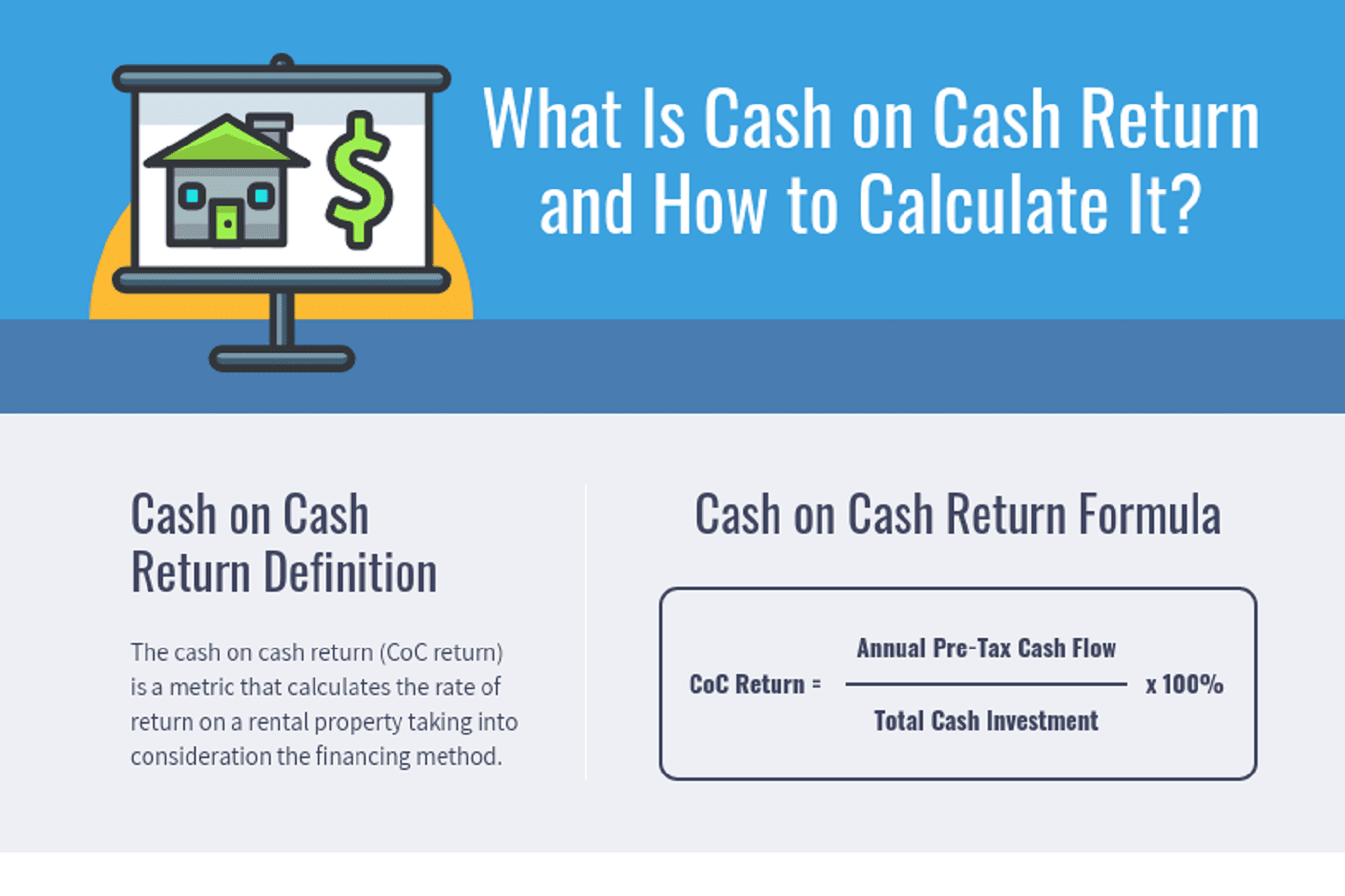

In the realm of real estate investment, understanding profitability is paramount. Beyond the headline purchase price and the eventual sale value, discerning investors delve into metrics that reveal the true income-generating power of their assets. Among these crucial indicators, the cash-on-cash return stands out as a direct and vital measure of an investment’s immediate profitability, particularly for those focused on generating passive income. This metric offers a clear snapshot of the annual pre-tax cash flow an investor can expect relative to the actual cash invested. It’s a fundamental concept for anyone looking to assess the effectiveness of their real estate ventures and compare the performance of different investment opportunities.

