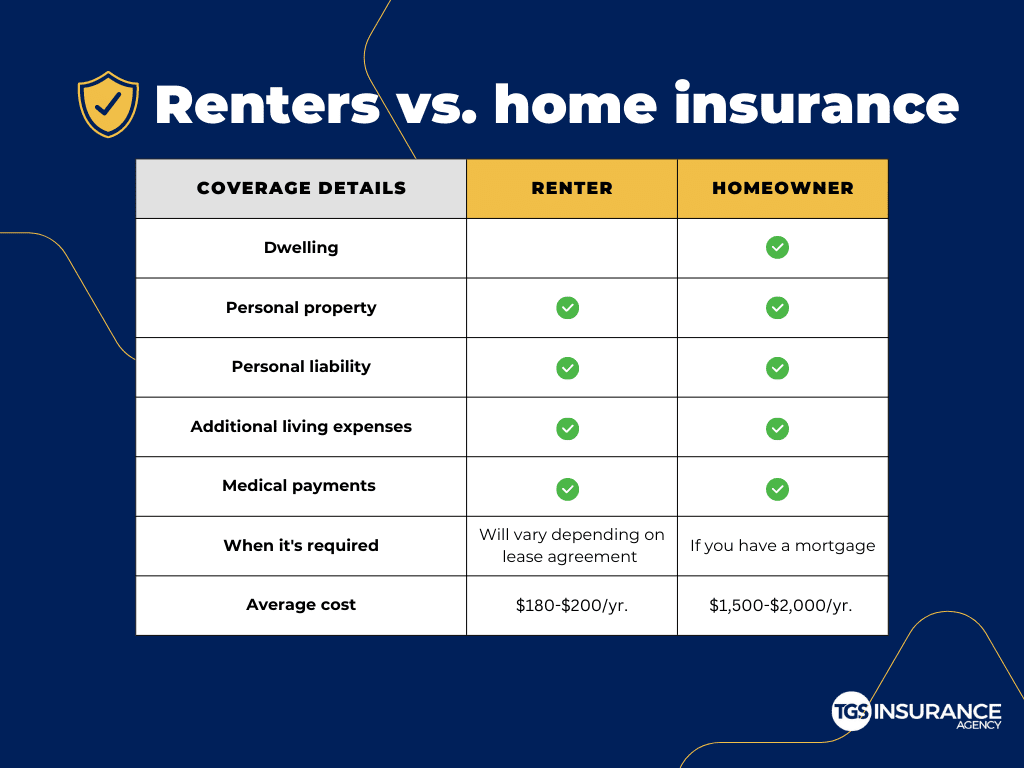

Renters insurance in Texas, much like in other states, serves as a crucial safety net for individuals leasing a property. It’s a contract between a policyholder and an insurance company that provides financial protection against a range of unforeseen events. Understanding the nuances of Texas renters insurance is vital for making informed decisions about safeguarding personal belongings and ensuring financial stability in the event of a loss. While the specific coverage can vary based on the policy and the insurance provider, several core components are generally included.

Personal Property Coverage

The cornerstone of renters insurance is personal property coverage, often referred to as “contents coverage.” This aspect of the policy protects your belongings against damage or theft, regardless of whether the loss occurs within your rented dwelling or elsewhere. Imagine a scenario where your apartment is burglarized, and valuable electronics and jewelry are stolen. Personal property coverage would help reimburse you for the cost of replacing these stolen items, up to your policy’s limits.

What is Covered Under Personal Property?

The scope of “personal property” is broad and encompasses most items you own and use in your daily life. This typically includes:

- Furniture: Sofas, chairs, tables, beds, and other furnishings.

- Electronics: Televisions, computers, gaming consoles, sound systems, and other electronic devices.

- Clothing and Accessories: Apparel, shoes, handbags, and jewelry.

- Appliances: Small kitchen appliances like toasters, blenders, and microwaves (larger appliances typically provided by the landlord may not be covered).

