In an increasingly interconnected global economy, the ability to transfer funds securely and efficiently across borders is paramount. At the heart of this intricate financial web lies a critical identifier: the SWIFT BIC number. Far from being a mere alphanumeric code, the SWIFT BIC (Society for Worldwide Interbank Financial Telecommunication Bank Identifier Code) is a cornerstone of international finance, a technological marvel that streamlines cross-border payments, enhances security, and ensures the accurate routing of billions of transactions daily. Understanding its function is not just for bankers; it’s key to comprehending the digital infrastructure that underpins global commerce and personal remittances. This article delves into the origins, structure, importance, and future of SWIFT BIC numbers as a prime example of enduring financial technology and innovation.

The Cornerstone of Global Financial Communication

The concept of moving money between different countries, banks, and currencies presented a formidable challenge before the advent of standardized systems. Manual processes were slow, error-prone, and inherently insecure. The need for a unified, reliable communication network for financial institutions became evident as globalization accelerated.

Defining SWIFT and BIC

At its core, SWIFT is a cooperative society owned by its member financial institutions. Established in 1973, its primary objective was to replace the antiquated telex system with a standardized, secure, and reliable communication network for financial transactions. SWIFT does not hold funds or manage accounts; instead, it provides the secure messaging platform that banks use to send payment orders, account statements, and other financial instructions to one another. It’s the secure “email system” for banks worldwide.

A BIC, or Bank Identifier Code, is the specific address used within the SWIFT network to identify a particular financial institution. Sometimes referred to as a SWIFT code, it uniquely identifies banks and financial organizations globally. Every bank that participates in the SWIFT network is assigned one or more BICs. This code acts like an international routing number, ensuring that funds sent from one country reach the correct bank in another.

The Problem SWIFT Solved

Before SWIFT, international money transfers relied heavily on manual processes, paper correspondence, and the telex system. This method was not only agonizingly slow, often taking weeks for funds to clear, but also lacked standardization. Each bank might have its own proprietary system or communication method, leading to significant delays, increased costs, and a high risk of errors or fraud. The lack of a universal language or addressing system for financial messages made global banking a labyrinthine task.

SWIFT revolutionized this by introducing a common standard for financial messages and a robust, secure network for their transmission. By creating a uniform messaging format and assigning unique BICs to each participating institution, SWIFT streamlined the entire process. This technological leap dramatically reduced transaction times, lowered operational costs, improved security through encryption and authentication, and fostered greater trust in cross-border financial exchanges. It transformed international banking from a slow, opaque process into a relatively fast, transparent, and dependable operation.

How SWIFT Transactions Work

When you initiate an international bank transfer, for instance, from your account in London to a friend’s account in New York, the process typically involves your bank (the originating bank) sending a SWIFT message to the recipient’s bank (the beneficiary bank). This message contains all the crucial details: the amount, currency, beneficiary’s name, account number, and, critically, the SWIFT BIC of the beneficiary bank.

The SWIFT network acts as the secure conduit for this message. It verifies the identity of the sending bank, encrypts the message, and routes it to the correct beneficiary bank identified by its BIC. Once the beneficiary bank receives the message and verifies its authenticity, it processes the transaction, crediting the funds to the recipient’s account. In some cases, especially when direct relationships between banks don’t exist, intermediary banks might be involved, each identified by their own BICs, facilitating the journey of the funds. This multi-stage process, while appearing complex, happens in a matter of hours or days, a significant improvement over the pre-SWIFT era.

Unpacking the BIC Structure

A SWIFT BIC is not a random string of characters; it follows a precise, standardized format that conveys specific information about the financial institution it identifies. This structured approach is a key innovation, ensuring clarity and minimizing ambiguity across diverse global banking systems.

