A deferred annuity stands as a cornerstone in personal finance, primarily serving as a vehicle for long-term savings and retirement planning. At its heart, a deferred annuity is a contractual agreement between an individual (the annuitant) and an insurance company. The core promise is simple yet profound: in exchange for a lump sum payment or a series of payments, the insurer commits to providing a stream of income at a future date, typically in retirement. Unlike an immediate annuity, which begins payouts almost immediately, a deferred annuity is designed with an accumulation phase, allowing the initial investment to grow over time, tax-deferred, before the income payments commence.

In an increasingly complex financial landscape, where individuals bear more responsibility for their retirement security, deferred annuities offer a compelling blend of growth potential, tax efficiency, and guaranteed income. Understanding its nuances, particularly how modern technology and innovation are reshaping its utility and accessibility, is crucial for anyone looking to build a robust financial future.

The Core Concept: Securing Future Income

The primary appeal of a deferred annuity lies in its ability to convert a current investment into a future income stream. This characteristic makes it particularly attractive for individuals concerned about outliving their savings, a phenomenon known as longevity risk. The structure of a deferred annuity is ingeniously designed around two distinct periods: the accumulation phase and the annuitization (or payout) phase.

Accumulation vs. Annuitization Phases

During the accumulation phase, the money contributed to the annuity grows on a tax-deferred basis. This means that earnings are not taxed until they are withdrawn, allowing the principal and its returns to compound more effectively over time. The growth rate during this phase can vary significantly depending on the type of deferred annuity selected—whether it’s fixed, variable, or indexed. This phase can last for many years, often until the annuitant reaches a predetermined age or decides to begin receiving income.

The annuitization phase begins when the annuitant elects to convert their accumulated value into a series of regular income payments. These payments can be structured in various ways: for a set period (e.g., 10 or 20 years), for the rest of the annuitant’s life, or even for the joint lives of the annuitant and their spouse. The amount of each payment is determined by factors such as the total accumulated value, the annuitant’s age and gender at the time of annuitization, the chosen payout option, and prevailing interest rates. The transition from accumulation to annuitization is a critical decision point, often influenced by life circumstances and broader financial planning goals.

Key Features and Benefits

Deferred annuities offer several distinctive features that make them a valuable component of a diversified financial strategy. One of the most significant is tax-deferred growth, which allows investments to compound without the drag of annual taxation on earnings. This can lead to substantially larger sums available for retirement compared to taxable accounts.

Another crucial benefit is the potential for guaranteed income for life. This feature, particularly with fixed and certain indexed annuities, provides peace of mind, knowing that a portion of retirement expenses will always be covered, regardless of market downturns or how long one lives. Many annuities also include a death benefit, ensuring that if the annuitant passes away before annuitization, their beneficiaries receive the remaining accumulated value or a guaranteed minimum amount. Furthermore, annuities typically offer various riders and customization options, allowing individuals to tailor the contract to their specific needs, such as inflation protection or enhanced liquidity features, though these often come with additional costs.

Deferred Annuities in the Digital Age: A FinTech Perspective

The traditional image of deferred annuities often conjures paper contracts and face-to-face meetings. However, the advent of financial technology (FinTech) has revolutionized the way these products are accessed, understood, and managed, pushing deferred annuities firmly into the realm of “Tech & Innovation.” Digital platforms, advanced analytics, and artificial intelligence are making these complex instruments more transparent, accessible, and personalized than ever before.

Leveraging Technology for Enhanced Understanding and Accessibility

One of the most significant contributions of FinTech to deferred annuities is improved accessibility and understanding. Online platforms, intuitive calculators, and educational resources powered by digital innovation now demystify the intricacies of annuity products. Prospective annuitants can easily compare different annuity types, project future income streams, and understand the impact of various riders through interactive digital tools. This enhanced transparency empowers individuals to make more informed decisions without necessarily needing a dedicated financial advisor at every step. Furthermore, the application process itself has been streamlined, moving from cumbersome paperwork to digital applications that reduce errors and accelerate approval times. This shift drastically lowers the barrier to entry, making deferred annuities viable options for a broader demographic.

AI and Data Analytics in Personalized Annuity Planning

Artificial intelligence (AI) and sophisticated data analytics are playing an transformative role in personalizing annuity planning. Financial institutions are leveraging AI algorithms to analyze vast datasets, including individual financial profiles, risk tolerance, longevity projections, and market trends. This allows them to offer highly customized annuity solutions that precisely match an individual’s unique retirement goals and risk appetite. AI-driven tools can simulate various market scenarios, helping annuitants visualize the potential outcomes of different annuity choices. Moreover, machine learning models can identify patterns and predict future financial needs, enabling advisors (or robo-advisors) to recommend optimal annuity structures, payout options, and rider selections. This level of personalization, previously unattainable without extensive manual analysis, is a direct result of technological innovation.

Types of Deferred Annuities and Modern Innovations

The landscape of deferred annuities is diverse, with several types catering to different investor profiles and objectives. Each type has seen its own share of innovation, primarily through digital interfaces and enhanced features.

