In an era defined by rapid technological advancement, the lines between personal hobbies, professional pursuits, and the innovative application of emerging tech blur with unprecedented speed. For enthusiasts, developers, and entrepreneurs deeply immersed in the world of drones, autonomous systems, AI, and remote sensing – the very essence of Tech & Innovation – understanding and mitigating potential risks is paramount. While the thrill of flight, the precision of mapping, or the insights from thermal imaging are undeniable, these activities also introduce novel liabilities that traditional insurance might not fully address. This is where a personal liability umbrella policy steps in, offering a crucial layer of defense for individuals navigating the often-uncharted territory of technological innovation.

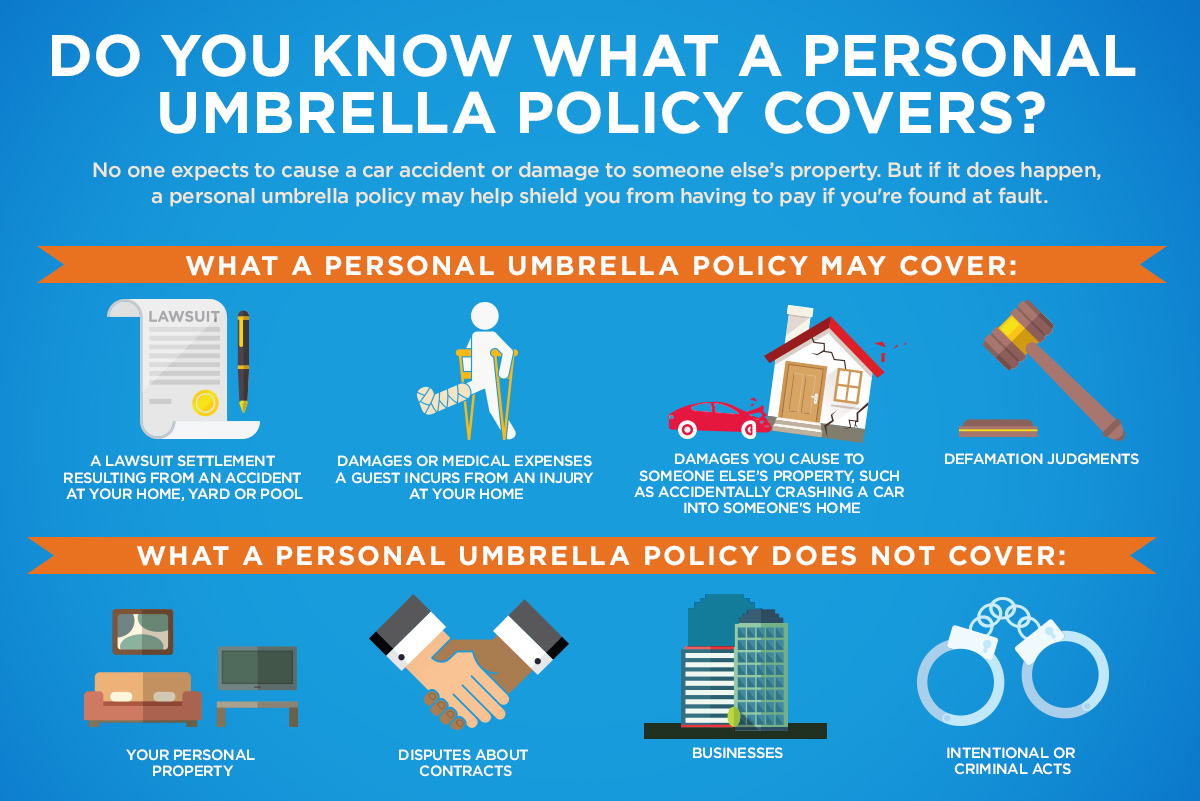

At its core, a personal liability umbrella policy is a form of excess liability insurance designed to provide additional coverage beyond the limits of your standard home, auto, or even specialized drone insurance policies. It acts as a safety net, extending your protection when the costs of a liability claim exceed the maximum payouts of your primary policies. For those engaged in the dynamic field of drone tech, where unforeseen incidents, privacy concerns, or even accidental property damage can lead to substantial financial claims, an umbrella policy is not merely an option but a vital component of a comprehensive risk management strategy. It’s an innovative solution for innovative risks, ensuring that your passion or profession in drone technology doesn’t inadvertently lead to financial ruin.

Understanding the Core: What a Personal Liability Umbrella Policy Offers Innovators

The allure of drone technology lies in its potential to revolutionize industries and enhance personal experiences. However, with this power comes inherent responsibilities and potential liabilities. A personal liability umbrella policy serves as a bulwark against these evolving risks, offering peace of mind to those pushing the boundaries of what’s possible in the aerial domain.

