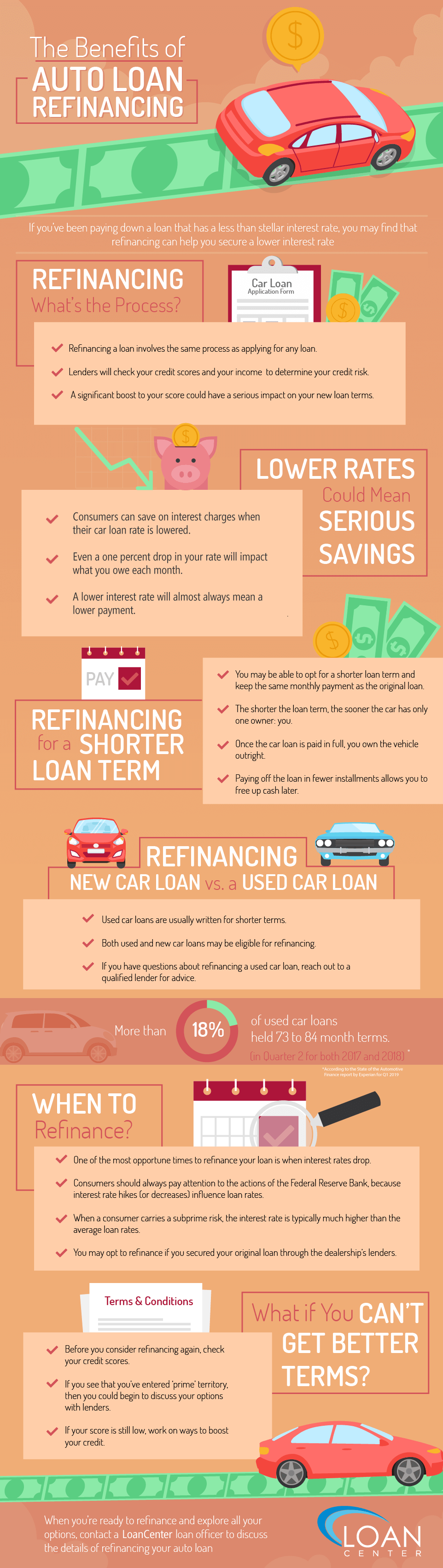

Refinancing a car is a financial maneuver that involves taking out a new auto loan to pay off your existing car loan. The primary motivations behind this decision are typically to secure a lower interest rate, reduce your monthly payments, or shorten the loan term. Essentially, you’re replacing your current loan with a new one from a different lender, or sometimes even from your current lender, under potentially more favorable terms. Understanding the mechanics and implications of refinancing is crucial for making an informed financial decision that can significantly impact your budget and overall financial health.

Understanding the Fundamentals of Auto Refinancing

At its core, refinancing a car loan is akin to a mortgage refinance, but for your vehicle. When you originally purchased your car, you likely secured an auto loan with a specific interest rate, loan term, and monthly payment. Over time, your financial circumstances may have improved, or market interest rates may have decreased, creating an opportunity to obtain better loan conditions. Refinancing allows you to capitalize on these changes.

The Mechanics of a Refinance Transaction

The process begins with identifying a lender willing to offer you a new loan. This lender will assess your creditworthiness, similar to when you initially applied for your car loan. They will consider your credit score, income, employment history, and the loan-to-value ratio of your vehicle. If approved, the new lender will provide you with the funds to pay off your existing loan in full. You then begin making payments to the new lender under the terms of your refinanced loan.

The key benefit is the potential for a lower Annual Percentage Rate (APR). Even a small reduction in interest can translate into substantial savings over the life of the loan, especially for longer loan terms. For instance, reducing your APR by 2% on a $20,000 loan with a remaining term of five years can save you thousands of dollars in interest.

Key Differences from Your Original Loan

Your original auto loan was secured when you purchased the vehicle. Refinancing essentially replaces that contract. The new loan may have a different interest rate, a different repayment period (shorter or longer), and consequently, a different monthly payment amount. It’s important to scrutinize the details of the new loan offer. Does it offer a lower interest rate? Does it extend the loan term significantly, which could lead to paying more interest overall despite lower monthly payments? These are critical questions to ask.

Furthermore, the equity in your car plays a role. If your car is worth more than the outstanding balance of your loan, you have positive equity. This can make you a more attractive borrower and potentially qualify you for better terms. Conversely, if you owe more than the car is worth (a negative equity or “upside-down” loan), refinancing can be more challenging.

