Understanding what constitutes a “good” Annual Percentage Rate (APR) for a personal loan is a crucial step in managing your finances effectively and ensuring you secure the most favorable terms. The APR represents the total cost of borrowing, encompassing not just the interest rate but also any associated fees, expressed as a yearly percentage. For personal loans, a good APR can significantly impact your repayment journey, saving you substantial amounts of money over the life of the loan. The ideal APR is not a universal number; rather, it’s a dynamic figure influenced by a multitude of personal and market-related factors.

The quest for a good APR begins with understanding the components that determine it and recognizing the benchmarks that define favorable lending. This involves a deep dive into your personal financial profile, the prevailing economic climate, and the competitive landscape of lenders. While a low APR is always desirable, the definition of “good” is relative to your individual circumstances and the type of loan you’re seeking.

Understanding the Components of APR

The Annual Percentage Rate (APR) is a comprehensive measure of the cost of borrowing. It’s vital to look beyond the advertised interest rate and understand all the elements that contribute to the APR. Lenders use the APR to provide a standardized way to compare loan offers, ensuring transparency and empowering borrowers to make informed decisions.

The Interest Rate: The Core of the Cost

The interest rate is the most significant component of the APR. It’s the percentage of the principal loan amount that the lender charges you for borrowing the money. Interest rates are typically expressed as a yearly percentage. For personal loans, these rates can vary widely based on the borrower’s creditworthiness, the loan term, and the lender’s risk assessment. A lower interest rate directly translates to a lower overall cost of borrowing, making it a primary factor in what constitutes a “good” APR.

Origination Fees and Other Charges

Beyond the interest rate, several other fees can contribute to the APR. Origination fees are common for personal loans and are charged by the lender to process the loan application. These fees can be a flat amount or a percentage of the loan principal. Other potential charges might include late payment fees, prepayment penalties (though less common for personal loans), or administrative fees. When calculating the APR, these fees are factored in to give a more realistic picture of the true cost of the loan. A loan with a seemingly low interest rate but high origination fees might actually have a higher APR than a loan with a slightly higher interest rate but no fees. Therefore, a thorough understanding of all associated charges is essential when evaluating loan offers.

Loan Term and Its Impact

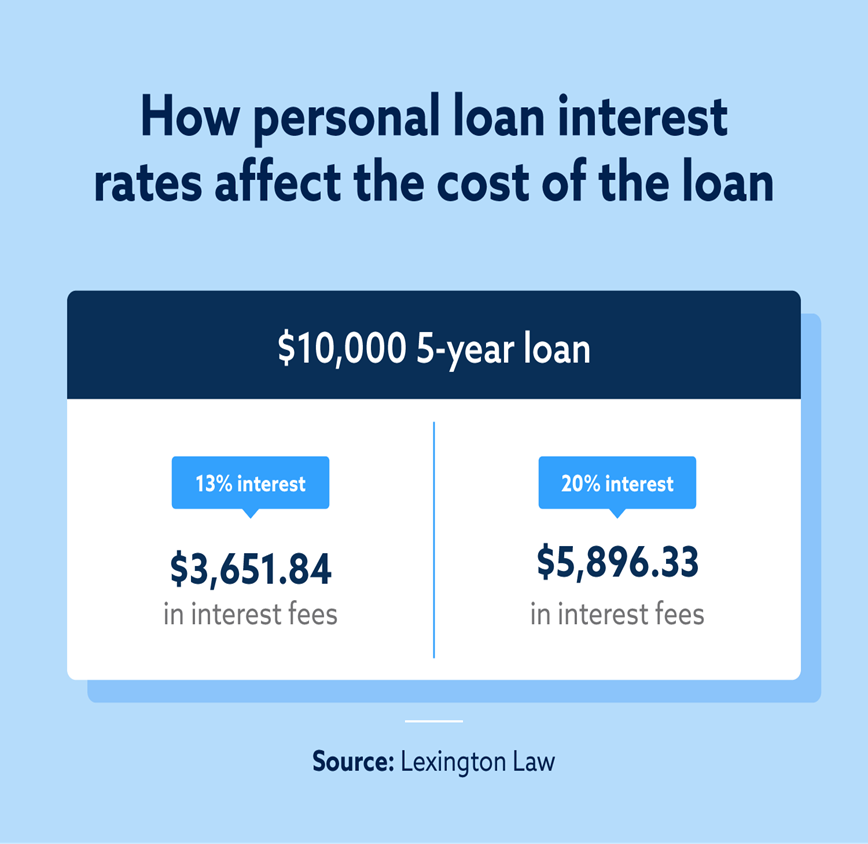

The duration of the loan, or the loan term, also plays a role in the overall cost and, consequently, the APR. While the APR itself is an annualized figure, the length of the repayment period affects the total interest paid. Shorter loan terms generally result in higher monthly payments but less total interest paid over the life of the loan. Conversely, longer loan terms mean lower monthly payments but more accumulated interest. While the APR is intended to standardize comparison, a lower APR on a longer-term loan might still result in more total interest paid than a slightly higher APR on a shorter-term loan. Understanding this interplay is key to discerning what constitutes a “good” APR for your specific financial situation and repayment capacity.