Understanding the Core Components of Cash-on-Cash Return

At its heart, the cash-on-cash return is a ratio that answers a simple yet powerful question: “How much cash am I getting back each year for every dollar of cash I’ve put into this property?” To accurately calculate this, we need to dissect two primary components: the annual pre-tax cash flow and the total cash invested. Both require careful consideration and accurate accounting to provide a meaningful result.

Annual Pre-Tax Cash Flow: The Engine of Profitability

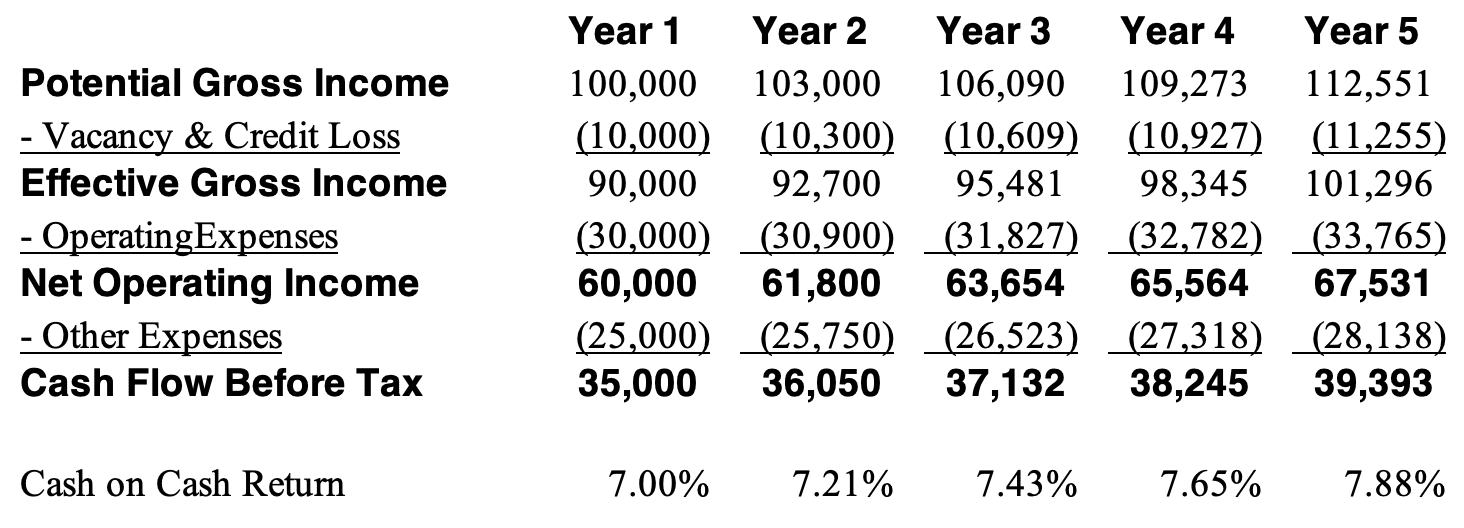

The annual pre-tax cash flow represents the net income generated by a property over a year, before accounting for income taxes. This is the actual money that flows into the investor’s pocket after all operating expenses and debt service have been paid. It’s crucial to distinguish this from net operating income (NOI), which excludes debt service. Cash-on-cash return must include the impact of financing because a significant portion of the investor’s actual out-of-pocket expense is the mortgage payment.

To calculate annual pre-tax cash flow, we start with the gross rental income. This is the total potential rent collected from all units in the property over a year, assuming 100% occupancy. However, in reality, vacancies are a factor, so it’s more practical to use the effective gross income (EGI). EGI accounts for potential rental losses due to vacancies and concessions.

From the EGI, we then subtract all operating expenses. These are the costs associated with running and maintaining the property. Common operating expenses include:

- Property Taxes: Annual taxes levied by the local government.

- Insurance: Premiums for landlord insurance policies.

- Property Management Fees: If a third-party management company is hired.

- Repairs and Maintenance: Costs for routine upkeep and minor repairs.

- Utilities: If any utilities are paid by the landlord.

- HOA Fees: If the property is part of a homeowner’s association.

- Property Management Salaries: If managing in-house.

- Legal and Accounting Fees: Costs for professional services related to the property.

It’s important to be realistic with these estimates. Overestimating income or underestimating expenses will lead to an inflated and inaccurate cash-on-cash return.

Once operating expenses are subtracted from the EGI, we arrive at the Net Operating Income (NOI). However, for cash-on-cash return, we need to go a step further and account for the debt service. This is the total amount paid annually on any loans secured by the property, including principal and interest payments.