Beyond Standard Coverage: The Unique Risks in Drone Tech

Traditional insurance policies, whether for homeowners or vehicle owners, were designed for a world less populated by autonomous flying machines. While some basic drone insurance might be integrated into a homeowner’s policy or available as a standalone product, these often come with specific limitations, exclusions, and relatively low coverage limits. For instance, a standard homeowner’s policy might cover incidental drone-related damage, but it’s unlikely to account for the complex liabilities arising from commercial drone operations, extensive data collection, or even a hobbyist pushing the limits of FPV racing.

Drone technology introduces unique risk profiles:

- Accidental Damage to Property: A momentary loss of GPS signal or an unexpected gust of wind can send a drone crashing into a neighbor’s roof, an expensive vehicle, or even commercial infrastructure. The repair costs can quickly escalate beyond typical primary policy limits.

- Personal Injury: A drone, particularly larger models used for mapping or delivery, can cause significant harm if it malfunctions or is operated carelessly in proximity to people. Injuries requiring extensive medical treatment or leading to long-term disability can result in astronomical claims.

- Privacy Violations: Equipped with high-resolution cameras, thermal imaging, and advanced sensors, drones have unparalleled surveillance capabilities. Accusations of privacy invasion, even unintentional, can lead to costly legal battles and reputational damage.

- Data Breach/Misuse: For innovators involved in remote sensing, agricultural mapping, or industrial inspection, collecting vast amounts of data is common. A breach of this data, or its accidental misuse, can incur massive liabilities, especially with stringent data protection regulations in place.

- Aviation-Specific Incidents: Operating in airspace, even at low altitudes, carries risks unique to aviation, from interfering with manned aircraft (even if unintentional) to violating no-fly zones, leading to regulatory fines and legal consequences.

A personal liability umbrella policy extends coverage precisely when these primary policies are exhausted or when certain risks fall into grey areas not explicitly covered. It’s a recognition that innovation often outpaces legislation and standard insurance offerings.

Financial Safeguard: Protecting Your Innovations and Assets

The primary benefit of an umbrella policy for tech innovators is its robust financial protection. Imagine a scenario where your experimental autonomous drone, while performing a legitimate remote sensing task, malfunctions and causes a multi-million dollar fire at a commercial facility. Or a misjudged maneuver during an aerial filmmaking shoot results in a serious injury to a bystander. Without adequate coverage, the resulting lawsuits could easily deplete your life savings, future earnings, and even impact your ability to continue your innovative work.

An umbrella policy typically offers coverage ranging from $1 million to $5 million or even more, providing a substantial financial buffer against catastrophic claims. This means that if a liability claim exceeds, for example, the $500,000 limit of your specialized drone insurance or homeowner’s policy, your umbrella policy kicks in to cover the remainder up to its own limit. This not only protects your current assets – your home, investments, and personal property – but also safeguards your future earning potential, preventing wage garnishments or the need to sell off assets to satisfy judgments. For innovators who invest heavily in R&D, specialized equipment, and intellectual property, protecting personal finances becomes critical to sustaining their ventures.

The Unseen Risks: Drone Innovation and Expanding Liability Horizons

The world of drone technology is a double-edged sword: immense opportunity on one side, and evolving, often unprecedented, risks on the other. For those pushing the envelope in AI-driven autonomous flight, intricate mapping projects, or sensitive remote sensing operations, understanding these expanded liability horizons is paramount.

Accidental Damage and Personal Injury: Flying into Uncharted Territory

While accidental damage and personal injury are standard liability concerns, the context of drone operations introduces new complexities. An FPV racing drone, while exhilarating, can reach high speeds, making an accidental collision with property or persons particularly impactful. A commercial drone carrying heavy payloads for construction or agricultural applications presents a greater risk of severe damage or injury if it falls. Moreover, the psychological impact and public perception surrounding drone incidents can amplify claims, especially if the technology is perceived as “dangerous” or “invasive.”

Beyond direct physical damage, there’s the emerging concern of “cyber-physical” incidents. What if an autonomous drone, due to a software glitch or a cyber attack, acts erratically and causes damage? Pinpointing liability in such scenarios involves complex legal analysis, often drawing out legal proceedings and increasing costs. An umbrella policy provides a buffer for these protracted legal battles, covering legal fees and settlements that might quickly exhaust primary coverages.