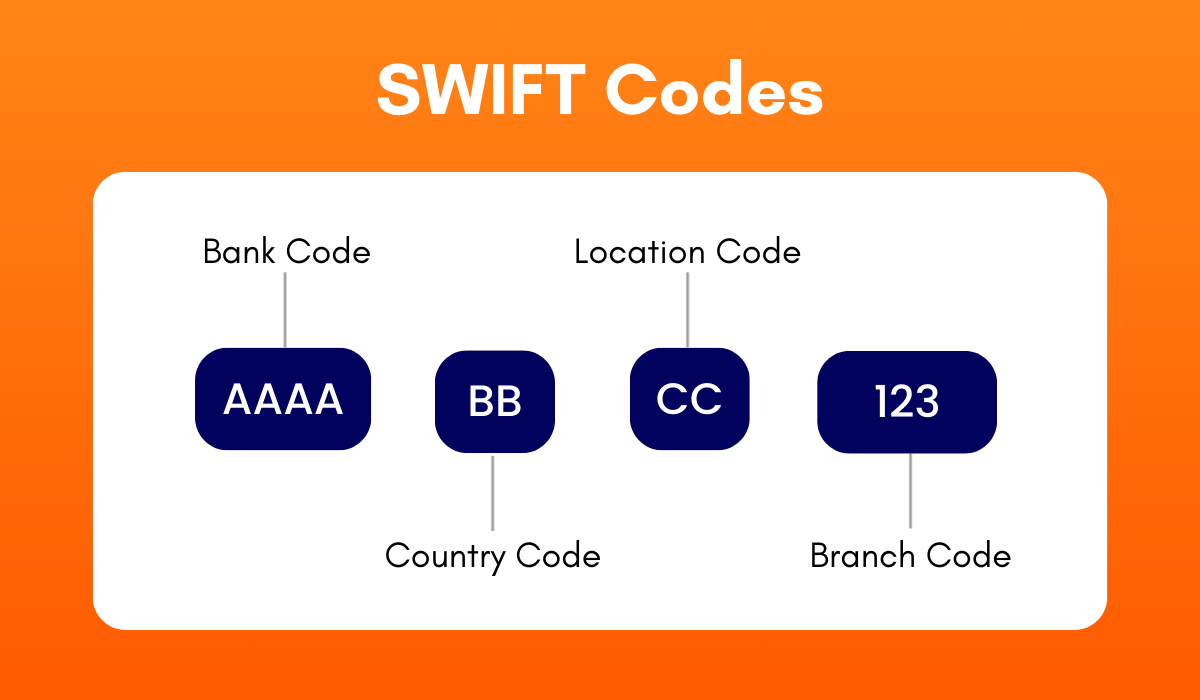

Decoding the 8-Character BIC

The most common and fundamental form of a BIC is an 8-character code, which provides core information about the bank. It is structured as follows:

- Bank Code (4 letters): These first four characters uniquely identify the bank. They are typically an abbreviation of the bank’s name, e.g., “HSBC” for HSBC Bank, “DEUT” for Deutsche Bank.

- Country Code (2 letters): These two characters follow the ISO 3166-1 alpha-2 standard and identify the country where the bank’s head office is located. For example, “US” for United States, “GB” for Great Britain, “DE” for Germany.

- Location Code (2 letters or digits): These two characters specify the city or region where the bank’s branch is located. They can be letters or numbers. For instance, “HH” for Hamburg or “LA” for Los Angeles.

So, an 8-character BIC like DEUTDEFF breaks down as:

- DEUT: Deutsche Bank

- DE: Germany

- FF: Frankfurt

This compact code provides enough information to accurately identify a bank and its country of origin, crucial for routing initial payment instructions.

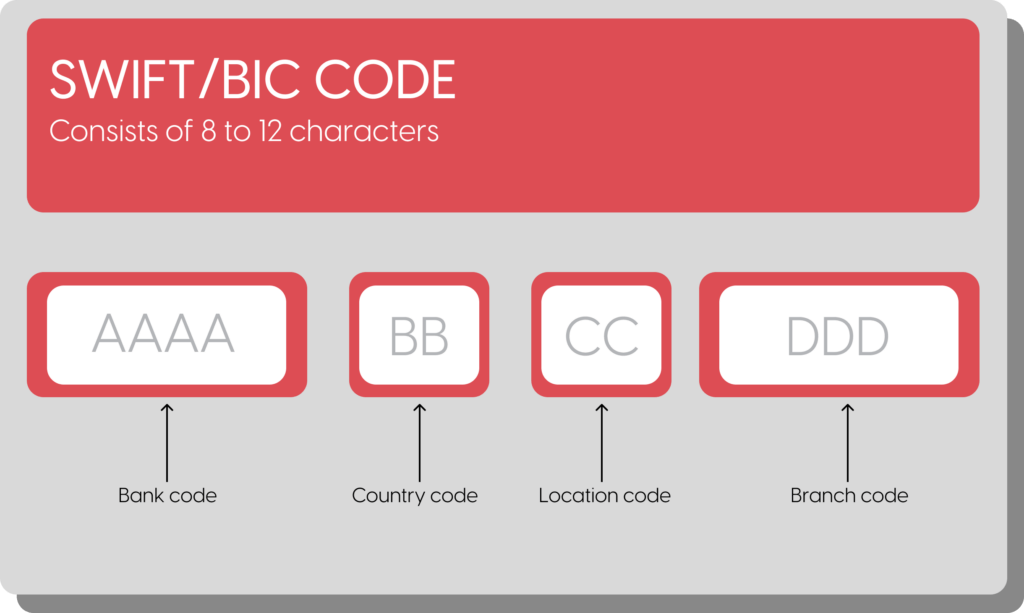

Understanding the 11-Character BIC

While the 8-character BIC identifies the main office or primary branch of a financial institution, an 11-character BIC provides more granular detail, specifically identifying a particular branch or a specific department within the bank.

