Florida’s unique approach to auto insurance, known as “no-fault” insurance, has been a subject of considerable discussion and often confusion for drivers. At its core, the no-fault system aims to expedite the payment of medical expenses and lost wages for individuals injured in car accidents, regardless of who was at fault for the collision. This system, enshrined in Florida Statute Chapter 627, Part I, dictates how insurance claims are handled after an accident, impacting both drivers and their insurers. Understanding its intricacies is crucial for navigating insurance policies and accident claims effectively.

The Pillars of Florida’s No-Fault System

Florida’s no-fault law mandates that all drivers carry a minimum level of Personal Injury Protection (PIP) coverage. This coverage is designed to provide prompt payment for medical bills and a portion of lost wages for you and your passengers, up to your policy limits, irrespective of fault. This immediate financial relief is the primary benefit of the no-fault system, intended to prevent lengthy disputes over liability from delaying necessary medical treatment.

Personal Injury Protection (PIP) Explained

Personal Injury Protection (PIP) is the cornerstone of Florida’s no-fault insurance. Every Florida driver is required to carry at least $10,000 in PIP coverage. This coverage applies to injuries sustained by the policyholder, their resident relatives, and their passengers, regardless of who caused the accident. PIP covers a broad range of expenses, including:

- Medical Expenses: This is the most significant component of PIP. It covers reasonable and necessary medical treatment, including hospital stays, doctor visits, surgery, diagnostic tests, and rehabilitation services. There is typically a 14-day rule for seeking medical treatment for the expenses to be covered by PIP. If you don’t seek treatment within 14 days of the accident, your PIP benefits may be reduced or eliminated.

- Lost Wages: PIP covers 80% of lost wages if you are unable to work due to injuries sustained in an accident. This is capped at $5,000 per person. This benefit is crucial for individuals who rely on their income to manage daily expenses.

- Death Benefits: In the unfortunate event of a fatality, PIP coverage includes a death benefit of $5,000 per person. This benefit is intended to assist with funeral expenses and other immediate costs.

- Replacement Services: PIP can also cover the cost of essential services you can no longer perform due to your injuries, such as household chores, childcare, and yard work. This is capped at $1,000.

The 80/20 Rule and Benefit Caps

A critical aspect of PIP is the 80/20 rule. PIP coverage pays 80% of your necessary and reasonable medical expenses and 60% of your lost wages. This means that while PIP provides initial coverage, it doesn’t cover 100% of your losses. The caps on lost wages ($5,000) and replacement services ($1,000) also highlight that PIP is intended as an initial safety net, not a comprehensive solution for all accident-related expenses.

The $10,000 Threshold

Florida law requires drivers to have at least $10,000 in PIP coverage. This amount is considered the minimum to provide a baseline of financial protection for medical expenses and lost wages. However, many drivers opt for higher PIP limits to ensure more substantial coverage in the event of a serious injury.

Proof of Insurance and Compliance

Maintaining proof of insurance is a legal requirement for all Florida drivers. This typically includes your insurance card with your PIP coverage details. Failure to maintain the required PIP coverage can result in penalties, including license and registration suspension, fines, and even impoundment of your vehicle.