Factors Influencing Your APR

The APR you are offered for a personal loan is not arbitrary. It’s a calculated figure based on a combination of your personal financial attributes and the lender’s assessment of risk. Understanding these influencing factors empowers you to take steps to secure a better APR.

Credit Score: Your Financial Report Card

Your credit score is arguably the most critical factor determining the APR you will be offered. This three-digit number, typically ranging from 300 to 850, represents your creditworthiness – your history of borrowing and repaying debt. Lenders use your credit score to gauge the likelihood that you will repay the loan as agreed. A higher credit score indicates a lower risk to the lender, often resulting in access to lower APRs. Conversely, a lower credit score signals higher risk, leading to higher APRs or even denial of the loan altogether. Maintaining a good credit score through timely payments, responsible credit utilization, and avoiding excessive debt is paramount to securing favorable loan terms.

Credit History: The Narrative of Your Financial Behavior

Beyond just the score, your credit history provides a detailed narrative of your financial behavior. This includes the types of credit you’ve used (credit cards, mortgages, auto loans), how long you’ve had credit, your payment history (on-time payments, late payments, defaults), and your credit utilization ratio. Lenders scrutinize your credit history to identify patterns and potential red flags. A consistent history of responsible credit management, including a mix of credit types and a long, positive payment record, strengthens your application and can help you qualify for a good APR. Conversely, a history of late payments, defaults, or high credit utilization can negatively impact your creditworthiness and lead to higher APR offers.

Income and Employment Stability: Demonstrating Repayment Capacity

Lenders also assess your ability to repay the loan based on your income and employment stability. They will typically require proof of income, such as pay stubs or tax returns, to verify that you have sufficient earnings to cover the loan payments. Furthermore, lenders look for stability in your employment. Frequent job changes or a history of unemployment can be viewed as increased risk, potentially leading to higher APRs. A steady employment history with a stable income demonstrates to lenders that you have the financial capacity to meet your loan obligations consistently, making you a more attractive borrower and increasing your chances of receiving a good APR.

Loan Amount and Term: Balancing Risk and Benefit

The amount of money you wish to borrow and the length of time over which you plan to repay it also influence the APR. Generally, larger loan amounts may carry slightly higher APRs due to the increased risk for the lender. Similarly, longer loan terms can also sometimes be associated with higher APRs, as the lender is exposed to risk for a longer period. However, the relationship isn’t always linear, and lenders also consider how the loan amount and term align with your income and credit profile. Finding the right balance between the loan amount and term that fits your financial needs and repayment capabilities, while also being attractive to lenders, is crucial for securing a good APR.

What Constitutes a “Good” APR? Benchmarks and Context

Defining a “good” APR for a personal loan is not a one-size-fits-all answer. It’s a fluid concept that depends on a variety of factors, including market conditions, your personal financial profile, and the specific type of personal loan. However, by understanding current benchmarks and contextualizing them, you can better assess whether an offered APR is favorable.

