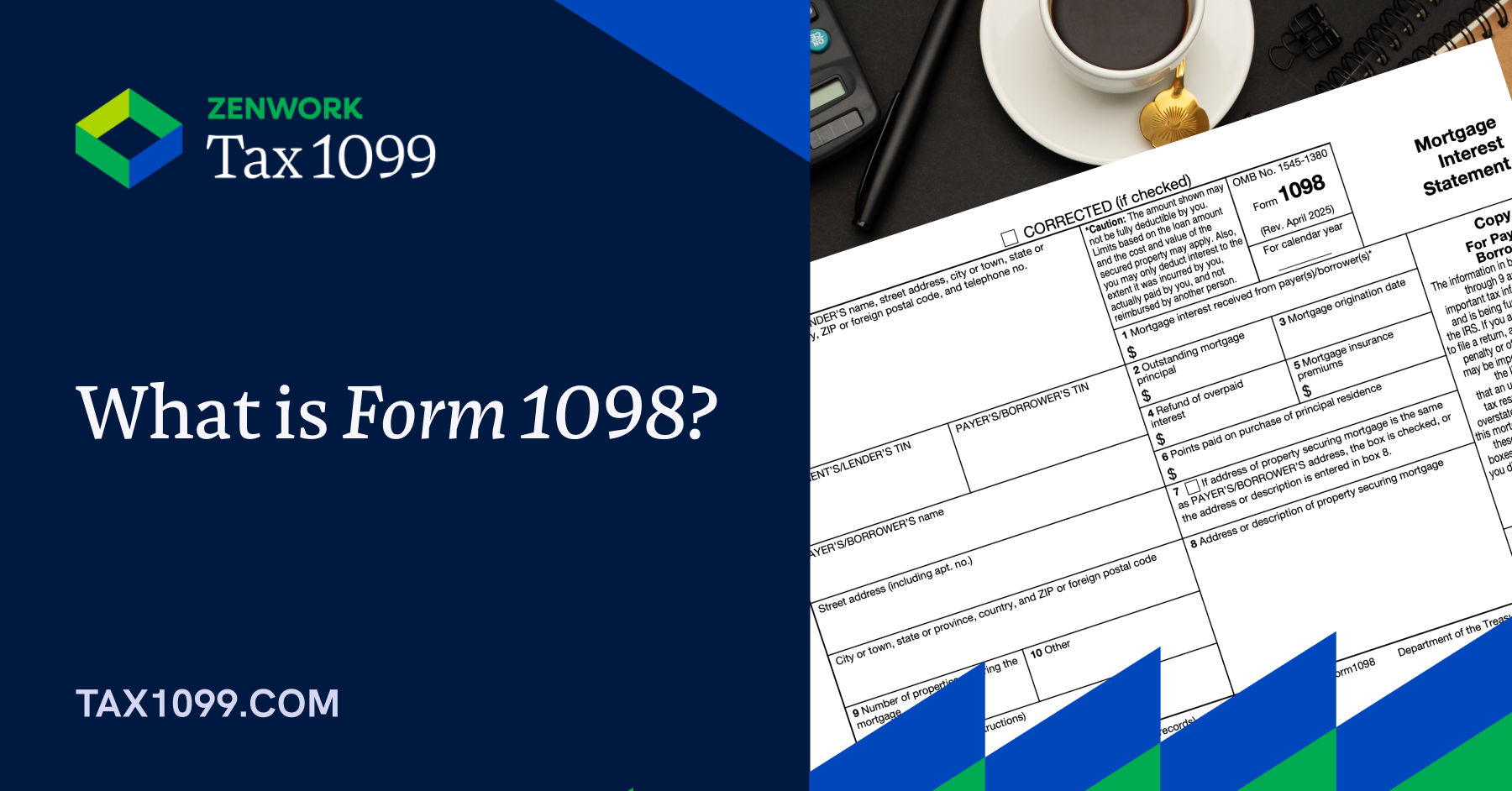

The 1098 tax form, officially known as the Mortgage Interest Statement, is a crucial document for homeowners who have paid mortgage interest during the tax year. It serves as an informational return filed by mortgage lenders and servicers with the Internal Revenue Service (IRS) and provided to borrowers. Understanding the purpose and contents of a Form 1098 is essential for accurate tax preparation and for potentially claiming valuable deductions. This form simplifies the process of reporting mortgage interest, allowing taxpayers to benefit from deductions that can significantly reduce their taxable income.