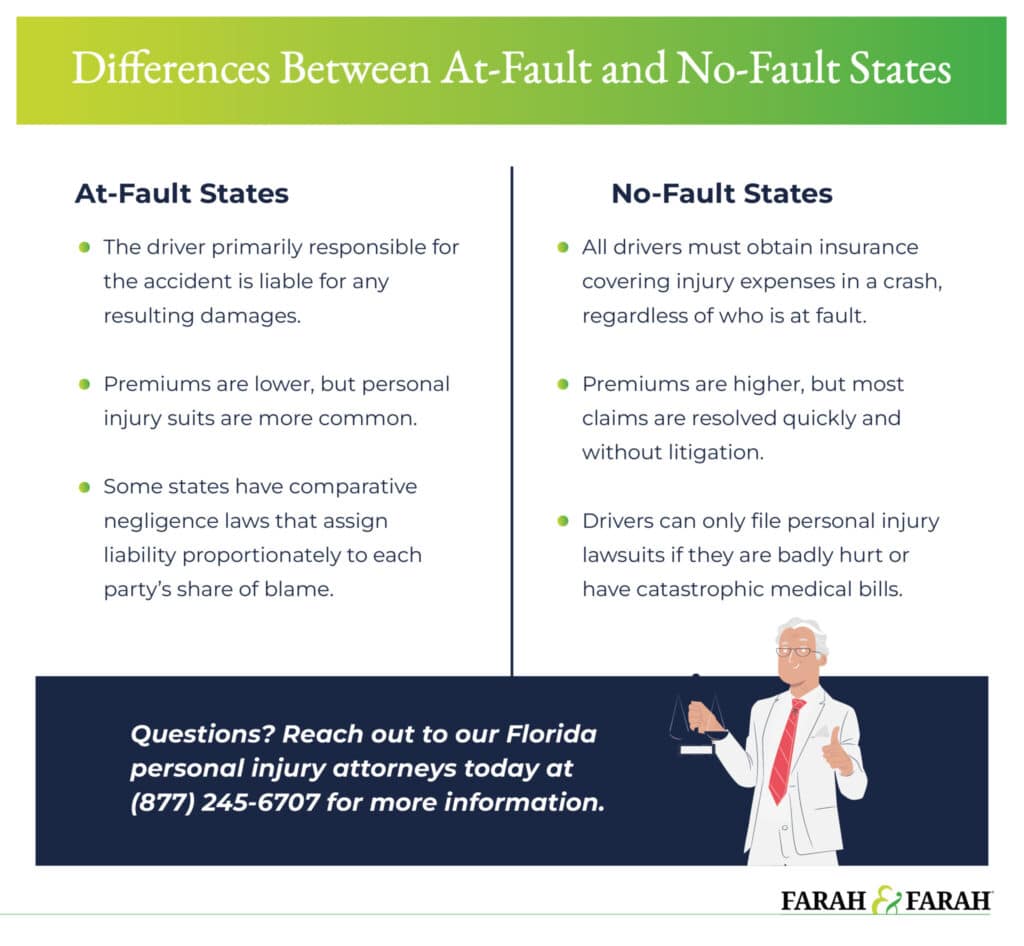

When Does “At-Fault” Matter in Florida?

While Florida’s no-fault system prioritizes prompt payment of initial medical bills and lost wages, it does not eliminate the concept of fault entirely. The system is designed to allow individuals to recover more significant damages beyond what PIP covers, but only if they can prove the other party was at fault and their injuries meet certain criteria. This is where the concept of “serious injury” becomes paramount.

The Serious Injury Threshold

To pursue compensation from the at-fault driver’s insurance for pain, suffering, and other non-economic damages (such as mental anguish), an injured party must demonstrate that they sustained a “serious injury.” Florida Statute 627.737 defines a serious injury as one that meets any of the following criteria:

- Death: As mentioned earlier, a fatality resulting from the accident automatically meets the serious injury threshold.

- Disfigurement: A significant and permanent disfigurement, such as severe scarring or loss of a limb, qualifies as a serious injury.

- Permanent Injury: This is a broad category encompassing injuries that are permanent in nature, meaning they are not expected to improve significantly over time. This could include nerve damage, loss of function, or chronic pain that significantly impacts daily life.

- Significant and Permanent Loss of an Important Bodily Function: This refers to the loss or substantial impairment of a crucial bodily function, such as the ability to walk, see, or use one’s hands effectively.

- More than 50% of a permanent impairment: This refers to a medical determination that an individual has suffered a permanent impairment that exceeds 50% of their total body function.

The Role of Bodily Injury Liability (BIL) Insurance

While PIP covers initial expenses regardless of fault, Bodily Injury Liability (BIL) insurance is what covers damages when the other driver is at fault and the serious injury threshold is met. BIL coverage is not mandatory in Florida, but it is highly recommended. If you are found to be at fault for an accident and the other driver has suffered a serious injury, your BIL coverage can protect you from significant financial liability. Conversely, if the other driver is at fault and meets the serious injury threshold, their BIL coverage will be the primary source for your non-economic damages.

Tort Recovery and Damages

If an injured party meets the serious injury threshold, they can pursue a tort claim against the at-fault driver. In a tort claim, an individual can seek compensation for a wider range of damages beyond what PIP covers, including:

- Pain and Suffering: This compensates for the physical pain and emotional distress caused by the accident.

