When navigating the world of consumer electronics, especially high-value items like advanced drones, understanding financing options is crucial. One term that frequently surfaces during the purchase process is “APR,” specifically “Regular Purchase APR.” While not directly a technical drone feature, it’s an integral part of the economic landscape that enables many enthusiasts to acquire the latest aerial technology. This article will demystify what Regular Purchase APR means within the context of acquiring drones and related equipment, exploring its implications for consumers and the purchasing journey.

Understanding the Core Concepts of APR

At its heart, APR, or Annual Percentage Rate, is a more comprehensive measure of the cost of borrowing money than a simple interest rate. It’s designed to give consumers a clearer picture of the total expense associated with a loan or credit line, including not just the interest but also certain fees. When you see “Regular Purchase APR” on a credit card or financing offer for a drone, it refers to the rate applied to your everyday purchases made on that account, as opposed to promotional rates or cash advances.

The Difference Between Interest Rate and APR

While often used interchangeably in casual conversation, the interest rate and APR are distinct. The interest rate is simply the percentage charged on the principal amount of a loan. For example, a credit card might have a 15% interest rate. However, this doesn’t tell the whole story of the cost of borrowing.

APR, on the other hand, takes into account the interest rate and also incorporates other charges that are often associated with obtaining credit. These can include:

- Origination fees: Fees charged to process the loan or credit application.

- Discount points: Fees paid to reduce the interest rate (though less common with credit cards used for regular purchases).

- Annual fees: Fees charged simply for having the credit card account open.

- Monthly maintenance fees: Regular charges for account upkeep.

By including these additional costs, APR provides a more accurate annual cost of credit. When you see “Regular Purchase APR,” it’s this all-encompassing annual cost applied to your general spending on a credit product.

Why is APR Important for Drone Purchases?

Drones, especially high-end models with advanced features like 4K gimbals, sophisticated flight controllers, and long-range FPV systems, can represent a significant financial investment. For many consumers, financing these purchases through credit cards or dedicated financing plans is a common route. Understanding the Regular Purchase APR allows potential buyers to:

- Compare financing offers: Different credit cards or retailers may offer various APRs. Knowing the Regular Purchase APR helps in choosing the most cost-effective option.

- Calculate total costs: By knowing the APR, consumers can estimate the total amount they will pay over time, including interest and fees, when financing a drone.

- Budget effectively: This knowledge aids in financial planning, ensuring that the cost of acquiring the drone doesn’t lead to unforeseen financial strain.

For instance, a drone priced at $2,000 with a Regular Purchase APR of 18% will accrue interest differently than one with a 22% APR. Over the life of the repayment period, this difference can amount to hundreds of dollars, directly impacting the overall affordability of the drone.

Deconstructing “Regular Purchase APR”

The term “Regular Purchase APR” is specifically designed to distinguish the standard rate applied to everyday transactions from other potential rates that might exist on a credit account. This is particularly relevant for credit cards, which often have multiple APRs for different types of transactions.