Privacy Invasion and Data Breaches: New Frontiers of Digital Liability

Drones are powerful data collection platforms. Equipped with advanced cameras, LiDAR, and multispectral sensors, they can capture highly detailed information about properties, individuals, and environments. While invaluable for mapping, surveying, and remote sensing, this capability inherently raises significant privacy concerns. Even if data collection is unintentional or anonymized, accusations of privacy invasion can lead to substantial lawsuits. Consider a drone mapping a remote area that inadvertently captures private moments of individuals on their property; regardless of intent, the legal ramifications can be severe.

Furthermore, for innovators collecting and processing data (e.g., for AI training, environmental monitoring, or precision agriculture), the risk of data breaches or misuse is a growing concern. If your drone system is compromised, and sensitive information is leaked, you could face massive fines under regulations like GDPR or CCPA, alongside civil lawsuits from affected parties. While specialized cyber insurance exists, a personal liability umbrella policy can often provide a broader, foundational layer of defense, particularly for individuals or small startups where personal and business liabilities can overlap significantly. It covers claims alleging libel, slander, defamation, and invasion of privacy, which are highly relevant in the context of drone-based data acquisition.

Commercial Operations & Regulatory Compliance: The Business of Innovation

Many tech innovators transition from hobbyist drone flying to offering commercial services – be it aerial photography, inspection, surveying, or delivery. This shift dramatically increases liability exposure. Commercial operations typically require specific certifications (e.g., FAA Part 107 in the US) and adherence to strict operational guidelines. Breaching these regulations, even inadvertently, can lead to fines, operational suspensions, and heightened liability in the event of an incident.

A personal liability umbrella policy can indirectly support compliance by providing the financial backing needed to navigate the legal complexities that arise from regulatory issues. For instance, if a regulatory violation leads to a third-party claim, the umbrella policy could cover the resulting settlement or judgment after primary policies are exhausted. This broad coverage is particularly vital for small businesses or independent contractors in the drone sector, where personal and business finances are often intertwined, and a single major lawsuit could dismantle an entire venture. It helps innovators confidently pursue their commercial aspirations without constant fear of potentially bankrupting legal challenges.

Who Needs This Coverage in the Drone Tech Ecosystem?

The question of “who needs a personal liability umbrella policy?” in the context of drone technology often boils down to anyone whose activities, whether for recreation or profit, could foreseeably lead to a substantial liability claim. The rapid pace of innovation means that more individuals are engaging with advanced drone capabilities, and thus, more are exposed to new forms of risk.

Hobbyists Pushing Boundaries

The modern drone hobbyist is far removed from the early days of basic RC planes. Today’s hobbyists routinely operate sophisticated UAVs equipped with 4K cameras, GPS navigation, and even rudimentary AI features. They participate in FPV racing, experiment with long-range flights, or engage in aerial photography as a serious passion. While a hobby, the potential for an incident remains very real.

Consider a drone racing enthusiast whose high-speed quadcopter veers off course during an outdoor practice session and crashes into a public park, injuring a bystander. Or an amateur aerial filmmaker capturing stunning vistas, who inadvertently causes property damage to an expensive historical landmark. Even an isolated incident, such as a drone falling from the sky and damaging a vehicle, can lead to substantial repair costs. Standard homeowner’s policies often have very low limits for liability arising from recreational drone use, or specific exclusions for damage caused by “aircraft.” An umbrella policy provides that essential extra layer, protecting personal assets from the significant costs associated with medical bills, property repair, or legal defense when pursuing a passion that pushes technological limits.

Developers and Researchers Testing New Concepts

The core of “Tech & Innovation” lies with developers, engineers, and researchers who are building the next generation of drone technology. This includes those working on advanced autonomous flight algorithms, novel sensor integrations, AI follow modes, or entirely new drone applications. Their work often involves testing prototypes in various environments, sometimes pushing the physical and software limits of their creations.

Testing experimental drone hardware or software inherently carries a higher risk of malfunction or unforeseen consequences. A developer testing a new obstacle avoidance system might accidentally crash a drone into a neighbor’s property or a public space. A research team experimenting with new remote sensing payloads might inadvertently capture sensitive data or cause privacy concerns during field trials. While institutions or employers might offer some level of protection, individual developers or those working on personal projects often find themselves personally exposed. An umbrella policy becomes critical for these innovators, protecting their personal finances from the liabilities that can arise from pushing the boundaries of what’s possible in drone tech. It allows them to innovate with a safety net, without fear that a single experimental mishap could derail their personal and professional future.

