Navigating the complexities of car financing can feel like a daunting task, especially when trying to determine what constitutes a “good” car payment. This isn’t a simple dollar figure; rather, it’s a metric that reflects your financial health, your budget, and your overall financial goals. A good car payment is one that allows you to afford the vehicle you need or desire without compromising your ability to meet other financial obligations, save for the future, or enjoy your life. It’s about striking a balance between vehicular desire and fiscal responsibility.

Understanding the Factors Influencing Your Car Payment

Before we can even begin to define what a good car payment looks like, it’s crucial to understand the various components that contribute to its calculation. These elements are not static and can fluctuate based on market conditions, your personal financial profile, and the specific vehicle you choose.

The Principal Loan Amount

This is the core of your car payment, representing the actual price of the vehicle minus any down payment you make. A larger down payment directly reduces the principal amount, leading to a lower monthly payment and less interest paid over the life of the loan. Conversely, a small down payment will inflate the principal, resulting in a higher monthly burden.

Interest Rate (APR)

The Annual Percentage Rate (APR) is the cost of borrowing money, expressed as a yearly percentage. This is arguably one of the most significant factors in determining your monthly payment and the total cost of the vehicle. A lower APR means you pay less in interest over time, making your car payment more manageable. Factors influencing your APR include your credit score, the loan term, and prevailing economic conditions. Lenders assess your creditworthiness to gauge the risk they’re taking by lending you money. A higher credit score typically qualifies you for lower APRs.

Loan Term (Duration)

The loan term is the length of time you have to repay the loan, usually measured in months. Common loan terms range from 36 to 84 months. A shorter loan term will result in higher monthly payments because you’re spreading the principal over fewer payments. However, you’ll pay less interest overall. Conversely, a longer loan term will lead to lower monthly payments, which can be more attractive from a cash-flow perspective, but you’ll end up paying significantly more in interest over the life of the loan. This is a critical trade-off to consider.

Loan Fees and Other Charges

Beyond the principal and interest, there may be other fees associated with the car loan. These can include origination fees, documentation fees, and potentially late payment fees. While often a smaller percentage of the total cost, these can still add up and should be factored into your overall financial assessment. Always inquire about all potential fees when discussing loan terms with a lender.

Defining a “Good” Car Payment: Common Benchmarks and Personalization

There’s no single, universally “good” car payment because financial situations and priorities vary so widely. However, several common benchmarks and personalized approaches can help you determine what’s appropriate for your circumstances.

The 20/4/10 Rule

A widely cited guideline in personal finance is the 20/4/10 rule. This rule suggests that you should aim for:

- A 20% down payment: This immediately reduces the amount you need to borrow, lowering your principal and subsequently your monthly payments and total interest. It also signifies a strong financial position to the lender.

- A loan term of no more than 4 years (48 months): Shorter loan terms mean you’ll pay less interest and will own your vehicle outright sooner. This avoids the scenario of being “upside down” on your loan (owing more than the car is worth).

- Your total car expenses (payment, insurance, and fuel) should not exceed 10% of your gross monthly income: This is a crucial metric for ensuring your car doesn’t become a financial albatross. It accounts not just for the payment itself but also for the ongoing costs of ownership.

While the 20/4/10 rule provides a solid framework, it’s important to note that it might be challenging to adhere to strictly in today’s market, where car prices have risen, and longer loan terms are often offered as an incentive for lower monthly payments. However, it remains an excellent aspirational goal.

The Affordability Approach: What You Can Comfortably Pay

Beyond standardized rules, the most practical definition of a good car payment is one that you can comfortably afford within your existing budget. This requires a detailed analysis of your income and expenses.

Budgeting and Expense Tracking

Start by creating a comprehensive budget. Track all your income sources and meticulously list every expense. This includes fixed costs like rent/mortgage, utilities, and existing loan payments, as well as variable costs such as groceries, entertainment, and savings contributions. Once you have a clear picture of where your money goes, identify areas where you can potentially allocate funds towards a car payment without sacrificing essential needs or savings goals.