Understanding the Purpose of Form 1098

The primary function of Form 1098 is to inform both the IRS and the taxpayer of the total mortgage interest paid during a calendar year. Lenders are legally obligated to furnish this information to the IRS to ensure compliance with tax laws and to prevent potential underreporting of income or overclaiming of deductions. For homeowners, this form acts as a readily available record of their deductible mortgage interest payments, eliminating the need to meticulously comb through monthly statements to calculate this figure.

Who Receives a Form 1098?

Generally, any individual or entity that has paid at least $600 in mortgage interest to a financial institution during the tax year will receive a Form 1098. This includes interest paid on:

- Primary Residence Mortgages: The most common scenario involves interest paid on the mortgage for your main home.

- Second Home Mortgages: If you have a mortgage on a vacation home or another property you own, the interest paid on that loan may also be reported.

- Home Equity Loans and Lines of Credit (HELOCs): Interest paid on these types of loans is deductible, provided the funds were used to buy, build, or substantially improve your home.

- Mortgages on Investment Properties: While less common and with different deduction rules, interest on mortgages for investment properties might also be reported.

It’s important to note that while lenders are required to send the form if the $600 threshold is met, you may still be able to deduct mortgage interest even if you don’t receive a Form 1098, provided you meet the IRS criteria for deductibility and have the necessary documentation.

Key Information Provided on Form 1098

Form 1098 is structured to provide clear and concise information relevant to mortgage interest deductions. The most critical boxes include:

- Box 1: Mortgage Interest Received from Payer: This box displays the total amount of mortgage interest paid by the taxpayer to the lender during the tax year. This is the primary figure used for the mortgage interest deduction.

- Box 2: Outstanding Mortgage Principal: This shows the remaining balance of the mortgage loan as of the end of the tax year. While not directly used for interest deduction, it can be helpful for financial planning and understanding your loan status.

- Box 3: Mortgage Origination Date: The date the mortgage was originated is provided, which can be relevant for certain tax calculations.

- Box 4: Refund of Overpaid Interest: If any interest was refunded to the taxpayer during the year, it will be reported here. This amount is generally subtracted from the deductible interest.

- Box 5: Mortgage Insurance Premiums: This box reports any mortgage insurance premiums paid. While these were deductible in prior years, their deductibility has changed, and it’s crucial to check current IRS guidelines.

- Box 6: Points Paid on Purchase of Principal Residence: Points are fees paid to the lender at the time of closing to get a lower interest rate. These may be deductible in the year they are paid, subject to certain conditions.

- Box 7: Address of Property: The address of the property securing the mortgage is listed, confirming the relevant property.

- Box 8: Property Identification Number: A unique identifier for the property.

- Box 9: Cost of a Mobile Home: If the mortgage was for a mobile home, this box may be used.

- Box 10: Other Information: This section can contain additional details relevant to the mortgage, such as information about property taxes that might have been paid through an escrow account.

Claiming the Mortgage Interest Deduction with Form 1098

The mortgage interest deduction is one of the most significant tax benefits available to homeowners. It allows individuals to reduce their taxable income by the amount of qualified mortgage interest they have paid. Form 1098 significantly simplifies the process of claiming this deduction on your federal income tax return.

When is Mortgage Interest Deductible?

To claim the mortgage interest deduction, the mortgage must be secured by your main home or a second home. Additionally, the loan must meet specific criteria:

- Acquisition Debt: The loan must have been used to buy, build, or substantially improve your qualified residence. The total acquisition debt (including any home equity debt used for these purposes) cannot exceed $750,000 for mortgages entered into on or after December 16, 2017, and $1 million for mortgages entered into before that date.

- Home Equity Debt: If you use a home equity loan or HELOC, the deduction is limited to the extent the loan proceeds were used to buy, build, or substantially improve your qualified residence. The total home equity debt plus any acquisition debt cannot exceed the fair market value of your home.

