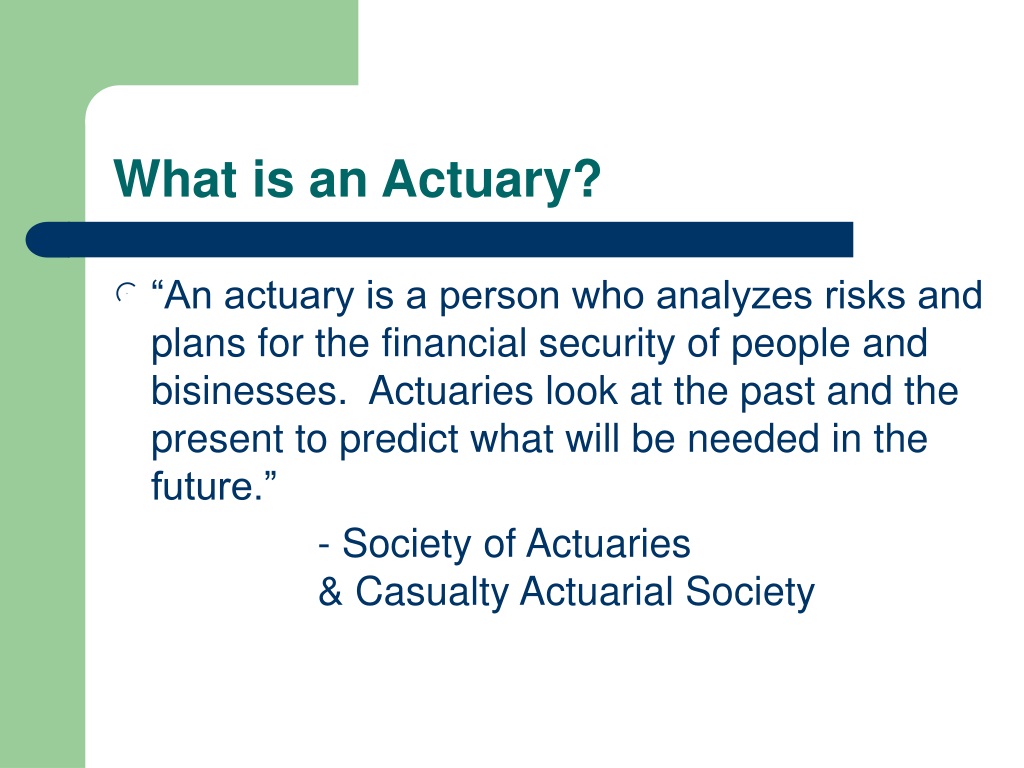

In an era defined by relentless technological advancement and escalating complexity, the role of an actuary has evolved far beyond traditional number-crunching. An actuary, at its core, is a professional who applies advanced mathematical, statistical, and financial theories to assess and manage risk, primarily in the insurance and finance industries. However, to truly understand “what is an actuarial” today, one must recognize their pivotal position at the intersection of quantitative analysis, strategic business foresight, and cutting-edge technological innovation. They are not merely forecasters of financial futures; they are architects of robust, future-proof systems, leveraging big data, artificial intelligence, and sophisticated modeling techniques to navigate an increasingly uncertain world. This field embodies a critical form of “Tech & Innovation,” applying advanced computational power and analytical methods to derive insights from vast datasets and inform critical decisions.

The Actuarial Imperative: Navigating Uncertainty with Data Science

The primary mission of an actuary is to translate uncertainty into quantifiable risk, thereby enabling businesses and individuals to make informed decisions. This imperative has never been more relevant than now, with unprecedented access to data and the computational power to process it. Actuarial science, therefore, stands as a sophisticated application of data science to some of the most complex financial problems.