Emergency Fund Considerations

A good car payment should not come at the expense of maintaining a healthy emergency fund. Unexpected expenses – job loss, medical emergencies, home repairs – can arise at any time. Having 3-6 months of living expenses saved provides a crucial safety net. If affording a car payment means depleting or neglecting your emergency fund, it’s likely too high.

Savings and Investment Goals

Your car payment should not derail your long-term financial goals, such as saving for retirement, a down payment on a home, or your children’s education. If a car payment significantly hinders your ability to contribute to these crucial savings, it’s a sign that the payment is too high. A good car payment allows you to balance current needs with future aspirations.

Debt-to-Income Ratio (DTI)

Lenders often look at your debt-to-income ratio (DTI) when approving loans. Your DTI is the percentage of your gross monthly income that goes towards paying your monthly debt obligations. A lower DTI generally indicates a stronger financial position. While specific thresholds vary by lender, a DTI of 43% or lower is often considered a benchmark for mortgage lending, and a similar principle applies to auto loans. Including a car payment should not push your DTI into unhealthy territory. Aim to keep your DTI as low as possible, considering all your recurring debts.

Beyond the Monthly Payment: Total Cost of Ownership

It’s a common mistake to focus solely on the monthly car payment. A “good” car payment is part of a larger picture that includes the total cost of owning and operating a vehicle.

Insurance Costs

Car insurance premiums can vary significantly based on the vehicle’s make, model, year, your driving history, location, and coverage levels. A sportier or more expensive car will generally cost more to insure than an economical sedan. Before finalizing your car purchase, get insurance quotes for the specific vehicles you are considering. This cost needs to be factored into your overall car budget, and a good car payment will be one that, when combined with insurance, fuel, and maintenance, remains within your affordable range.

Fuel Expenses

The fuel efficiency of a vehicle directly impacts its ongoing operating costs. A gas-guzzling SUV will cost more to fuel than a fuel-efficient hybrid or compact car. Consider your typical driving habits and the current cost of fuel when evaluating the affordability of a vehicle. A good car payment is one that, combined with reasonable fuel expenses, fits within your budget.

Maintenance and Repair Costs

Different vehicles have different maintenance schedules and associated costs. Luxury vehicles or those with specialized parts can be more expensive to maintain and repair than more common models. Research the typical maintenance costs for any vehicle you’re considering. Unexpected repairs can be a significant financial burden, so understanding potential future costs is essential.

Strategies for Securing a Good Car Payment

Achieving a car payment that aligns with your financial goals requires a proactive and informed approach to the car buying and financing process.

Improving Your Credit Score

Your credit score is a primary determinant of the interest rate you’ll be offered. The higher your score, the lower your APR, and consequently, the lower your monthly payment and the total interest paid. Focus on paying bills on time, reducing existing debt, and avoiding opening too many new credit accounts simultaneously.

Shopping Around for Lenders

Don’t settle for the first loan offer you receive, especially from the dealership. Research and compare loan offers from various banks, credit unions, and online lenders. Each institution may have different interest rates and terms based on their lending criteria and your financial profile. Getting pre-approved for a loan before you visit a dealership can give you significant negotiating power.

Negotiating the Vehicle Price

The car payment is directly influenced by the price of the car. Negotiating a lower purchase price for the vehicle will naturally lead to a lower loan amount and, therefore, a lower monthly payment. Be prepared to walk away if you’re not getting a price you’re comfortable with.

