The financial landscape for homeowners is often a complex terrain, filled with terms and processes that can feel daunting. Among these, the concept of “recasting a mortgage” stands out as a potentially valuable tool for managing homeownership finances. While the term itself might sound technical, its implications are quite practical and can offer significant benefits, particularly for those looking to adjust their monthly payments or leverage existing home equity without refinancing. Understanding what it means to recast a mortgage is the first step in determining if it’s the right strategy for your financial goals.

At its core, recasting a mortgage is a specific type of loan modification where the outstanding loan balance is recalculated. Crucially, this process does not alter the original interest rate or the loan term. Instead, it effectively resets the mortgage with a new amortization schedule based on the current outstanding principal balance. This is often achieved by making a substantial lump-sum payment towards the principal, thereby reducing the overall debt. The lender then recalculates your monthly principal and interest payments over the remaining life of the loan, resulting in lower payments. It’s important to distinguish this from refinancing, which involves obtaining a completely new loan, potentially with a new interest rate, loan term, and associated closing costs. Recasting is generally a simpler, less costly process focused solely on adjusting the payment amount.

The Mechanics of Mortgage Recasting

To truly grasp what it means to recast a mortgage, it’s essential to understand the underlying mechanics. A mortgage payment is comprised of two main components: principal and interest. Over the life of a standard amortizing loan, the proportion of interest paid is higher in the early years, gradually shifting towards a larger principal portion as the loan matures. When you make a principal-only payment, you directly reduce the amount of money on which interest is calculated. This is the linchpin of recasting.

The Role of Principal Reduction

The primary driver behind a mortgage recast is a significant reduction in the principal balance. This reduction can stem from various sources:

- Large Lump-Sum Payments: The most common method is making a substantial payment that is specifically designated to reduce the principal. This could come from an inheritance, a bonus, savings, or the sale of another asset. The key is that this payment is applied directly to the principal and not spread across future payments.

- Sale of Unused Home Equity: In some cases, if a portion of the home has been legally separated or if there was an overpayment that has accumulated, these funds could be applied to the principal. However, this is less common and typically requires specific legal and financial structuring.

- Escrow Surplus (Rare): While not the primary method, in rare instances where an escrow account has a significant surplus that the lender is willing to apply to the principal, it could contribute to a recast. However, lenders usually address escrow surpluses by adjusting future payments or issuing a refund.

Once this lump sum is applied to the principal, the lender essentially re-amortizes the loan. This means they recalculate the monthly payment required to pay off the new, lower principal balance over the remaining term of the original loan at the original interest rate. For example, if you have 20 years left on a 30-year mortgage and you make a $50,000 principal-only payment, your lender will recalculate the monthly payments needed to pay off the reduced balance in those remaining 20 years, using your original interest rate. The outcome is a lower monthly payment.