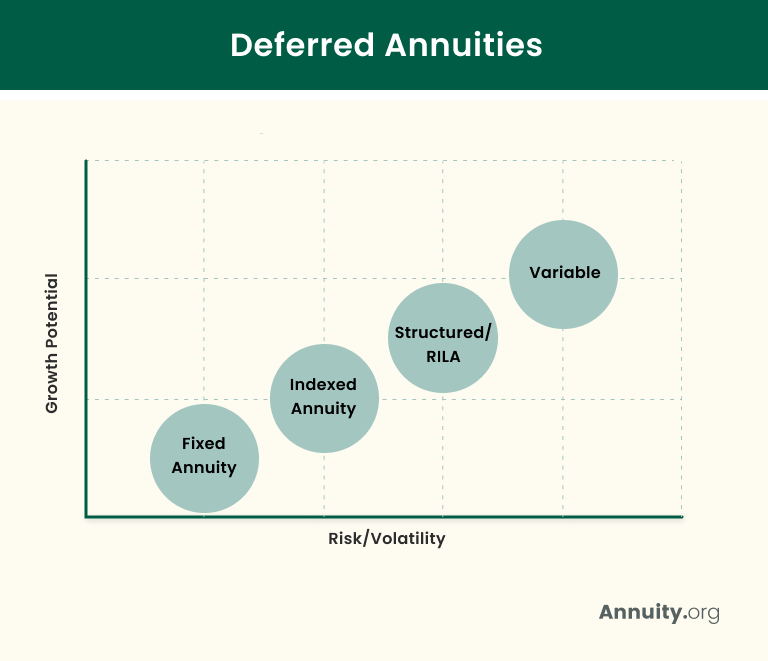

Fixed, Variable, and Indexed Annuities – Evolving with Technology

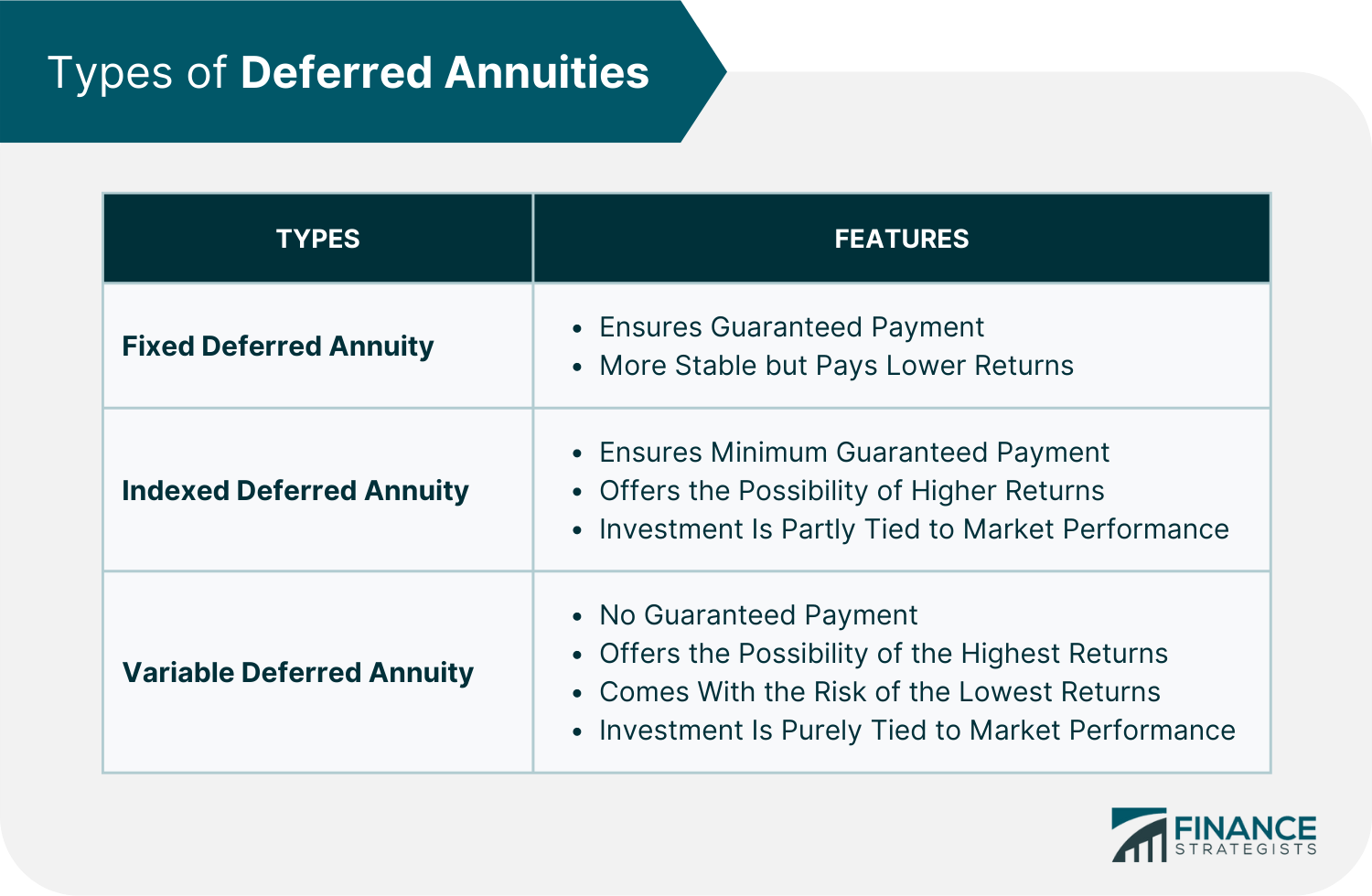

Fixed Deferred Annuities offer a guaranteed interest rate for a specified period, providing predictable growth and capital preservation. Technological innovation here focuses on efficient online quoting systems, digital contract management, and tools that clearly illustrate guaranteed returns.

