In the realm of estate planning and financial security, understanding the intricacies of beneficiary designations is paramount. Among the various designations, the concept of an “irrevocable beneficiary” holds significant weight, particularly in contexts where long-term financial commitments and protection are key. While not directly tied to the operational mechanics of drones or flight technology, the principles behind irrevocable beneficiary designations are crucial for anyone involved in the financial stewardship of assets that might eventually be transferred to a trust or entity, which could, in turn, be related to drone technology development, acquisition, or deployment. For instance, a company specializing in advanced drone mapping solutions might establish a trust for future research and development, naming an irrevocable beneficiary to ensure the continuity of its vision. This article will delve into the definition, implications, and scenarios surrounding irrevocable beneficiaries, focusing on the financial and legal frameworks that govern such designations.

Understanding the Nature of Beneficiary Designations

Before dissecting the specifics of an irrevocable beneficiary, it’s essential to grasp the general concept of a beneficiary designation. In financial instruments such as life insurance policies, retirement accounts, and trusts, a beneficiary is the person or entity designated to receive the assets upon the death of the account holder or policy owner. This designation bypasses the probate process, allowing for a relatively swift transfer of assets. Beneficiary designations are a powerful tool for directing where one’s wealth goes, ensuring that loved ones or chosen organizations are provided for according to the individual’s wishes.