The Primary Benefits of Refinancing Your Car

The decision to refinance is driven by a desire for tangible financial advantages. These benefits can range from immediate cost savings to improved financial flexibility.

Lowering Your Monthly Payments

One of the most common reasons individuals refinance their car loans is to reduce their monthly financial obligations. This can be achieved by securing a lower interest rate or by extending the loan term. A lower interest rate directly reduces the amount of interest paid each month. Extending the loan term, while potentially increasing the total interest paid over the life of the loan, spreads the principal balance over a longer period, thereby lowering the individual monthly payment. This can provide much-needed breathing room in a tight budget, freeing up cash for other expenses, savings, or investments.

For example, imagine you have a $15,000 loan balance remaining with a 6% APR over three years (36 months), resulting in a monthly payment of approximately $450. If you can refinance to a 4% APR over the same term, your monthly payment could drop to around $430, saving you $20 each month. If you opt for a longer term, say four years (48 months) at 4% APR, your monthly payment might decrease to about $330, a significant reduction, but you’d be paying interest for an additional year.

Reducing the Total Interest Paid

While lowering monthly payments is often the immediate goal, another significant benefit of refinancing is the potential to reduce the total amount of interest paid over the life of the loan. This is primarily achieved by securing a lower interest rate. If you refinance to a significantly lower APR, even if you maintain the same loan term, you will pay substantially less in interest charges by the time the loan is fully repaid. This is a powerful way to save money without necessarily altering your monthly budget significantly.

Consider the previous example:

- Original Loan: $15,000 at 6% APR for 36 months. Total interest paid ≈ $1,200.

- Refinance (same term): $15,000 at 4% APR for 36 months. Total interest paid ≈ $800.

In this scenario, refinancing results in a saving of approximately $400 in interest over the loan’s life. This illustrates the power of securing a lower interest rate.

Shortening the Loan Term

Conversely, refinancing can also be used to shorten the loan term. If your financial situation has improved, you might be able to afford higher monthly payments. By refinancing to a new loan with a shorter repayment period, you can pay off your car loan faster and become debt-free sooner. This strategy typically involves accepting a slightly higher monthly payment than your current one, but it results in significant interest savings and quicker debt elimination.

For instance, if you have a $10,000 loan balance with two years remaining at 5% APR, your monthly payment might be around $439. If you can refinance to a new two-year loan at the same 5% APR, your payment remains similar. However, if you manage to secure a 4% APR for a two-year term, your monthly payment might drop to about $434, and you’ll still be paying off the loan faster than if you had a longer term. The real benefit of shortening the term comes when combined with a lower interest rate or if you simply decide to pay more than the minimum required.

Improving Financial Flexibility

Beyond direct cost savings, refinancing can offer enhanced financial flexibility. When monthly car payments are reduced, it frees up discretionary income. This additional cash can be allocated towards other financial goals, such as building an emergency fund, paying down higher-interest debt (like credit cards), saving for a down payment on a home, or investing. This increased liquidity can provide peace of mind and accelerate progress towards broader financial objectives.

Factors to Consider Before Refinancing

While the benefits of refinancing are compelling, it’s not a universally beneficial decision. Several critical factors must be evaluated to ensure it aligns with your financial goals and circumstances.

Your Credit Score and History

Your credit score is arguably the most significant determinant of whether you’ll qualify for refinancing and at what interest rate. Lenders use your credit score to assess your risk as a borrower. A higher credit score generally indicates a lower risk, leading to more favorable interest rates and loan terms. If your credit score has improved since you obtained your original car loan, you are likely a strong candidate for refinancing at a lower APR.

Conversely, if your credit score has declined, you may not qualify for a better rate, or you might even be offered a higher one. It’s essential to check your credit report and score before applying. If there are errors on your report, take steps to correct them. If your score is low, focus on improving it before attempting to refinance.

The Age and Mileage of Your Vehicle

Lenders often have restrictions on the age and mileage of vehicles they will refinance. Older cars with high mileage generally have lower market values and are considered higher risk. Many lenders prefer to refinance vehicles that are no longer than 7-10 years old and have fewer than 100,000 miles. If your car is older or has accumulated significant mileage, you may find it difficult to find a lender willing to refinance your loan. It’s crucial to research lenders’ specific criteria regarding vehicle age and mileage.