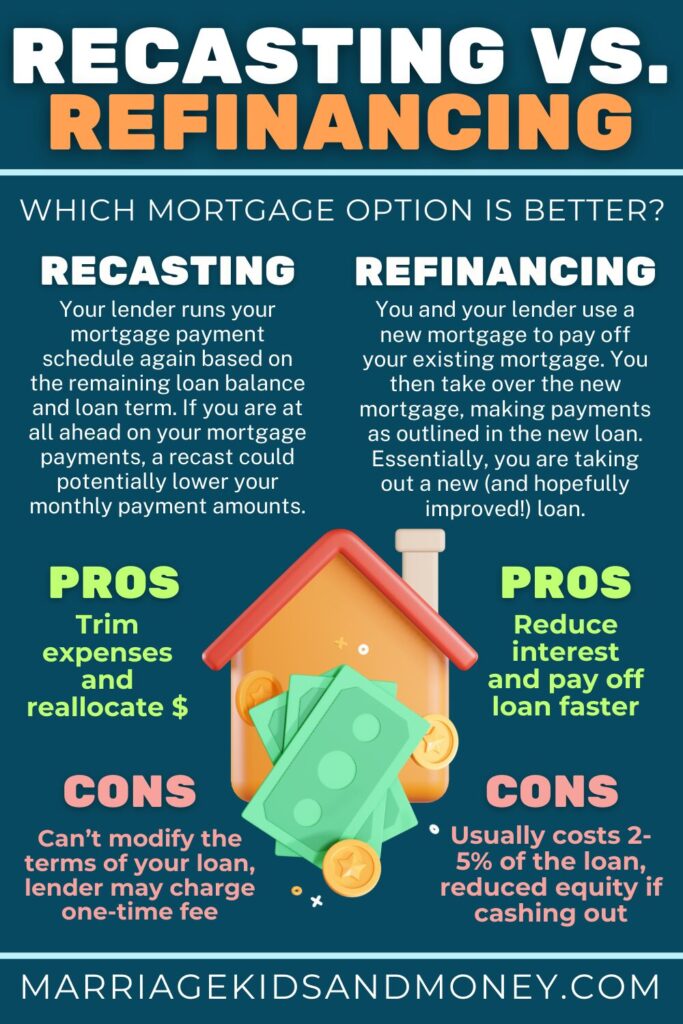

Distinguishing Recasting from Refinancing

The confusion between recasting and refinancing is widespread, largely because both can lead to lower monthly mortgage payments. However, their fundamental processes and implications differ significantly:

-

Recasting:

- Process: Loan modification where the principal balance is reduced, and payments are re-amortized over the remaining term at the original interest rate.

- Interest Rate: Remains the same.

- Loan Term: Remains the same (original loan term, but with fewer years remaining).

- Closing Costs: Typically minimal to none. Lenders may charge a small administrative fee.

- Credit Impact: Minimal to none, as it’s not a new loan application.

- Purpose: Primarily to lower monthly payments without changing the interest rate or extending the loan term.

-

Refinancing:

- Process: Obtaining an entirely new mortgage loan to pay off the existing one. This involves a new application, underwriting process, and closing.

- Interest Rate: Can be the same, lower, or higher, depending on market conditions and your creditworthiness.

- Loan Term: Can be reset (e.g., to a new 30-year term), extended, or shortened.

- Closing Costs: Significant, similar to obtaining a new mortgage (appraisal fees, title insurance, origination fees, etc.).

- Credit Impact: A hard credit inquiry is performed, and the new loan appears on your credit report.

- Purpose: To lower monthly payments, reduce the interest rate, shorten the loan term, or cash out equity.

Therefore, if your primary goal is to reduce your monthly payment without altering your interest rate or loan term, and you have a substantial sum to put towards your principal, recasting is likely the more efficient and cost-effective option.

When Does Recasting Make Sense?

Understanding what it means to recast a mortgage also involves recognizing the scenarios where it becomes a strategically sound financial move. It’s not a one-size-fits-all solution, but for many homeowners, it can unlock significant financial flexibility and savings.

Lowering Monthly Payments

The most immediate and common benefit of recasting is the reduction in monthly mortgage payments. This can be a lifesaver for homeowners facing financial strain, job loss, or unexpected expenses. Lowering the monthly obligation frees up cash flow, which can be allocated to other financial priorities, such as building an emergency fund, paying down higher-interest debt, or investing. For instance, a family anticipating a period of reduced income might recast their mortgage to make their housing expenses more manageable, providing peace of mind during uncertain times.

Maximizing Home Equity Without Increasing Debt

Recasting allows homeowners to leverage their existing equity for personal financial benefit without resorting to a cash-out refinance. If you’ve paid down a significant portion of your mortgage or have accumulated a substantial lump sum, applying it to your principal through a recast means you’re effectively increasing your ownership stake in your home. This can be particularly appealing if you don’t want to take on additional debt or pay the closing costs associated with a cash-out refinance, yet you still want the financial relief of lower monthly payments. It’s a way to “cash in” on your equity by reducing your liability, rather than borrowing against it.

Avoiding Refinancing Costs and Risks

As discussed, refinancing involves substantial closing costs, which can range from 2% to 6% of the loan amount. These costs can eat into any potential savings, especially for those who don’t plan to stay in their home for a long period. Recasting, on the other hand, typically incurs minimal fees, often just a small administrative charge from the lender. Furthermore, refinancing involves a new loan application, which means a credit check, underwriting, and the risk of denial if market conditions change or your financial situation has deteriorated. Recasting bypasses these hurdles, making it a more secure option for those who have a good payment history and want to avoid the complexities of a full refinance.

Leveraging Windfalls and Savings

Large, unexpected financial windfalls are prime opportunities for recasting. This could include:

- Bonuses or Inheritance: A substantial monetary gift or bonus can be used to significantly reduce the principal.

- Sale of Other Assets: Selling a vehicle, stocks, or other valuable possessions can provide the necessary funds.

- Aggressive Savings: Homeowners who have been diligently saving and have accumulated a large sum can use it to their advantage.

By strategically applying these funds to the mortgage principal and then recasting, homeowners can achieve immediate monthly savings and improve their overall financial standing.