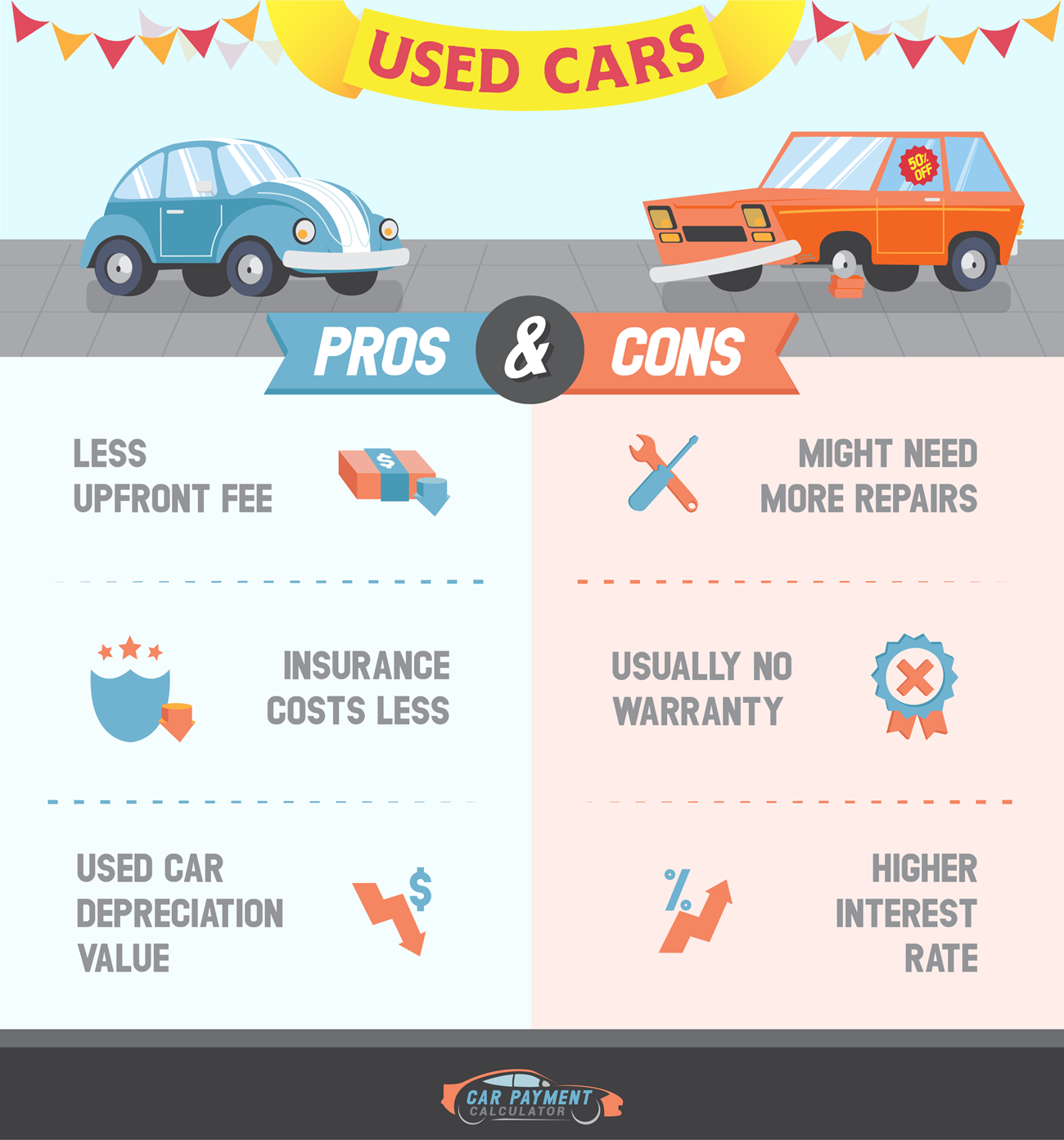

Considering Used Vehicles

New cars depreciate significantly the moment they are driven off the lot. A well-maintained used car can offer substantial savings on the purchase price, leading to a lower loan amount and a more affordable car payment. Thoroughly inspect any used vehicle and consider a pre-purchase inspection by an independent mechanic.

Exploring Alternative Transportation

For some individuals, a car payment might not be the most financially sound option. Depending on your lifestyle, location, and needs, exploring public transportation, carpooling, ride-sharing services, or even bicycles might be more cost-effective solutions that free up your finances for other goals.

In conclusion, a “good” car payment is not a one-size-fits-all figure. It’s a payment that aligns with your personal budget, your financial goals, and your overall financial health. By understanding the factors that influence your payment, utilizing sound financial planning principles, and approaching the car buying process strategically, you can secure a car payment that enhances your life without becoming a financial burden. It’s about making an informed decision that supports your present needs and secures your future financial well-being.