The Distinction from Promotional APRs

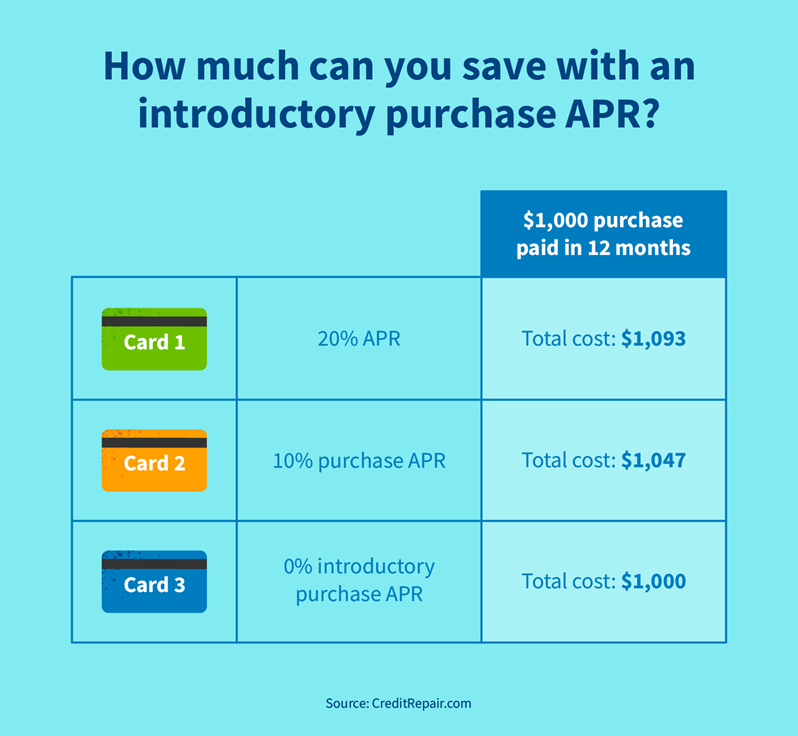

Many credit card offers, especially those marketed towards large purchases like electronics, include introductory promotional APRs. These might be 0% APR for a specific period (e.g., 6, 12, or 18 months). While highly attractive, it’s crucial to understand what happens after this promotional period ends.

The “Regular Purchase APR” is the rate that takes effect once the promotional period expires. If you finance a drone with a 0% introductory APR and haven’t paid off the balance by the end of the promotional term, the remaining balance will be subject to the Regular Purchase APR. This can lead to a sudden and significant increase in the cost of your purchase if not managed carefully.

Example: You purchase a $3,000 professional drone using a credit card with a 12-month 0% introductory APR. If you still owe $1,500 after 12 months, that remaining balance will then accrue interest at the card’s Regular Purchase APR, which might be 19.99%. This means you’ll start paying a substantial amount in interest on that remaining balance.

Understanding Variable vs. Fixed APRs

Most credit cards, including those offering a Regular Purchase APR, utilize a variable APR. This means the APR can fluctuate over time, typically tied to a benchmark interest rate, such as the Prime Rate. If the Prime Rate increases, your Regular Purchase APR will likely increase as well, leading to higher borrowing costs.

A fixed APR, on the other hand, remains constant throughout the life of the loan or credit account. While less common for standard credit cards, some personal loans or specific financing plans might offer a fixed APR. It’s important to check the terms and conditions of any credit offer to understand whether the Regular Purchase APR is variable or fixed.

Other APRs to Be Aware Of

Beyond the Regular Purchase APR, credit cards might also list:

- Balance Transfer APR: The rate applied to balances transferred from other credit cards. This can sometimes be a promotional rate, but the regular rate for balance transfers will apply afterwards.

- Cash Advance APR: Typically much higher than the Regular Purchase APR, this is the rate applied to cash withdrawals made using the credit card.

- Penalty APR: This is an exceptionally high APR that may be applied if you miss payments or violate other terms of your credit agreement.

For consumers focused on purchasing a drone, the Regular Purchase APR is the primary rate of concern for the initial transaction. However, being aware of these other APRs is vital for responsible credit management.

The Impact of Regular Purchase APR on Drone Financing

The Regular Purchase APR has a direct and significant impact on the total cost of purchasing a drone when financing is involved. This is particularly true for higher-priced drones that require substantial financing.

Calculating the True Cost of a Financed Drone

When you finance a drone, the Regular Purchase APR dictates how much interest you will pay over time. This interest is added to your principal balance, increasing the overall amount you owe.