The 11-character BIC simply extends the 8-character format by adding three additional characters:

- Branch Code (3 letters or digits): These final three characters specify a particular branch, department, or office within the bank. If a bank does not have specific branch codes for a transaction, these characters are often represented by “XXX,” effectively making it an 8-character BIC with an optional suffix.

For example, CHASUS33XXX could represent JPMorgan Chase Bank’s main office in the US. If a specific branch code were needed, it might look like CHASUS33NYC for a New York City branch. The inclusion of the “XXX” is a common convention when only the main office needs to be identified but an 11-character field is required.

Examples of BIC Formats

Let’s look at a few hypothetical examples to illustrate the variations:

- HSBCGB2L: This would identify HSBC Bank in Great Britain (GB), with “2L” possibly indicating London or a specific regional hub.

- CITIUS33: Citibank in the United States (US), with “33” for New York City (their primary hub).

- BARCGB22XXX: Barclays Bank in Great Britain (GB), “22” for London, with “XXX” indicating the main office or unspecified branch.

- RABONL2U: Rabobank in Netherlands (NL), “2U” for Utrecht.

The consistency in this structure is a testament to the innovative design of SWIFT, allowing for global interoperability despite the vast number of financial institutions involved.

Importance and Applications in Modern Finance

The SWIFT BIC number’s significance extends far beyond simply routing messages. It is an indispensable tool that underpins the security, efficiency, and reach of modern financial systems.

Ensuring Accuracy and Security

The primary benefit of BICs lies in their role in ensuring the accuracy of international payments. By providing a universally recognized, machine-readable identifier for each bank, BICs drastically reduce the likelihood of funds being misdirected. This precision is critical in high-volume, high-value financial transactions, where errors can lead to significant financial losses and operational nightmares.

Furthermore, the SWIFT network itself is engineered with robust security protocols, including encryption, authentication, and message validation. BICs are an integral part of this secure ecosystem, as they are part of the verified message structure that travels through the network. This combination of accuracy and security builds trust among financial institutions and their clients, fostering a stable environment for global commerce. The standardization also aids in regulatory compliance, allowing authorities to track and monitor cross-border financial flows more effectively.

Beyond International Transfers

While most commonly associated with international wire transfers, the application of SWIFT BICs extends to various other financial operations:

- Securities Transactions: BICs are used to identify the financial institutions involved in buying, selling, and settling international securities trades.

- Treasury Management: Corporations use BICs for their cross-border cash management and liquidity planning.

- Interbank Communications: Beyond payment instructions, BICs facilitate various types of secure interbank communications, such as account statements, foreign exchange confirmations, and collection notices.

- Foreign Exchange (FX) Markets: In the vast global FX market, BICs identify the banks involved in currency trades, ensuring that the correct parties receive and deliver the respective currencies.

These diverse applications highlight how deeply integrated SWIFT and BICs are into the technological fabric of the global financial system, serving as a foundational element for multiple financial services.

The Role of BICs in SEPA Payments

Even within regional payment systems, BICs play a role. The Single Euro Payments Area (SEPA) simplifies euro-denominated bank transfers within Europe. While SEPA aims to make domestic and cross-border euro payments feel like domestic ones, requiring only an IBAN (International Bank Account Number) for most transactions, BICs are still foundational. In the early stages of SEPA adoption, BICs were often required alongside IBANs for international euro transfers, particularly for reaching banks outside the immediate SEPA zone or for certain types of payments. Although the mandate for BIC in SEPA credit transfers and direct debits was largely phased out, the underlying SWIFT infrastructure, identified by BICs, remains crucial for banks to communicate and settle these payments at an interbank level. It underscores that even seemingly self-contained regional systems often rely on broader global standards.

SWIFT, BIC, and the Future of Financial Technology

The financial landscape is in constant evolution, driven by technological advancements and changing user demands. SWIFT and BICs, while established technologies, are not static; they continue to adapt and innovate.

Evolution and Adaptability

Since its inception, SWIFT has continuously evolved its messaging standards and network capabilities. The introduction of SWIFT gpi (global payments innovation) is a prime example of this adaptability. SWIFT gpi significantly enhances the speed, transparency, and traceability of cross-border payments, allowing banks to provide end-to-end tracking of payments in real time, akin to tracking a package. This innovation directly addresses some of the long-standing challenges of traditional SWIFT payments, making them faster and more predictable for both financial institutions and their customers.