Foundations in Predictive Analytics

At the heart of actuarial work lies predictive analytics. Actuaries develop and deploy complex statistical models to forecast future events such such as mortality rates, disease prevalence, investment returns, and the likelihood of catastrophic events. Historically, this involved meticulous statistical analysis and manual calculations. Today, however, the field is supercharged by modern data science techniques. Actuaries utilize advanced methodologies like generalized linear models, time-series forecasting, and intricate stochastic modeling to simulate millions of possible outcomes. This allows them to project long-term liabilities, assess the solvency of pension funds, price insurance products accurately, and understand the potential impact of various market conditions or behavioral shifts. The emphasis has shifted from simply calculating probabilities to understanding the distribution of possible outcomes, giving a much richer understanding of risk.

Bridging Mathematics and Business Strategy

While deeply rooted in mathematics and statistics, the actuary’s value extends significantly into strategic business counsel. They are not just producers of complex algorithms and detailed reports; they are interpreters. Actuaries translate highly technical analytical findings into clear, actionable business insights for senior management, stakeholders, and regulators. Their work directly influences critical strategic decisions such as product design, pricing strategy, capital allocation, reserve setting, and overall enterprise risk management. For instance, an actuary might analyze vast demographic and health data to design a new health insurance product, projecting its profitability and potential market penetration, all while ensuring compliance with evolving regulations. This strategic interpretation of data makes them indispensable partners in business innovation and sustainability.

Technological Evolution of Actuarial Practice: Embracing AI and Big Data

The actuarial profession has undergone a profound technological transformation, moving from reliance on rudimentary tools to leveraging the full power of modern computational analytics. This evolution mirrors the broader “Tech & Innovation” landscape, with actuaries at the forefront of applying advanced computing to complex financial domains.

AI, Machine Learning, and Big Data in Actuarial Science

The advent of Artificial Intelligence (AI) and Machine Learning (ML) has revolutionized actuarial science. Actuaries now integrate sophisticated AI/ML algorithms – including neural networks, decision trees, random forests, and gradient boosting machines – into their models for enhanced accuracy and deeper insights. These technologies are particularly powerful in processing vast datasets, identifying subtle patterns, and predicting outcomes with a level of precision previously unattainable. Applications include highly accurate risk segmentation, personalized pricing based on individual behavior (e.g., using telematics data for auto insurance or wearable device data for health insurance), and advanced fraud detection systems that can identify anomalies in claims data in real-time. The ability to ingest and analyze “big data” from diverse sources – ranging from traditional policyholder information to external economic indicators, IoT sensor data, and even anonymized social media trends – allows actuaries to build dynamic models that adapt and learn, offering a granular view of risk that was once unimaginable.

From Spreadsheets to Sophisticated Simulation Models

The journey of actuarial tools has evolved dramatically from foundational spreadsheets to highly sophisticated computational platforms. Today’s actuaries utilize specialized actuarial software suites, powerful statistical programming languages like Python and R, and cloud-based computing resources to manage and analyze massive datasets. Techniques such as Monte Carlo simulations allow actuaries to model thousands or even millions of possible future scenarios, providing a comprehensive distribution of potential financial outcomes rather than a single point estimate. This probabilistic modeling approach is crucial for assessing tail risks, conducting stress tests, and performing dynamic financial analysis, which explores how a company’s financial position might change under various hypothetical future economic conditions. This shift represents a significant leap in analytical capability, enabling more robust risk management and strategic planning.

Actuaries as Architects of Future-Proof Systems: Anticipating Emerging Risks

Beyond conventional financial risks, actuaries are increasingly critical in understanding, quantifying, and mitigating novel and complex risks that emerge from a rapidly changing global landscape. Their innovative approach to risk assessment is essential for future-proofing businesses.

Designing Robust Risk Frameworks

Actuaries play a central role in designing and implementing comprehensive enterprise risk management (ERM) frameworks. These frameworks extend beyond purely financial risks to encompass operational, strategic, reputational, and compliance risks. By integrating these diverse risk categories into a holistic view, actuaries help organizations develop strategies to identify, measure, monitor, and control potential threats across the entire enterprise. This systematic approach ensures that companies can build resilience, adapt to unforeseen challenges, and protect their long-term viability in an increasingly volatile world. They help organizations move from reactive risk management to proactive strategic risk management.