- Annual Debt Service = (Monthly Mortgage Payment) x 12

The final step in determining annual pre-tax cash flow is to subtract the annual debt service from the NOI:

- Annual Pre-Tax Cash Flow = NOI – Annual Debt Service

This figure represents the actual cash profit the investor pockets from the property each year before any income taxes are considered.

Total Cash Invested: The Out-of-Pocket Expense

The denominator in the cash-on-cash return calculation is the total amount of actual cash the investor has personally contributed to the acquisition and immediate stabilization of the property. This is not the total purchase price, nor is it the loan amount. It represents the sum of all out-of-pocket expenses necessary to acquire and get the property ready for rent.

Key components of total cash invested include:

- Down Payment: The initial percentage of the purchase price paid in cash by the investor.

- Closing Costs: These are fees paid at the closing of a real estate transaction. They can include:

- Loan origination fees

- Appraisal fees

- Title insurance premiums

- Recording fees

- Attorney fees

- Inspection fees

- Escrow fees

- Initial Repairs and Renovations: Any immediate capital expenditures made to the property to make it rentable or to increase its value. This is distinct from ongoing repairs and maintenance, which are operating expenses. If significant renovations are needed to make the property habitable or attractive to tenants, these costs should be included as part of the initial investment.

- Reserves: Sometimes, investors will place additional cash reserves with the lender or set aside funds for immediate capital expenditures. These cash reserves, if directly tied to the acquisition and initial stabilization, can be considered part of the total cash invested.

It is crucial to be precise here. For instance, if a property is purchased for $200,000 with a 20% down payment ($40,000), and closing costs amount to $5,000, and initial renovations cost $10,000, the total cash invested would be $40,000 + $5,000 + $10,000 = $55,000. The remaining $160,000 would be the loan amount, which does not count as cash invested.

Calculating and Interpreting the Cash-on-Cash Return

With a clear understanding of the two core components, the calculation of cash-on-cash return becomes straightforward. However, interpreting the resulting percentage requires context and an understanding of its limitations.

The Formula and Its Application

The formula for cash-on-cash return is elegantly simple:

- Cash-on-Cash Return = (Annual Pre-Tax Cash Flow / Total Cash Invested) x 100%

Let’s revisit our example. If the property generates an annual pre-tax cash flow of $6,000 and the total cash invested was $55,000, the calculation would be:

- Cash-on-Cash Return = ($6,000 / $55,000) x 100% ≈ 10.91%

This means that for every dollar of cash invested, the investor is receiving approximately 10.91 cents back in pre-tax profit annually. This percentage provides a standardized way to evaluate the performance of this specific investment.

What a “Good” Cash-on-Cash Return Looks Like

Defining what constitutes a “good” cash-on-cash return is subjective and highly dependent on several factors, including market conditions, investment strategy, risk tolerance, and the investor’s goals. However, some general benchmarks can be applied:

- Below 5%: Often considered low, especially in markets with high property values or low rental yields. This might indicate an underperforming investment or a property purchased at a premium.

- 5% to 10%: A respectable range for many residential real estate investments, particularly in stable markets. It suggests a reasonable return on invested capital.

- 10% to 15%: Generally considered a strong cash-on-cash return, indicating a potentially excellent investment with good cash flow relative to the initial cash outlay.

- Above 15%: Typically signifies a very strong performer, possibly in a high-yield market, or achieved through significant value-add strategies or a lower initial cash investment.

It’s crucial to compare the cash-on-cash return of a potential investment against:

- Other Investment Opportunities: How does it stack up against other real estate deals or even other asset classes like stocks or bonds?

- Local Market Averages: What are similar properties in the same area yielding?

- Your Personal Financial Goals: Does this return help you achieve your desired passive income level or wealth-building targets?

Furthermore, a higher cash-on-cash return is not always the sole determinant of a superior investment. For example, a property with a lower cash-on-cash return but significant potential for appreciation might be more attractive to certain investors.

The Importance and Limitations of Cash-on-Cash Return

The cash-on-cash return is a powerful tool in an investor’s arsenal, offering a direct measure of income generation. However, like any single metric, it has its limitations and should be considered alongside other financial analyses.

Why Cash-on-Cash Return Matters to Investors

- Simplicity and Clarity: It’s easy to understand and calculate, making it accessible to both novice and experienced investors.

- Focus on Actual Returns: It directly measures the cash that an investor receives, which is often the primary goal of real estate investing, especially for those seeking passive income.