How to Report Mortgage Interest on Your Tax Return

When you file your federal income tax return (typically Form 1040), you will report your mortgage interest deduction on Schedule A, Itemized Deductions.

- Gather Your Form 1098: Locate the Form 1098 provided by your mortgage lender.

- Identify Box 1: The amount in Box 1 is the primary figure for your mortgage interest deduction.

- Determine if Itemizing is Beneficial: You can only deduct mortgage interest if you choose to itemize your deductions. You will itemize if the total of your itemized deductions (including mortgage interest, state and local taxes, charitable contributions, etc.) is greater than the standard deduction.

- Enter the Information on Schedule A: On Schedule A, find the section for “Home Mortgage Interest.” You will enter the lender’s name and address and the amount of mortgage interest paid (from Box 1 of Form 1098).

- Include Other Deductible Expenses: If you paid points (reported in Box 6), they may also be deductible. Consult IRS Publication 936, Home Mortgage Interest, for specific rules on deducting points. If you paid mortgage insurance premiums (reported in Box 5), their deductibility has been subject to change; refer to current tax laws.

- Carryover Calculations: In some cases, you may have paid more mortgage interest than you can deduct in a given year. The IRS allows you to carry over and deduct this excess interest in future years, provided the mortgage continues to qualify.

What if You Don’t Receive a Form 1098?

There are situations where you might not receive a Form 1098, even if you paid deductible mortgage interest. This could happen if:

- Interest Paid is Less Than $600: If the total interest paid during the year is below the $600 threshold, the lender is not required to send you a Form 1098.

- Seller Financing: If you purchased your home through seller financing, the seller (not a financial institution) would be the one to report the interest received. You would need to obtain this information directly from the seller.

- Foreclosure or Bankruptcy: In complex situations involving foreclosure or bankruptcy, the reporting of mortgage interest might differ.

In these instances, you are still responsible for accurately calculating and reporting your deductible mortgage interest. You will need to maintain your own records, such as monthly mortgage statements and payment histories, to substantiate your deduction.

Beyond Mortgage Interest: Other 1098 Series Forms

While Form 1098 is the most common, the “1098 series” of tax forms includes other informational returns that provide details about various types of payments or transactions. Understanding these can offer a broader perspective on tax reporting for different financial activities.

Form 1098-E: Student Loan Interest Statement

This form reports the interest paid on qualified student loans. Similar to Form 1098, it allows borrowers to claim a deduction for student loan interest paid during the year, up to a certain limit. This deduction is an “above-the-line” deduction, meaning you don’t need to itemize to claim it, further enhancing its value to taxpayers.