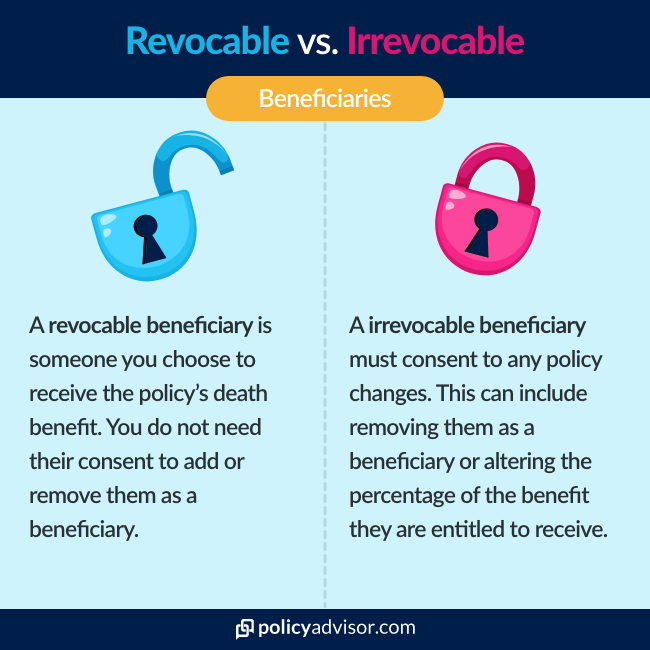

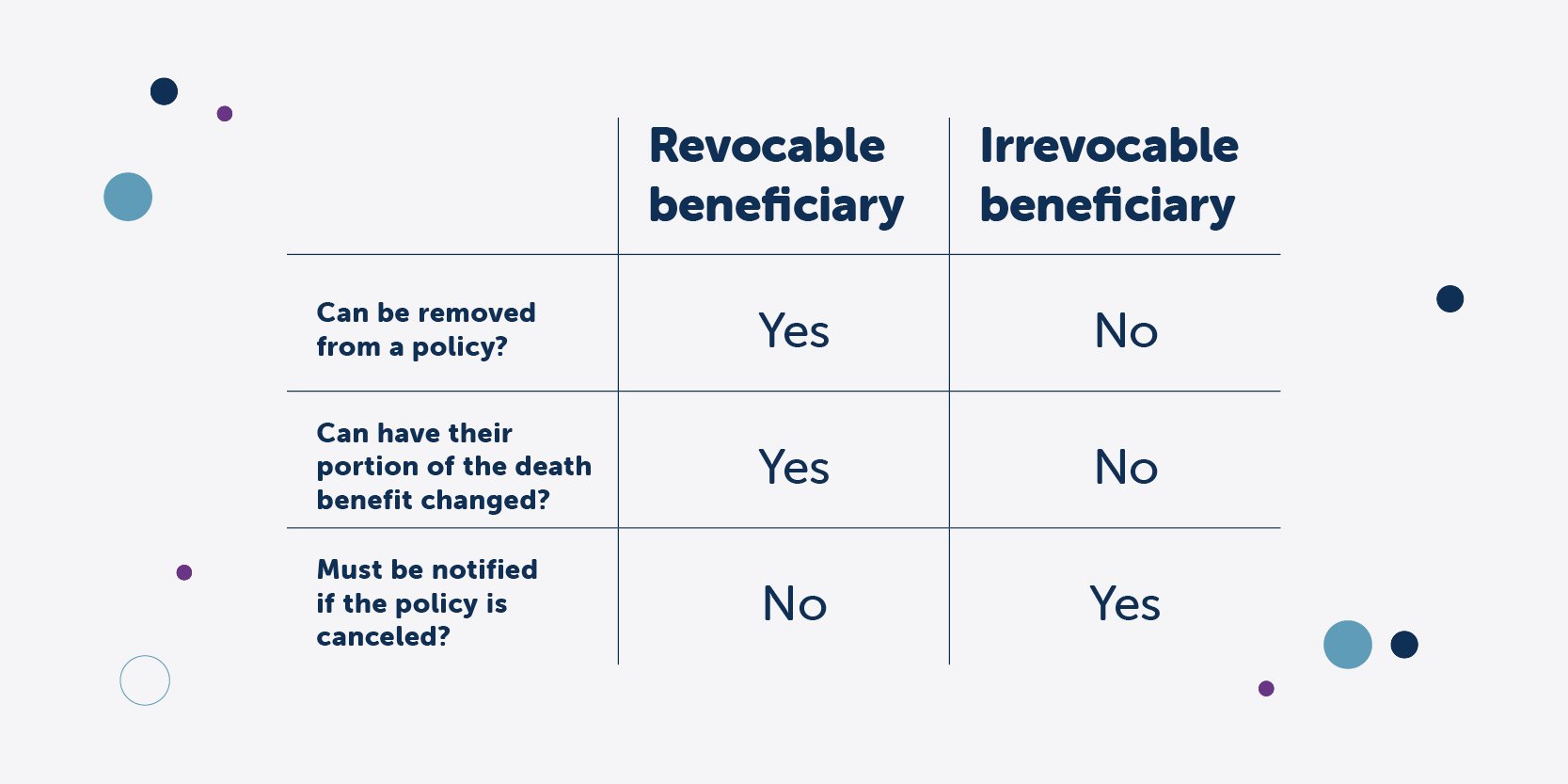

There are typically two primary types of beneficiary designations: revocable and irrevocable.

Revocable Beneficiaries

A revocable beneficiary designation offers the most flexibility. The account holder or policy owner retains the right to change or remove a revocable beneficiary at any time without the beneficiary’s consent. This is the default designation for many financial products and is suitable for situations where the owner anticipates potential changes in their circumstances or relationships. For example, if someone initially names their spouse as a revocable beneficiary on a life insurance policy, they can later change it to their children if they get divorced.

Irrevocable Beneficiaries: A Binding Commitment

An irrevocable beneficiary designation is a legally binding commitment. Once established, the account holder or policy owner cannot change or remove an irrevocable beneficiary without that beneficiary’s explicit consent. This type of designation is often used in specific legal and financial planning scenarios where a permanent and protected allocation of assets is desired. The irrevocability stems from a contractual obligation or a legal agreement that solidifies the beneficiary’s claim.

The primary characteristic of an irrevocable beneficiary is the forfeiture of control by the grantor. This is not a decision to be taken lightly, as it significantly alters the owner’s ability to manage or repurpose the designated assets. The purpose behind such a designation is usually to provide an absolute guarantee of future benefit to the named party.

Scenarios Where Irrevocable Beneficiaries Are Utilized

The implementation of an irrevocable beneficiary designation is typically reserved for situations where a stable and protected financial arrangement is critical. While the direct application in drone technology might be indirect, the underlying financial principles are universally applicable to the entities and individuals that might fund or benefit from such advancements.

Irrevocable Life Insurance Trusts (ILITs)

One of the most common uses of irrevocable beneficiaries is within Irrevocable Life Insurance Trusts (ILITs). In this setup, a trust is established, and the grantor transfers ownership of a life insurance policy to the trust. The trust then names beneficiaries, who are designated as irrevocable. The primary purpose of an ILIT is often to remove the life insurance proceeds from the grantor’s taxable estate, thereby reducing potential estate taxes. The irrevocable nature ensures that the trust and its beneficiaries are permanently protected from the grantor’s creditors and are insulated from changes in the grantor’s personal life. For a venture capital firm investing heavily in drone innovation, establishing an ILIT could be a strategic move to ensure that a portion of their future assets, potentially derived from successful drone ventures, is irrevocably set aside for philanthropic purposes or for the ongoing support of research initiatives.

Child Support and Alimony Obligations

In some jurisdictions, courts may order an individual to name an ex-spouse or child as an irrevocable beneficiary on a life insurance policy or retirement account as a means of securing child support or alimony payments. This ensures that financial support will continue to be provided to the dependent party even if the obligor passes away unexpectedly. The irrevocability guarantees that the funds will be available, providing a crucial safety net for the recipient. Imagine a scenario where a company heavily involved in drone pilot training has a founder who is subject to substantial child support obligations. Naming the children as irrevocable beneficiaries on a key company-owned life insurance policy would ensure those obligations are met regardless of future events.