- Household Goods: Dishes, cookware, linens, decorative items, and personal care products.

- Books and Media: Books, CDs, DVDs, and other forms of media.

- Sporting Goods: Bicycles, exercise equipment, and sports gear.

- Valuables: While there are often sub-limits for high-value items like jewelry, furs, and art, these can be covered up to a certain amount. For more expensive items, additional riders or endorsements may be necessary.

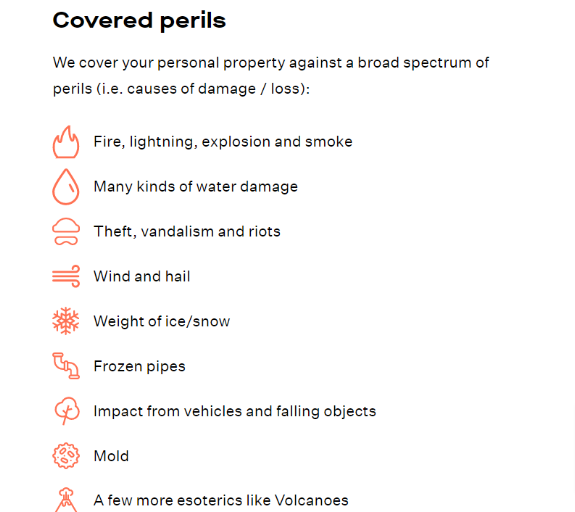

Perils Covered by Personal Property Insurance

Renters insurance policies in Texas typically cover damage or loss to personal property caused by a specific list of “named perils.” These are the events that trigger coverage. The most common named perils include:

- Fire and Smoke: Damage caused by fire originating within your dwelling or from smoke damage.

- Windstorms: Damage from high winds, such as during a hurricane or tornado.

- Hail: Damage caused by hailstones.

- Lightning: Damage from lightning strikes.

- Theft: Loss of property due to burglary or robbery.

- Vandalism: Intentional damage to your property by others.

- Explosion: Damage resulting from an explosion.

- Riot or Civil Commotion: Damage that occurs during riots or public disturbances.

- Falling Objects: Damage caused by objects falling onto your property (e.g., a tree branch).

- Weight of Ice, Snow, or Sleet: Damage caused by the accumulation of these elements.

- Water Damage: Limited water damage, often from sources within the dwelling like a burst pipe or overflowing sink. Crucially, this typically excludes flood damage, which requires separate flood insurance.

- Freezing: Damage caused by the freezing of plumbing, heating, or air conditioning systems.

Actual Cash Value vs. Replacement Cost

When it comes to settling a claim for damaged or stolen personal property, your policy will likely specify whether it pays out based on “Actual Cash Value” (ACV) or “Replacement Cost” (RC).

- Actual Cash Value (ACV): This pays you the current market value of the damaged or stolen item, taking into account depreciation. For example, if your five-year-old television is destroyed, ACV would pay you what that television is worth today, not what a brand-new one would cost.

- Replacement Cost (RC): This pays you the cost to replace the damaged or stolen item with a new one of similar kind and quality, without deduction for depreciation. This is generally more favorable for the policyholder as it allows you to replace your belongings with new items.

It is essential to understand which method your policy uses, as it significantly impacts the payout you would receive in the event of a claim. Many renters opt for replacement cost coverage for greater peace of mind.

Additional Living Expenses (ALE) Coverage

Beyond protecting your belongings, renters insurance in Texas also provides vital financial support if your home becomes uninhabitable due to a covered peril. This coverage is known as Additional Living Expenses (ALE), or sometimes “Loss of Use.” If a fire, for instance, renders your apartment unsafe to live in, ALE coverage can help you cover the extra costs associated with living elsewhere temporarily.

What is Covered Under ALE?

ALE coverage is designed to restore your standard of living while your home is being repaired or rebuilt. This can include a range of expenses, such as:

- Hotel or Motel Stays: The cost of temporary accommodation.