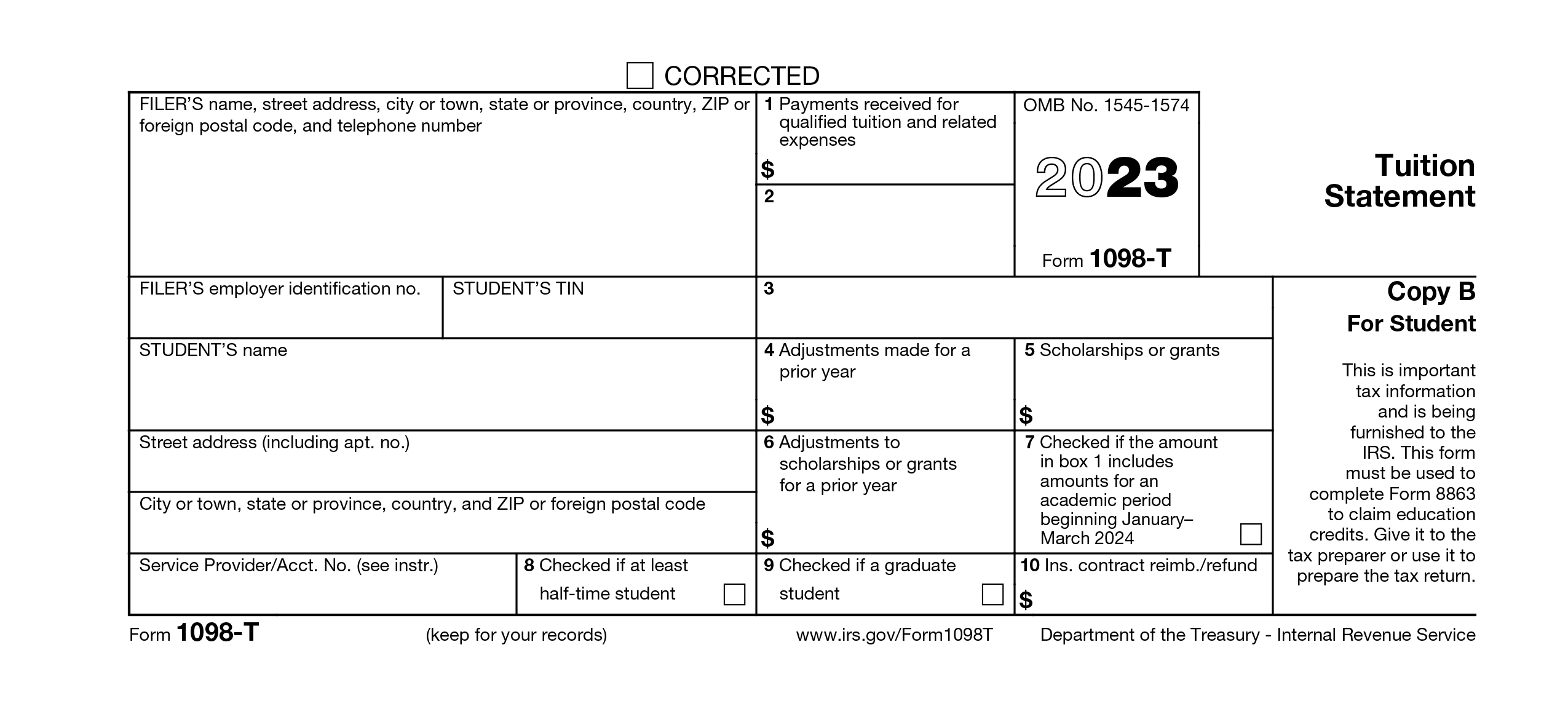

Form 1098-T: Tuition Statement

Form 1098-T is provided by educational institutions to students and the IRS. It reports tuition and related expenses paid, which are crucial for calculating eligibility for education tax credits, such as the American Opportunity Tax Credit and the Lifetime Learning Credit. It is essential to reconcile the information on Form 1098-T with your own records of educational expenses.

Form 1098-C: Contributions of Motor Vehicles, Boats, and Airplanes

This form is used by charities to report the donation of vehicles. It details the vehicle’s sale price and the amount of the donation that is tax-deductible, providing documentation for the donor’s charitable contribution deduction.

Form 1098-F: Fraud Recovery Penalty

This form reports penalties recovered by a taxpayer due to fraudulent actions by a third party. It can be relevant for tax purposes in specific situations involving financial fraud.

Navigating Tax Season with Form 1098

The arrival of tax season can often be a source of stress, but having a clear understanding of important tax forms like Form 1098 can significantly alleviate this burden. For homeowners, Form 1098 serves as a key document that simplifies the process of claiming a valuable tax deduction, potentially leading to substantial savings.

Tips for Managing Your Tax Documents

- Organize Early: As soon as you receive Form 1098 (and other tax documents), file them in a dedicated tax folder or digitally organize them. This prevents last-minute scrambling.

- Read Carefully: Review all information on Form 1098 for accuracy. If you notice any discrepancies, contact your mortgage lender immediately.

- Understand Deductibility Rules: Familiarize yourself with the IRS guidelines for mortgage interest deductibility, especially concerning acquisition debt limits and the use of home equity loans. IRS Publication 936 is an excellent resource.

- Consult a Tax Professional: If your tax situation is complex, or if you are unsure about any aspect of Form 1098 or the mortgage interest deduction, consider consulting a qualified tax advisor or CPA. They can help ensure you are claiming all eligible deductions accurately and efficiently.

By understanding what a Form 1098 is and how it relates to your mortgage interest payments, you can approach tax season with greater confidence, ensuring you take full advantage of the financial benefits available to you as a homeowner.