The Role in Emerging Technologies and Cyber Risks

The proliferation of new technologies brings with it a new class of risks that actuaries are uniquely positioned to analyze. They are at the forefront of quantifying the financial implications of cyberattacks, data breaches, and systemic technology failures. For instance, actuaries are developing models to assess the frequency and severity of cyber incidents, informing the pricing of cyber insurance products and guiding companies on appropriate risk mitigation investments. Similarly, as autonomous vehicles, smart contracts, and other cutting-edge technologies become mainstream, actuaries are developing frameworks to understand and manage their associated liabilities and opportunities. Their analytical rigor provides the foundation for developing innovative insurance products and risk strategies that address these novel and rapidly evolving threats, embodying true “Tech & Innovation” in risk foresight.

Driving Innovation in Financial Products and Services: Personalization and Predictive Power

Actuaries are not merely responding to risk; they are actively shaping the future of financial products and services, making them more personalized, efficient, and responsive through data-driven innovation.

Personalization and Dynamic Pricing

Leveraging advanced data analytics and sophisticated actuarial models, actuaries are enabling unprecedented levels of personalization in financial products. In insurance, this means moving beyond broad demographic categories to assess individual risk profiles with remarkable precision. Telematics devices in cars provide real-time driving data, allowing for usage-based insurance premiums that reflect actual driving behavior. Wearable health devices can inform health insurance policies, encouraging healthier lifestyles while dynamically adjusting premiums. This highly granular risk assessment facilitates dynamic pricing strategies that are fairer, more competitive, and more reflective of individual needs and behaviors, driven entirely by innovative data collection and analysis.

Impact on Insurance, Pensions, and Investment Strategies

The innovative work of actuaries leads directly to the creation of new and tailored financial products. Examples include parametric insurance, which pays out automatically based on predefined triggers (e.g., specific weather events) rather than damage assessment, enabled by real-time data feeds. Actuarial models are also critical in the design and management of complex pension schemes, ensuring their long-term solvency and sustainability. Furthermore, actuaries contribute significantly to investment strategies, providing crucial insights into asset-liability matching, capital market risk, and portfolio optimization, all underpinned by rigorous quantitative modeling and forecasting. Their ability to project future cash flows and liabilities allows for more informed and innovative investment decisions.

The Actuarial Mindset: A Blend of Quantitative Rigor and Strategic Foresight

Success as an actuary in this rapidly evolving, tech-driven landscape demands a unique blend of analytical prowess, acute business acumen, and an unwavering commitment to ethical practice.

Ethical Considerations in AI-Driven Risk Assessment

As actuaries increasingly rely on AI and machine learning, ethical considerations become paramount. The potential for algorithmic bias, data privacy concerns, and issues of transparency and explainability in automated decision-making processes are significant challenges. Actuaries bear a critical responsibility to ensure that the models they build and deploy are fair, unbiased, and compliant with regulatory standards. This involves rigorous testing for disparate impact, advocating for data governance best practices, and maintaining human oversight over complex algorithms. Their ethical compass guides the responsible application of powerful technologies in sensitive financial contexts.

Continuous Learning and Adaptation in a Digital Age

The actuarial profession requires a commitment to lifelong learning. To remain at the forefront of “Tech & Innovation,” actuaries must continuously upskill in emerging technologies, programming languages (such as Python and R), advanced statistical software, and data visualization tools. They must also remain abreast of new data sources, evolving regulatory landscapes, and the shifting dynamics of global markets. This constant adaptation ensures that actuaries can effectively leverage the latest technological advancements to address new challenges and seize emerging opportunities, cementing their role as indispensable navigators of financial risk in a digital age.

In conclusion, “what is an actuarial” transcends a simple definition of a risk assessor. Today’s actuary is a technologist, a data scientist, a strategist, and an ethical guardian, leveraging the power of advanced analytics, AI, and sophisticated modeling to manage complex financial risks. They are critical innovators in the financial sector, ensuring the stability and resilience of businesses, shaping the future of financial products, and guiding strategic decisions in an ever-changing world. Their unique blend of quantitative rigor and strategic foresight, underpinned by a relentless embrace of technological advancement, positions them as vital architects of our collective financial future.