The Loan-to-Value (LTV) Ratio

The loan-to-value ratio compares the amount you owe on your car to its current market value. Lenders assess this ratio to understand the risk involved. A lower LTV ratio (meaning you owe less than the car is worth) is more favorable. Many lenders prefer an LTV of 125% or less, meaning the loan balance is no more than 125% of the car’s value. If you owe significantly more than your car is worth (a negative equity situation), it can be challenging to refinance. In such cases, you might need to wait until you’ve paid down more of the loan or the car’s value increases relative to the loan balance.

Associated Fees and Costs

Refinancing isn’t always free. There can be various fees associated with the process, such as application fees, origination fees, title transfer fees, and documentation fees. These costs can offset some or all of the potential savings from a lower interest rate. It’s vital to calculate the total cost of refinancing by adding up all associated fees and comparing it to the total interest savings. If the fees are substantial, they might make refinancing less attractive, especially if the interest rate savings are minimal. Always ask for a complete breakdown of all fees upfront.

The Refinancing Process: A Step-by-Step Guide

Navigating the refinancing process can seem daunting, but by breaking it down into manageable steps, it becomes a straightforward procedure.

Step 1: Assess Your Current Loan and Financial Situation

Before you begin looking for new lenders, thoroughly review your current car loan. Understand the remaining balance, the current interest rate (APR), the monthly payment, and the number of months left in the loan term. Simultaneously, evaluate your current financial standing. Has your credit score improved? Is your income stable? A clear understanding of your current situation will help you determine if refinancing is a viable option and what terms you might qualify for.

Step 2: Check Your Credit Score and Report

Obtain copies of your credit report from the three major credit bureaus (Equifax, Experian, and TransUnion) and check your credit score. Many financial institutions offer free credit score access. Review your report for any errors and dispute them if found. A strong credit score is your most valuable asset when seeking a new loan.

Step 3: Research and Compare Lenders

Shop around for the best refinancing offers. This involves contacting various lenders, including banks, credit unions, and online auto loan providers. Many lenders allow you to get pre-qualified without a hard credit inquiry, which can give you an estimate of the interest rate you might receive. Compare the APR, loan terms, monthly payments, and any associated fees from different lenders. Don’t be afraid to negotiate.

Step 4: Gather Necessary Documentation

Once you’ve identified a lender, you’ll need to complete a formal loan application. Be prepared to provide documentation such as proof of income (pay stubs, tax returns), proof of residency (utility bills), your driver’s license, and details about your current car loan and vehicle.

Step 5: Submit Application and Finalize the Loan

Submit your completed application and all required documents to your chosen lender. The lender will perform a hard credit inquiry, which may slightly impact your credit score. If approved, you will receive a loan offer. Review the terms carefully. Once you accept the offer, the lender will disburse the funds to pay off your old loan, and you will begin making payments on your new refinanced loan.

When Refinancing Might Not Be the Right Choice

While refinancing offers numerous advantages, there are specific situations where it may not be the optimal financial decision.

When Your Credit Score Has Decreased

As mentioned, a declining credit score can hinder your ability to secure a better interest rate. If your credit has worsened since you took out your original loan, you might not qualify for refinancing, or you could end up with a higher APR and less favorable terms, negating any potential benefits. In such cases, focusing on improving your credit score by making on-time payments and reducing debt is a more prudent approach.

When the Loan Term is Extended Too Significantly

While extending the loan term can lower monthly payments, it can also lead to paying substantially more interest over the life of the loan. If the goal is to save money, a significant extension of the loan term might not be beneficial, even with a slightly lower interest rate. It’s crucial to balance the immediate relief of lower monthly payments with the long-term cost of interest. A common rule of thumb is to avoid extending the loan term by more than a year or two unless absolutely necessary.

When Associated Fees Are High

If the fees associated with refinancing are substantial, they could outweigh the interest savings. For example, if you can only secure a 0.5% reduction in APR, but the origination and documentation fees add up to several hundred dollars, the net savings might be negligible or even negative. Always calculate the breakeven point to understand how long it will take for the interest savings to recoup the refinancing costs.

When You Are Close to Paying Off the Loan

If you only have a few months or a year left on your car loan, the effort and potential costs of refinancing may not be worthwhile. The remaining interest you would pay is likely minimal, and the administrative hassle of refinancing could outweigh any small savings. It’s often more practical to simply continue making your current payments and become debt-free sooner.

In conclusion, refinancing a car loan can be a powerful financial tool for saving money, reducing monthly payments, and improving financial flexibility. However, it requires careful consideration of your creditworthiness, vehicle’s condition, loan terms, and associated costs. By understanding the process and its implications, individuals can make informed decisions that align with their financial goals.