Variable Deferred Annuities allow annuitants to invest in a selection of sub-accounts, similar to mutual funds, with growth tied to market performance. Innovation in this space includes advanced online dashboards for portfolio tracking, real-time performance reporting, and digital tools that help annuitants rebalance their investments within the annuity, often with AI-powered recommendations.

Indexed Deferred Annuities (FIAs) offer growth potential linked to a market index (like the S&P 500) but with downside protection. FinTech innovation has enabled more transparent explanations of indexing strategies, caps, participation rates, and floors through interactive digital models. Complex crediting methods are made understandable with visual aids and calculators that allow users to simulate potential earnings under different market conditions.

Digital Platforms and Streamlined Management

Modern digital platforms are central to the innovative management of deferred annuities. These platforms provide a single point of access for annuitants to view their account balances, track investment performance (for variable and indexed annuities), access statements, and even initiate certain transactions. Automated alerts can notify annuitants of upcoming contract milestones, changes in market conditions affecting their annuity, or opportunities to optimize their investment. Furthermore, digital tools facilitate seamless communication between annuitants, advisors, and insurance providers, reducing administrative burdens and enhancing the overall customer experience. The ability to manage an annuity from a smartphone or computer empowers annuitants with greater control and convenience, a hallmark of modern tech-driven services.

Strategic Integration: Deferred Annuities in a Comprehensive Financial Plan

The utility of deferred annuities extends beyond mere savings; they are strategic tools for comprehensive financial planning, especially for retirement. Technology has amplified their integration capabilities, making them more dynamic and adaptable within broader financial strategies.

Role in Retirement Planning & Longevity Risk Mitigation

In retirement planning, deferred annuities address the critical challenge of longevity risk – the possibility of outliving one’s savings. By providing a guaranteed income stream for life, they serve as a vital hedge against this risk. Tech innovation has contributed by integrating annuity planning into broader financial planning software. These tools use predictive analytics to model various retirement scenarios, helping individuals understand how adding a deferred annuity impacts their future cash flow, portfolio longevity, and overall financial security. Digital advisors can help allocate appropriate portions of a retirement portfolio to annuities based on an individual’s risk profile and income needs, optimizing for a balanced approach that combines growth assets with guaranteed income.

The Impact of Robo-Advisors and Online Tools

Robo-advisors and other online financial planning tools have significantly democratized access to sophisticated retirement planning strategies, including the appropriate use of deferred annuities. These platforms use algorithms to assess an individual’s financial situation and goals, then recommend tailored investment portfolios that may include annuities. While traditional human advisors remain crucial, robo-advisors offer a cost-effective and accessible entry point for many, providing data-driven recommendations on when and how to incorporate deferred annuities. This innovative approach makes expert-level financial guidance more widely available, ensuring that the benefits of annuities can be leveraged by a broader segment of the population.

Navigating Complexity with Technological Clarity

Deferred annuities can be complex financial instruments due to their contractual nature, various features, and regulatory considerations. Technology and innovation are pivotal in simplifying this complexity, offering greater clarity and ensuring compliance.

Regulatory Compliance and Transparency through Tech

The financial industry is heavily regulated, and annuities are no exception. Technology plays a critical role in ensuring regulatory compliance and enhancing transparency. Digital platforms can automate compliance checks, maintain meticulous records, and generate audit trails, reducing the risk of errors and non-compliance. Smart contracts and blockchain technology, though still nascent in this specific application, hold future potential for creating immutable, transparent, and self-executing annuity agreements, further enhancing trust and reducing disputes. Furthermore, technology facilitates the clear disclosure of terms, fees, and risks associated with deferred annuities, empowering consumers with all the necessary information to make informed decisions.

Future Outlook: Continuous Innovation in Annuity Products

The trajectory for deferred annuities is one of continuous innovation, driven by technological advancements and evolving consumer needs. We can anticipate further development in AI-driven personalized product recommendations, real-time performance monitoring, and predictive analytics that anticipate changes in an annuitant’s financial situation. Blockchain may eventually offer enhanced security, transparency, and efficiency in annuity contracts and payments. Moreover, the integration of annuities with other FinTech solutions, such as budgeting apps and wealth management platforms, will create a more holistic and seamless financial experience. As individuals live longer and demand greater control and flexibility over their retirement savings, deferred annuities, propelled by “Tech & Innovation,” are set to become even more sophisticated, adaptable, and indispensable tools for securing financial longevity.