- Rent for a Temporary Residence: If you need to rent another apartment or house.

- Increased Food Costs: If your temporary living situation makes it more expensive to purchase and prepare food (e.g., if you can’t use your kitchen and have to eat out more often).

- Laundry Expenses: If you need to pay for laundry services due to lack of access to facilities.

- Storage Fees: If your belongings need to be stored while your home is being repaired.

- Pet Boarding: Costs associated with boarding pets if your temporary housing doesn’t allow them.

Limits and Duration of ALE Coverage

ALE coverage has specific limits, typically expressed as a percentage of your personal property coverage or as a maximum dollar amount per claim. There may also be a time limit for how long ALE benefits will be paid out, often tied to the estimated repair time. It is crucial to discuss these limits and durations with your insurance provider to ensure adequate coverage.

Liability Protection

Renters insurance in Texas also offers significant liability protection, which is a critical, though sometimes overlooked, component. This coverage safeguards you financially if someone is injured on your rented property or if you or a member of your household accidentally cause damage to someone else’s property.

Bodily Injury Liability

If a guest slips and falls on your wet floor and sustains an injury, they could sue you for medical expenses, lost wages, and pain and suffering. Bodily injury liability coverage within your renters insurance policy can help pay for these costs, including legal defense fees if you are sued.

Property Damage Liability

Similarly, if you accidentally cause damage to a neighbor’s property, such as if a cooking mishap leads to a fire that spreads to their unit, property damage liability can cover the cost of repairs or replacement. This also extends to situations where a pet belonging to you might cause damage to a neighbor’s property.

Medical Payments to Others

This is a smaller, but helpful, part of liability coverage. It can pay for minor medical expenses for guests injured on your property, regardless of who is at fault. This is a “no-fault” coverage designed to quickly resolve small medical incidents and potentially prevent larger liability claims.

What is Typically NOT Covered by Renters Insurance?

While renters insurance provides extensive protection, it’s important to be aware of its limitations. Certain events and types of property are usually excluded from standard policies:

- Flooding: As mentioned earlier, flood damage is almost universally excluded. If you live in a flood-prone area in Texas, you will need to purchase a separate flood insurance policy, typically through the National Flood Insurance Program (NFIP) or a private insurer.

- Earthquakes and Earth Movement: Damage caused by earthquakes or other seismic activity is generally not covered. Earthquake insurance is available as a separate policy.

- Pest Infestations: Damage or loss caused by rodents, insects, or other pests is typically excluded.

- Mold and Mildew: While some policies may offer limited coverage for mold resulting from a covered peril, widespread or pre-existing mold issues are usually not covered.

- Intentional Acts: Damage caused by your own intentional actions or negligence is not covered.

- War and Nuclear Hazard: These catastrophic events are excluded.

- Business Property: If you run a business out of your rented home, inventory, equipment, and other business-related property are generally not covered under a standard renters policy. A separate business policy would be needed.

- Valuable Items Beyond Limits: As noted, high-value items like expensive jewelry, art, or collectibles often have sub-limits. If the value of these items exceeds the sub-limit, you will need to purchase scheduled personal property endorsements (riders) to ensure full coverage.

- Damage to the Structure of the Building: Renters insurance covers your personal belongings and your liability, not the physical structure of the building itself. That responsibility falls on the landlord or property owner, who should have their own landlord insurance.

Understanding Your Texas Renters Insurance Policy

Navigating the world of insurance can seem complex, but for Texas renters, understanding the basics of your policy is a vital step in protecting yourself and your assets. The key lies in carefully reviewing your policy documents, understanding the covered perils, knowing the difference between ACV and RC, and being aware of what is excluded. Don’t hesitate to ask your insurance agent or provider for clarification on any aspect of your coverage. Investing in a renters insurance policy in Texas is a relatively inexpensive way to gain significant peace of mind, knowing that you are financially prepared for many of life’s unexpected challenges.