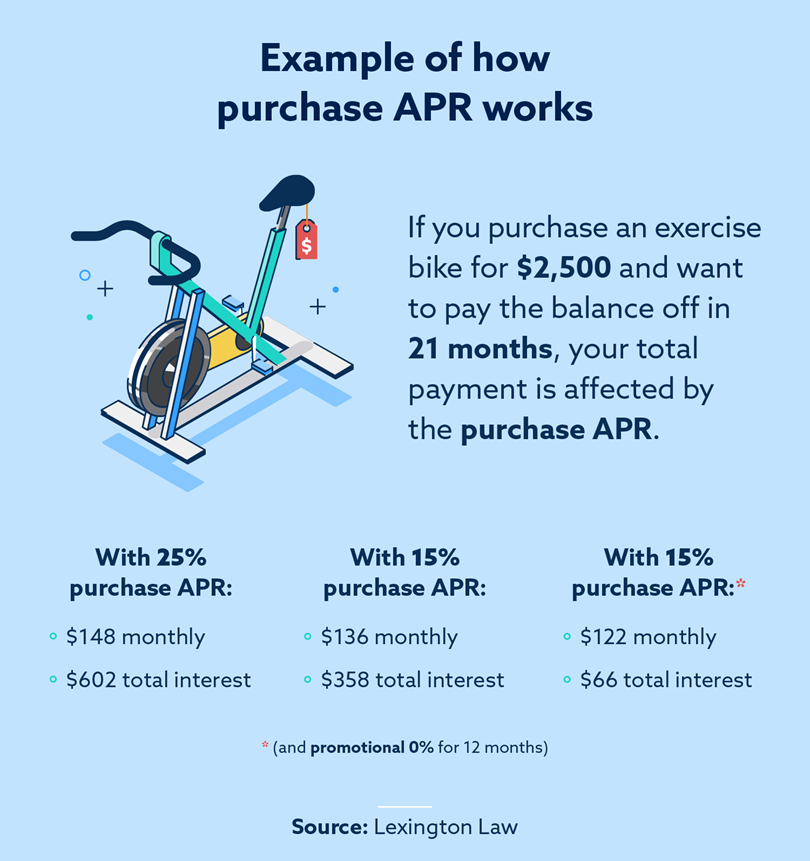

Illustrative Calculation:

Let’s consider purchasing a drone for $2,500.

- Scenario A: 0% Intro APR for 12 months, then 19.99% Regular Purchase APR.

If you pay off $1,000 within the first 12 months and owe $1,500 after, and then take another 24 months to pay off the remaining $1,500 at 19.99% APR, the total interest paid on that remaining balance would be approximately $390. The total cost would be $2,500 (drone price) + $390 (interest) = $2,890. - Scenario B: 15% Regular Purchase APR from the start.

If you were to finance the entire $2,500 at 15% APR over 36 months (a common repayment period for larger purchases), the total interest paid would be approximately $640. The total cost would be $2,500 + $640 = $3,140.

These scenarios highlight how the Regular Purchase APR, especially when it kicks in after a promotional period, can substantially increase the final price of the drone.

Strategies for Minimizing APR Costs

To make the acquisition of a new drone more financially manageable and to avoid excessive interest charges, consumers can employ several strategies:

- Maximize Down Payment: The larger the down payment you make, the smaller the principal amount you need to finance. This directly reduces the amount of interest that will accrue, regardless of the APR.

- Pay Off Promotional Balances Quickly: If you utilize a 0% introductory APR offer, create a rigorous payment plan to pay off the entire balance before the promotional period ends. This effectively allows you to purchase the drone interest-free.

- Choose Cards with Lower Regular APRs: If you anticipate needing to carry a balance, compare credit cards and look for those with a lower Regular Purchase APR. While 0% APR offers are enticing, a consistently lower regular APR might be more beneficial in the long run for those who might struggle to pay off the balance within a promotional period.

- Consider Retailer Financing or Personal Loans: Some drone retailers offer their own financing options, which may have different APR structures. Additionally, a personal loan from a bank or credit union could potentially offer a lower fixed APR than a credit card’s variable rate. Always compare the terms and total costs.

- Avoid Minimum Payments: Making only the minimum payment on a financed purchase will significantly extend the repayment period and dramatically increase the total interest paid due to compounding. Aim to pay as much as you can above the minimum.

Navigating Credit Offers for Tech Purchases

The technology sector, including the drone industry, often sees aggressive marketing of credit and financing options to make high-ticket items more accessible. Understanding the nuances of terms like “Regular Purchase APR” is a crucial part of being a savvy consumer.

Reading the Fine Print: What to Look For

When presented with a credit offer for a drone purchase, it’s imperative to meticulously read all terms and conditions. Pay close attention to:

- The specific APR for purchases: Ensure you are looking at the Regular Purchase APR and not other rates.

- The length of any introductory APR period: Know exactly when the promotional rate ends and the Regular Purchase APR begins.

- The benchmark rate for variable APRs: Understand how your APR can change.

- Any fees associated with the account: Annual fees, late payment fees, and other charges can add to the overall cost.

- The calculation method for interest: How is the interest calculated on your balance?

The Role of Credit Scores in APR

It’s also important to remember that the APR you are offered is heavily influenced by your creditworthiness. Individuals with higher credit scores are typically offered lower APRs, reflecting a lower perceived risk by the lender. Conversely, those with lower credit scores may be offered higher APRs, or even denied credit altogether. Maintaining a good credit score is therefore an indirect but significant factor in managing the cost of financing tech purchases like drones.

Responsible Use of Credit for Hobbyists

For drone enthusiasts, especially those looking to invest in professional-grade equipment, understanding Regular Purchase APR empowers them to make informed financial decisions. It transforms a potentially confusing array of credit terms into actionable knowledge, allowing for the acquisition of desired technology without falling into debt traps. By being aware of what Regular Purchase APR means, consumers can confidently navigate financing options and ensure their passion for aerial technology remains an enjoyable and financially sound pursuit.