General APR Ranges and Market Conditions

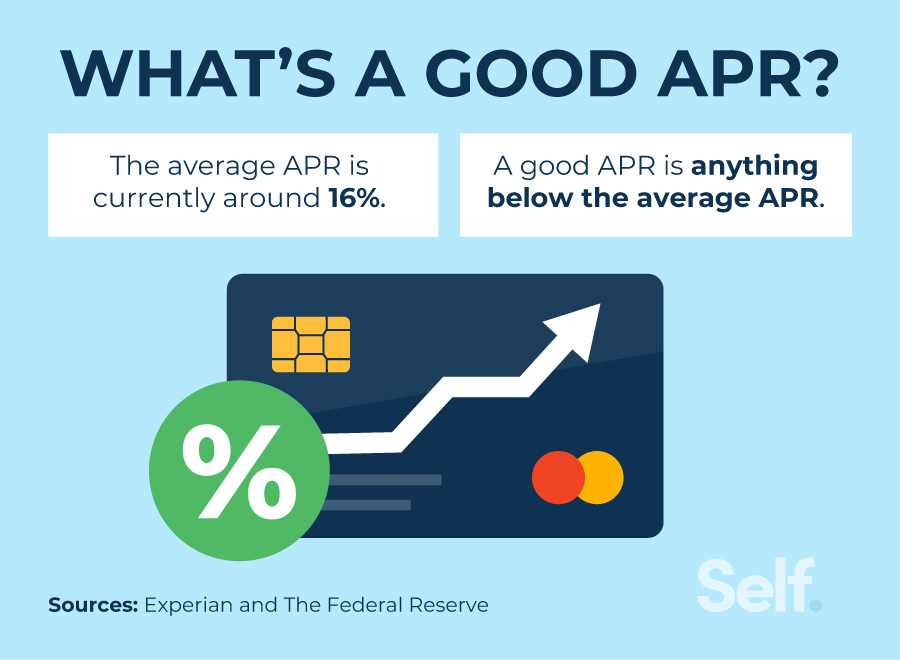

The APRs for personal loans can fluctuate significantly based on prevailing economic conditions, the Federal Reserve’s interest rate policies, and the competitive landscape among lenders. Generally, personal loan APRs can range from as low as 5-6% for borrowers with excellent credit and competitive market offers, to as high as 36% or more for those with poor credit or who are considered high-risk. A “good” APR typically falls within the lower to middle end of this spectrum, reflecting a favorable assessment of your creditworthiness by the lender and a competitive market. Staying informed about current interest rate trends and average APRs for personal loans can provide a valuable benchmark for evaluating offers.

Excellent vs. Good vs. Fair Credit: Tailored APRs

The categorization of your credit score directly correlates with the APR you can expect. Borrowers with excellent credit (typically FICO scores of 740 and above) are in the best position to secure the lowest APRs. For these individuals, a good APR might be in the range of 6-10%, though this can vary. Those with good credit (FICO scores typically between 670 and 739) can still expect competitive rates, perhaps in the 10-15% range. Borrowers with fair credit (FICO scores typically between 580 and 669) will likely face higher APRs, potentially in the 15-25% range, as they represent a greater perceived risk. For individuals with poor credit (FICO scores below 580), APRs can be significantly higher, often exceeding 25% and reaching into the 30s. Understanding where you fall within these credit tiers is essential for setting realistic expectations about what constitutes a good APR for you.

Comparing Loan Offers: The Key to Finding Value

The most effective way to determine if an APR is “good” is through diligent comparison of multiple loan offers. Lenders compete for borrowers, and by shopping around, you increase your chances of finding the most competitive rate. When comparing offers, always look at the full APR, not just the advertised interest rate, and consider all associated fees. Utilize online comparison tools and pre-qualification options, which allow you to check potential rates without impacting your credit score. A “good” APR is not necessarily the lowest rate you can find but the best rate available to you based on your financial profile, that also comes with terms and conditions that align with your repayment strategy.

Strategies for Securing a Better APR

The APR you are offered for a personal loan is not fixed; you can actively take steps to improve your chances of securing a more favorable rate. By focusing on your financial health and employing smart borrowing strategies, you can significantly impact the cost of your loan.

Improving Your Credit Score and History

As previously discussed, your credit score is paramount. Before applying for a personal loan, dedicate time to improving your creditworthiness. This involves consistently making all debt payments on time, reducing your credit utilization ratio (keeping balances low on your credit cards), avoiding opening too many new credit accounts simultaneously, and regularly reviewing your credit reports for any errors that could be negatively impacting your score. Even a modest increase in your credit score can translate into a noticeable reduction in your APR.

Building a Strong Application Beyond Credit

While credit is king, lenders also consider other aspects of your financial profile. A stable employment history with consistent income is a strong indicator of your ability to repay. If possible, demonstrate a history of responsible financial management, such as maintaining a healthy savings account. Some lenders may also consider a co-signer with excellent credit to back your loan, which can help you secure a lower APR. Presenting a well-rounded application that showcases your financial stability and reliability can persuade lenders to offer you better terms, including a more attractive APR.

Shopping Around and Negotiating Terms

Never accept the first loan offer you receive. Actively shop around and compare APRs from multiple lenders, including banks, credit unions, and online lenders. Many lenders offer pre-qualification tools that allow you to check potential rates without a hard inquiry on your credit report. Once you have a few competitive offers, don’t hesitate to negotiate. If you have a better offer from another lender, you can use that as leverage to see if your preferred lender can match or beat it. Remember, the APR is negotiable, and by being an informed and proactive borrower, you can often secure a better deal.