The Process of Recasting: Step-by-Step

Understanding what it means to recast a mortgage is incomplete without knowing how to initiate and navigate the process. While it’s generally straightforward, attention to detail and clear communication with your lender are key.

1. Assess Your Eligibility and Readiness

Before approaching your lender, you need to determine if recasting is a viable option for you.

- Lump-Sum Availability: Do you have a substantial amount of money readily available to make a principal-only payment? The larger the payment, the more significant the impact on your monthly payment.

- Lender Policy: Not all lenders offer mortgage recasting, or they may have specific requirements. It’s crucial to confirm with your current mortgage servicer if they provide this service and what their terms are.

- Loan Type: Recasting is typically available for conventional fixed-rate mortgages. Adjustable-rate mortgages (ARMs) or government-backed loans (FHA, VA) might have different procedures or may not be eligible for standard recasting.

2. Contact Your Mortgage Lender

Once you’ve confirmed your lender offers recasting and you have the funds, the next step is to contact them.

- Inquire Specifically: Ask to speak with a loan modification specialist or customer service representative about “recasting your mortgage.”

- Understand the Requirements: Your lender will outline their specific process, including any required forms, minimum principal payment amounts, and associated fees.

- Confirm Fees: While generally low, ensure you understand the exact cost of the recast.

3. Make the Principal Payment

This is the pivotal step.

- Designate Funds: When you make the large payment, explicitly state that it is a principal-only payment. This is critical to ensure the funds are applied correctly and not to your next regular payment or escrow.

- Verification: Obtain written confirmation from your lender that the payment has been received and applied correctly to your principal balance.

4. Lender Re-amortizes the Loan

After your principal payment has been processed, your lender will recalculate your loan.

- New Amortization Schedule: The lender will create a new amortization schedule based on the reduced principal balance and the remaining term of your original loan, using your original interest rate.

- New Monthly Payment: You will be informed of your new, lower monthly principal and interest payment. This change will take effect with your next payment cycle, or as specified by the lender.

5. Update Your Records

Ensure your personal financial records reflect the new monthly payment amount and the reduced outstanding loan balance. This is important for budgeting and future financial planning.

Potential Downsides and Considerations

While recasting a mortgage offers compelling benefits, it’s essential to consider the potential downsides and nuances to make an informed decision. Understanding what it means to recast a mortgage also involves acknowledging its limitations.

Impact on Equity Buildup Speed

By lowering your monthly payments, you will also slow down the rate at which you build equity through your regular principal and interest payments. While you’ve reduced your principal with a lump sum, your ongoing payments are now smaller, meaning less of each payment goes towards principal compared to your original amortization schedule. If your goal was to pay off your mortgage as quickly as possible, recasting might counteract that objective, even though you’ve reduced your overall debt. This is a trade-off between immediate cash flow relief and long-term equity acceleration.

Inability to Access Cash

Unlike a cash-out refinance, recasting does not provide you with immediate access to cash from your home equity. The lump sum you contribute is permanently applied to reduce your debt. If you need funds for other purposes, such as home improvements, education, or emergencies, recasting alone will not meet that need. In such cases, a cash-out refinance or a home equity loan or line of credit (HELOC) might be more appropriate, despite their potentially higher costs.

Lender Dependence and Requirements

The availability and terms of mortgage recasting are entirely dependent on your lender’s policies. Some lenders may have strict requirements regarding the minimum principal payment, the frequency of recasting allowed, or the types of loans they will recast. If your lender does not offer recasting or has unfavorable terms, you may be forced to consider other options like refinancing, which can be more expensive. It’s always advisable to shop around and understand if other lenders might offer better recasting terms if your current lender is restrictive.

Not a Solution for Interest Rate Reduction

A critical point to reiterate is that recasting does not alter your interest rate. If you are seeking to take advantage of lower market interest rates to reduce your overall interest costs over the life of the loan, recasting will not achieve this. In such scenarios, a refinance that secures a new, lower interest rate would be necessary, even with its associated costs. The decision to recast should be based on a need for lower monthly payments rather than a desire to secure a better interest rate.

In conclusion, understanding what it means to recast a mortgage reveals it as a powerful, yet specific, financial tool. It offers a straightforward path to lower monthly payments by reducing the principal balance, all without the complexities and costs of a full refinance. However, it requires a significant lump sum and does not offer the benefit of a lower interest rate or immediate cash access. By carefully weighing these aspects against your personal financial goals, you can determine if recasting is the optimal strategy for your homeownership journey.