- Mental Anguish: This covers the psychological impact of the accident, such as anxiety, depression, and post-traumatic stress disorder.

- Loss of Enjoyment of Life: This compensates for the inability to participate in activities and hobbies that were once enjoyed.

- Loss of Consortium: This may be claimed by a spouse for the loss of companionship, affection, and services of their injured partner.

- Future Medical Expenses: If future medical treatment is anticipated, compensation for these costs can be sought.

- Lost Earning Capacity: If the injuries prevent the individual from earning as much as they could have before the accident, they can seek compensation for this diminished earning capacity.

Criticisms and Considerations of Florida’s No-Fault System

Despite its intention to provide prompt relief, Florida’s no-fault system has faced its share of criticism and has undergone various reforms over the years. Some argue that the system can lead to undercompensation for serious injuries, while others point to potential for fraud and abuse.

Challenges in Proving Serious Injury

One of the most significant challenges for individuals injured in an accident is proving that they have met the “serious injury” threshold. This often requires extensive medical documentation, expert medical opinions, and can lead to complex legal battles. Without meeting this threshold, recovery for non-economic damages is significantly limited.

Potential for Undercompensation

Critics argue that the $10,000 PIP limit, combined with the 80/20 rule, can leave individuals with significant medical bills undercompensated, particularly in cases involving severe injuries requiring extensive treatment and rehabilitation. While some drivers opt for higher PIP coverage, the mandatory minimum may not be sufficient for many.

Fraud and Abuse

Like any insurance system, Florida’s no-fault system has been susceptible to fraud and abuse. This can include staged accidents, inflated medical billing, and unnecessary medical treatment. These practices can drive up insurance costs for all policyholders.

Impact of Reforms

Florida’s no-fault law has been amended several times in an effort to address these issues. For instance, reforms have aimed to curb insurance fraud, strengthen verification processes for medical treatment, and adjust benefit levels. Understanding the current version of the law and any recent legislative changes is crucial for drivers.

Beyond the Basics: Optional Coverages and Best Practices

While Florida law mandates a minimum level of PIP coverage, drivers have the option to purchase additional insurance to enhance their protection. Understanding these optional coverages can provide greater financial security in the event of an accident.

Collision Coverage

Collision coverage helps pay to repair or replace your vehicle after an accident, regardless of who is at fault. This coverage is particularly important if you have a newer or more valuable vehicle and want to ensure it can be repaired or replaced if damaged in an accident.

Comprehensive Coverage

Comprehensive coverage addresses damage to your vehicle from events other than collisions, such as theft, vandalism, fire, or natural disasters like hail or falling trees.

Uninsured/Underinsured Motorist (UM/UIM) Coverage

This is a vital optional coverage that protects you if you are involved in an accident with a driver who has no insurance (uninsured) or insufficient insurance (underinsured) to cover your damages. UM/UIM coverage can step in to cover your medical expenses, lost wages, and even pain and suffering, up to your policy limits. Given the number of uninsured drivers on the road, this coverage is highly recommended.

Medical Payments (MedPay) Coverage

MedPay is an optional coverage that can supplement your PIP benefits. It typically covers medical expenses and funeral expenses for you and your passengers, regardless of fault, and often has higher limits than PIP. MedPay can also cover expenses that PIP does not, such as deductibles or expenses incurred after PIP benefits are exhausted.

Best Practices for Florida Drivers

- Review Your Policy Annually: Insurance needs can change. It’s wise to review your auto insurance policy at least once a year to ensure it still meets your needs and that you understand your coverage.

- Understand Your Deductibles: For coverages like collision and comprehensive, be aware of your deductible – the amount you pay out-of-pocket before your insurance coverage begins.

- Consult with an Insurance Professional: If you are unsure about your coverage or need help selecting the right policies, consult with an independent insurance agent. They can help you understand your options and tailor a policy to your specific circumstances.

- Keep Records: Maintain copies of your insurance policy, accident reports, and all medical bills and receipts. This documentation is crucial if you need to file a claim or pursue legal action.

By understanding the nuances of Florida’s no-fault system, including the role of PIP, the serious injury threshold, and the importance of optional coverages, drivers can better protect themselves and navigate the complexities of auto insurance in the Sunshine State.