Service Providers and Entrepreneurs Leveraging Drones

The commercial drone sector is booming, with entrepreneurs offering services ranging from agricultural mapping and infrastructure inspection to aerial real estate photography and precision delivery. These individuals and small businesses are directly leveraging cutting-edge drone technology for commercial gain, which comes with significantly increased liability exposure compared to hobbyists.

A drone service provider (DSP) conducting a roofing inspection might accidentally drop a tool or the drone itself, causing damage to the property or injury to a resident. A DSP performing a large-scale agricultural mapping project could be accused of trespassing or data misuse. If a delivery drone malfunctions and damages high-value cargo or causes an accident, the financial implications could be severe. While commercial drone insurance exists and is essential for businesses, an umbrella policy provides crucial additional personal liability protection for the business owner. In many small businesses, personal and business assets are closely intertwined, and a catastrophic lawsuit can easily pierce the corporate veil, threatening personal wealth. The umbrella policy ensures that even if commercial insurance limits are exhausted, or if a claim has a personal component, the entrepreneur’s personal assets remain protected, allowing them to rebuild and continue innovating.

How a Personal Liability Umbrella Policy Integrates with Your Tech Ventures

Integrating a personal liability umbrella policy into your risk management strategy for drone tech is a savvy move. It’s not a replacement for specialized drone insurance, but rather a powerful enhancement, ensuring comprehensive protection.

Layering Protection Over Existing Drone Insurance

Think of a personal liability umbrella policy as the capstone of your insurance architecture. Your primary policies – like homeowners, auto, and crucially, any dedicated drone insurance (commercial or hobbyist) – form the foundational layers. These policies provide the first line of defense, covering specific risks up to their stated limits.

However, the nature of drone tech often means that a single incident can lead to damages exceeding these primary limits. This is where the “umbrella” comes into play. Once your primary policy limits are exhausted, your umbrella policy steps in to cover the remaining costs up to its much higher limit, typically millions of dollars. For instance, if your drone insurance covers $1 million for third-party property damage, but a mishap results in $2.5 million in damages, your umbrella policy would cover the additional $1.5 million. This seamless layering ensures that you’re not left personally responsible for the substantial gap between primary coverage and total claim costs, a scenario increasingly common with high-value assets and complex liabilities in the tech world. It’s an efficient way to achieve significantly higher coverage without necessarily purchasing extremely expensive primary policies with higher limits.

Choosing the Right Coverage: Factors for Tech Enthusiasts

Selecting the appropriate personal liability umbrella policy requires careful consideration, especially for individuals actively involved in drone technology and innovation. It’s not a one-size-fits-all solution, and several factors should guide your decision:

- Scope of Activities: Are you a hobbyist, a developer, or a commercial operator? The extent and nature of your drone activities heavily influence your risk profile. More extensive or higher-risk activities (e.g., beyond visual line of sight operations, complex data collection, operations near people) warrant higher umbrella coverage.

- Asset Protection Needs: Assess the total value of your personal assets (home equity, savings, investments, future earnings). Your umbrella policy limit should ideally be high enough to protect these assets from a worst-case scenario lawsuit.

- Primary Policy Limits: Ensure your underlying home, auto, and specialized drone insurance policies have sufficient limits to meet the “attachment point” requirements of the umbrella policy. Most umbrella policies require a certain minimum level of underlying coverage before they will activate.

- Exclusions: Carefully review the policy for any exclusions related to aviation, commercial activities, or specific types of data-related liabilities. While umbrella policies are broad, some might have fine print that could be relevant to advanced drone operations. It’s crucial to understand what is and isn’t covered, especially for activities that push technological boundaries.

- Cost vs. Risk: Umbrella policies are surprisingly affordable given the extensive coverage they provide. Compare quotes from different insurers, but prioritize comprehensive protection over marginal cost savings. The peace of mind and financial security they offer far outweigh the annual premium.

- Provider Expertise: Consider insurers who understand the evolving landscape of technology and its associated risks. They might offer insights or have policies better tailored to individuals engaged in innovative pursuits.

By thoughtfully evaluating these factors, tech enthusiasts and innovators can select a personal liability umbrella policy that provides robust, tailored protection, allowing them to focus on pushing the boundaries of what drone technology can achieve without the looming threat of catastrophic financial liability.

In conclusion, for anyone navigating the exciting yet challenging world of drone tech and innovation, a personal liability umbrella policy is an indispensable safeguard. It transcends the limitations of standard insurance, offering expansive financial protection against the unique and evolving risks associated with autonomous flight, advanced sensing, and data-driven applications. By understanding its benefits and carefully choosing the right coverage, innovators can ensure that their passion for technology remains a source of progress, not peril, securing their personal assets as they shape the future.