- Comparison Tool: It allows investors to compare the immediate profitability of different investment properties, regardless of their purchase price or financing structure. A $10,000 cash-on-cash return on a $100,000 investment (10%) is generally more attractive than a $10,000 cash-on-cash return on a $200,000 investment (5%), assuming all other factors are equal.

- Performance Evaluation: It helps investors track the ongoing performance of their existing portfolio and identify properties that may need attention.

Limitations to Consider

- Ignores Appreciation: The most significant limitation is that cash-on-cash return does not account for potential property value appreciation. An investment with a modest cash-on-cash return might be an excellent long-term performer if the property’s value significantly increases over time.

- Excludes Tax Benefits: It is a pre-tax metric. Investors may realize substantial tax advantages from real estate ownership, such as depreciation deductions, which can significantly reduce their overall tax liability and improve their after-tax cash flow.

- Doesn’t Account for Loan Amortization: While debt service is included, the portion of the mortgage payment that goes towards principal reduction builds equity over time, which is a form of return on investment not captured by cash-on-cash.

- Short-Term Focus: It primarily reflects the current year’s performance and may not fully capture the long-term potential or risk profile of an investment.

- Susceptible to Manipulation: If not calculated diligently with realistic expense projections, it can be misleading. Overly optimistic assumptions about rental income or underestimated expenses can inflate the metric.

Beyond Cash-on-Cash: Complementary Metrics for Holistic Analysis

While the cash-on-cash return is invaluable, a truly comprehensive investment analysis requires looking at other financial metrics that provide a more complete picture of an investment’s performance and potential. These metrics help to address the limitations of cash-on-cash return and offer insights into different aspects of profitability and value creation.

Internal Rate of Return (IRR): The Long-Term Perspective

The Internal Rate of Return (IRR) is a more sophisticated metric that calculates the discount rate at which the net present value (NPV) of all cash flows from a particular investment equals zero. In simpler terms, it represents the annualized effective compounded rate of return that an investment is expected to yield.

-

Key Advantages of IRR:

- Considers Time Value of Money: It accounts for the fact that a dollar today is worth more than a dollar in the future.

- Includes All Cash Flows: It incorporates all anticipated cash inflows and outflows over the entire holding period, including the eventual sale of the property.

- Accounts for Appreciation and Equity Buildup: Unlike cash-on-cash, IRR implicitly includes the impact of property appreciation and the principal portion of mortgage payments that builds equity.

-

How it Differs from Cash-on-Cash: While cash-on-cash looks at the annual return on invested cash, IRR provides a projected overall return on the investment over its entire lifespan. A property might have a moderate cash-on-cash return but a high IRR if it’s expected to appreciate significantly.

Capitalization Rate (Cap Rate): The Unleveraged Performance Indicator

The Capitalization Rate (Cap Rate) is another fundamental metric used in real estate. It represents the ratio of a property’s Net Operating Income (NOI) to its market value (or purchase price).

-

Cap Rate = (Net Operating Income / Property Value) x 100%

-

Key Advantages of Cap Rate:

- Unleveraged Comparison: It provides a measure of a property’s return potential without considering the impact of financing. This allows for a direct comparison of the operational profitability of different properties, regardless of how they are financed.

- Market Indicator: Cap rates are widely used by investors and appraisers to assess the relative value of income-producing properties. Lower cap rates generally indicate higher property values relative to their income, and vice versa.

-

How it Differs from Cash-on-Cash: Cap rate is a measure of unleveraged yield, while cash-on-cash return is a measure of leveraged, after-operating-expenses, before-tax yield. A property with a high cap rate may not necessarily translate into a high cash-on-cash return if it carries a significant amount of debt. Conversely, a property with a lower cap rate might offer a strong cash-on-cash return due to strategic financing.

Return on Investment (ROI): The Broader Profitability Measure

While often used interchangeably with cash-on-cash return, Return on Investment (ROI) is a more general profitability metric. It measures the profit generated relative to the total cost of the investment.

-

ROI = (Net Profit / Cost of Investment) x 100%

-

How it Differs from Cash-on-Cash: When applied to real estate, ROI can be calculated in various ways. If “Net Profit” is defined as the total profit from sale (including appreciation and equity buildup) minus total expenses, and “Cost of Investment” is the total cash invested, it encompasses a broader view than just annual cash flow. However, for ongoing income analysis, cash-on-cash is more specific to the cash-generating aspect.

By analyzing these complementary metrics alongside cash-on-cash return, investors can gain a robust understanding of their real estate investments, making more informed decisions that align with their financial objectives and risk appetites. Each metric offers a unique lens through which to view profitability, and using them in conjunction provides a more accurate and complete financial picture.