The underlying BIC system remains essential for gpi, as it still identifies the participants in this enhanced network. This demonstrates SWIFT’s commitment to leveraging its foundational infrastructure while embracing new technologies to meet the demands of a digital-first world.

Comparison with Other Payment Systems (e.g., IBAN)

It’s important to distinguish BICs from other financial identifiers like the IBAN. While a BIC identifies the bank, an IBAN (International Bank Account Number) identifies an individual account within a bank. An IBAN combines a country code, bank identifier (often incorporating part of the BIC’s bank code), and the specific account number, making it a comprehensive identifier for a specific beneficiary account in international payments.

Both IBANs and BICs are critical for international transfers, often used in conjunction. For instance, when sending money to a European account, you’ll typically need both the recipient’s IBAN (to identify their specific account) and the recipient’s bank’s BIC (to identify the bank itself within the SWIFT network). They serve complementary but distinct purposes in the architecture of global financial technology.

Challenges and Emerging Innovations

Despite its robustness, SWIFT and the use of BICs face challenges from emerging financial technologies. Distributed Ledger Technologies (DLT) like blockchain, and the rise of central bank digital currencies (CBDCs), promise instantaneous and potentially lower-cost cross-border payments, directly challenging the existing correspondent banking model that SWIFT supports. Fintech startups are also developing alternative payment rails that bypass traditional intermediaries.

In response, SWIFT is actively exploring these new technologies, looking for ways to integrate them with its existing infrastructure rather than being rendered obsolete. They are experimenting with DLT-based solutions and researching interoperability with CBDCs, aiming to maintain their pivotal role in the future of global payments. The enduring innovation of SWIFT will be in how it continues to adapt to these disruptive forces, potentially by becoming a central hub that connects traditional finance with new digital payment systems.

Practical Implications for Users and Businesses

For individuals and businesses engaged in international transactions, understanding SWIFT BICs is not merely academic; it has direct practical implications. Incorrect information can lead to significant delays, additional fees, or even the loss of funds.

Locating Your Bank’s BIC

Finding your bank’s BIC is usually straightforward. For most international transfers you receive, you’ll need to provide your bank’s BIC to the sender. This information can typically be found:

- On your bank statement: Many banks print their BIC on account statements.

- Through your online banking portal: Log in to your online account; the BIC is often displayed in the account details section.

- On your bank’s official website: Banks usually have a dedicated section for international transfers or FAQs where their BIC is listed.

- By contacting your bank directly: A quick call to customer service will provide the necessary code.

Always ensure you have the correct and complete BIC to avoid issues with incoming international payments.

Common Mistakes to Avoid

Errors with BICs can cause significant headaches:

- Typographical Errors: Even a single incorrect character can cause a payment to be rejected or routed to the wrong bank, leading to delays and investigation fees.

- Using an Outdated BIC: Banks merge, change names, or update their BICs. Always confirm the latest BIC, especially if dealing with a lesser-known or recently merged institution.

- Confusing BIC with IBAN: As discussed, they serve different purposes. Both are often required for international transfers, but using one in place of the other will result in a failed transaction.

- Not including a Branch Code (if required): While “XXX” often suffices for main offices, some transactions or banks may specifically require an 11-character BIC with a valid branch code. Confirm with the recipient if their bank requires a specific branch code.

Double-checking all details before initiating or expecting an international transfer is crucial for a smooth transaction.

The Impact on Cross-Border E-commerce

For businesses operating in the booming cross-border e-commerce space, SWIFT BICs are indirectly vital. While consumers typically use credit cards or digital wallets for online purchases, these payment processors and the underlying banking infrastructure they rely on still use SWIFT for settling funds internationally. Businesses receiving payments from international customers might have their funds routed through banks that utilize SWIFT to bring the money into their domestic accounts.

Moreover, for B2B e-commerce or larger international invoices, direct bank transfers using SWIFT and BICs are common. Businesses must ensure they provide accurate BIC details to their international clients to facilitate prompt payment for goods and services. The reliability and standardization provided by SWIFT BICs allow e-commerce businesses to confidently expand their reach globally, knowing that the financial rails are in place to support their international transactions.

In conclusion, the SWIFT BIC number is far more than just a code; it is a testament to technological innovation in finance. It represents a standardized language and a secure network that has transformed the complexities of international banking into a streamlined process. As global financial interactions continue to evolve, the underlying principles of secure, standardized identification provided by SWIFT and its BIC codes will remain a cornerstone of the interconnected world economy, constantly adapting to new technologies while retaining its fundamental role.