive professional-grade aerial equipment might choose a voluntary repossession if their client base dwindles or if newer, more efficient models make their current fleet obsolete and unmarketable without significant loss. The cost of financing obsolete or underutilized technology can become a drag on a business’s profitability, and a voluntary repossession can be a strategic move to divest of these assets.

Real Estate (Though Less Common Terminology)

While the term “voluntary repossession” is more commonly associated with personal property like vehicles and equipment, the concept of voluntarily returning property to a lender applies to real estate as well, though it’s typically referred to as a “deed in lieu of foreclosure.” If a homeowner or business owner cannot afford their mortgage payments and believes a foreclosure sale will result in significant financial damage, they might negotiate with the lender to transfer ownership of the property directly. This avoids the public record and potentially more severe credit implications of a foreclosure.

Potential Drawbacks and Considerations

Despite its advantages, a voluntary repossession is not without its downsides, and borrowers must weigh these carefully.

Credit Report Impact

As mentioned, a voluntary repossession will appear on a credit report. While it may be less damaging than an involuntary repossession, it is still a negative mark that will likely lower a credit score. This can make it more difficult to obtain new loans, credit cards, or even rent an apartment for several years. The length of time this mark remains on a credit report is typically seven years, though its impact diminishes over time.

Lender Negotiation and Cooperation

The success of a voluntary repossession often hinges on the lender’s willingness to cooperate. Some lenders may be more amenable to negotiation than others. If a borrower is unable to reach an agreement with their lender regarding deficiency balances or other terms, the situation could devolve into an involuntary repossession anyway. It is therefore crucial for borrowers to approach the negotiation with a clear understanding of their goals and the lender’s potential responses.

Emotional and Psychological Toll

Voluntarily giving up a valuable asset can be emotionally difficult. It signifies a failure to meet financial commitments and can lead to feelings of shame or regret. Borrowers must be prepared for the emotional impact and have a support system in place to help them navigate this challenging period.

Conclusion: A Strategic Financial Decision

A voluntary repossession is a tool that can be used by borrowers facing overwhelming debt to mitigate further financial damage. It is a proactive approach that, when handled correctly, can lead to a less severe impact on credit scores and the avoidance of significant deficiency balances. However, it is not a solution that should be entered into lightly. A thorough understanding of the process, potential advantages, and inherent drawbacks is essential. Consulting with financial advisors or legal professionals can provide invaluable guidance in making an informed decision about whether a voluntary repossession is the right path forward when faced with insurmountable loan obligations. It represents a difficult, but sometimes necessary, strategic financial decision aimed at preserving long-term financial health over short-term asset retention.