Charitable Giving and Legacy Planning

For individuals and organizations with a strong commitment to philanthropy, an irrevocable beneficiary designation can be a powerful tool for legacy planning. By naming a charity as an irrevocable beneficiary, donors can ensure that their assets will continue to support a cause they believe in, even after their lifetime. This provides a lasting impact and a guarantee that the charitable mission will be supported. A company pioneering advanced AI for autonomous drone navigation might establish a foundation and name it as an irrevocable beneficiary of a significant portion of its future profits, ensuring that the development of safer and more efficient aerial systems continues to be funded.

Business Succession Planning

In closely held businesses, particularly those in nascent or rapidly evolving sectors like advanced drone services, irrevocable beneficiary designations can play a role in succession planning. For instance, a business owner might set up a trust for their children, naming them as irrevocable beneficiaries of certain business assets or life insurance policies intended to fund the transfer of ownership. This provides a structured and protected pathway for the next generation to inherit and manage the business.

Legal and Financial Implications

The designation of an irrevocable beneficiary carries significant legal and financial implications that must be carefully considered.

Loss of Control and Flexibility

As previously stated, the most profound implication is the relinquishing of control. The grantor can no longer unilaterally alter the beneficiary designation. Any proposed change requires the consent of the irrevocable beneficiary, which they are not obligated to provide. This lack of flexibility means that the grantor must be absolutely certain about their long-term intentions before making such a designation.

Protection from Creditors

One of the key advantages of an irrevocable beneficiary designation is the protection it offers from the grantor’s creditors. Because the assets are legally designated to go to the beneficiary, they are generally shielded from claims by the grantor’s creditors, including those arising from business debts or personal liabilities. This is particularly relevant for companies operating in high-risk or capital-intensive industries like cutting-edge drone development, where financial liabilities can fluctuate.

Estate Tax Considerations

While irrevocable designations, particularly within trusts like ILITs, are often used to reduce estate taxes, it’s crucial to understand the nuances. The assets designated irrevocably may still be considered part of the grantor’s estate for certain tax purposes, depending on the structure of the trust and the specific laws governing estate taxation. Expert legal and financial advice is essential to ensure that the desired tax benefits are achieved.

Alteration and Revocation Challenges

Once established, altering or revoking an irrevocable beneficiary designation is exceedingly difficult. It typically requires the explicit written consent of the beneficiary. In rare circumstances, legal challenges might be possible if there is evidence of fraud, undue influence, or a material change in circumstances that was not reasonably foreseeable at the time of the designation. However, these are complex legal battles with uncertain outcomes.

Steps to Designate an Irrevocable Beneficiary

The process of designating an irrevocable beneficiary involves several critical steps, often requiring professional assistance.

1. Consult with Legal and Financial Professionals

The first and most crucial step is to seek advice from experienced estate planning attorneys and financial advisors. They can help assess your goals, explain the implications, and advise on the most appropriate legal structures. For instance, they can guide a drone technology startup founder on how to structure a trust that irrevocably benefits future research initiatives while also complying with relevant corporate and tax laws.

2. Determine the Specific Assets and Beneficiary

Clearly identify the specific financial assets (e.g., life insurance policy, account) that will have an irrevocable beneficiary and precisely name the beneficiary (individual, trust, or charity). Precision is key to avoid ambiguity.

3. Draft Necessary Legal Documents

Depending on the scenario, this may involve drafting trust documents, amending policy beneficiary forms, or creating new legal agreements. The language used in these documents is critical to establishing the irrevocability. For example, specific clauses will be included to explicitly state that the beneficiary designation cannot be changed without the beneficiary’s consent.

4. Execute and Formalize the Designation

Properly execute all legal documents according to state and federal laws. This often involves notarization and witnessing. The financial institution holding the asset must also be formally notified and acknowledge the irrevocable designation.

5. Ongoing Review and Compliance

While the designation is irrevocable, it’s still prudent to periodically review the underlying financial instruments and ensure they remain aligned with your long-term intentions, especially if the financial landscape or beneficiary’s circumstances change significantly. However, any changes to the beneficiary themselves would require their consent and likely new legal documentation.

Conclusion

An irrevocable beneficiary designation represents a profound commitment, a legally binding promise to ensure future financial provision for a chosen individual, entity, or cause. While the direct application might not be in the flight path of a drone, the underlying principles of secure, long-term financial planning are fundamental to the stability and growth of any enterprise, including those at the forefront of drone technology and innovation. Whether it’s securing legacies, fulfilling obligations, or perpetuating charitable missions, understanding and judiciously utilizing the irrevocable beneficiary designation provides a robust framework for guaranteed future support. It is a testament to foresight, a strategic tool for ensuring that intentions endure beyond one’s lifetime, providing a stable foundation for the future, much like the precise engineering that underpins advanced aerial systems.