Compounding is a fundamental concept with far-reaching implications across various disciplines, particularly in finance. At its core, compounding refers to the process of earning returns not only on your initial investment but also on the accumulated returns from previous periods. This creates a snowball effect, where your money grows at an accelerating rate over time. Understanding compounding is crucial for anyone looking to build wealth, make informed investment decisions, or grasp the dynamics of long-term financial growth.

The Mechanics of Compounding: Building Wealth Through Reinvestment

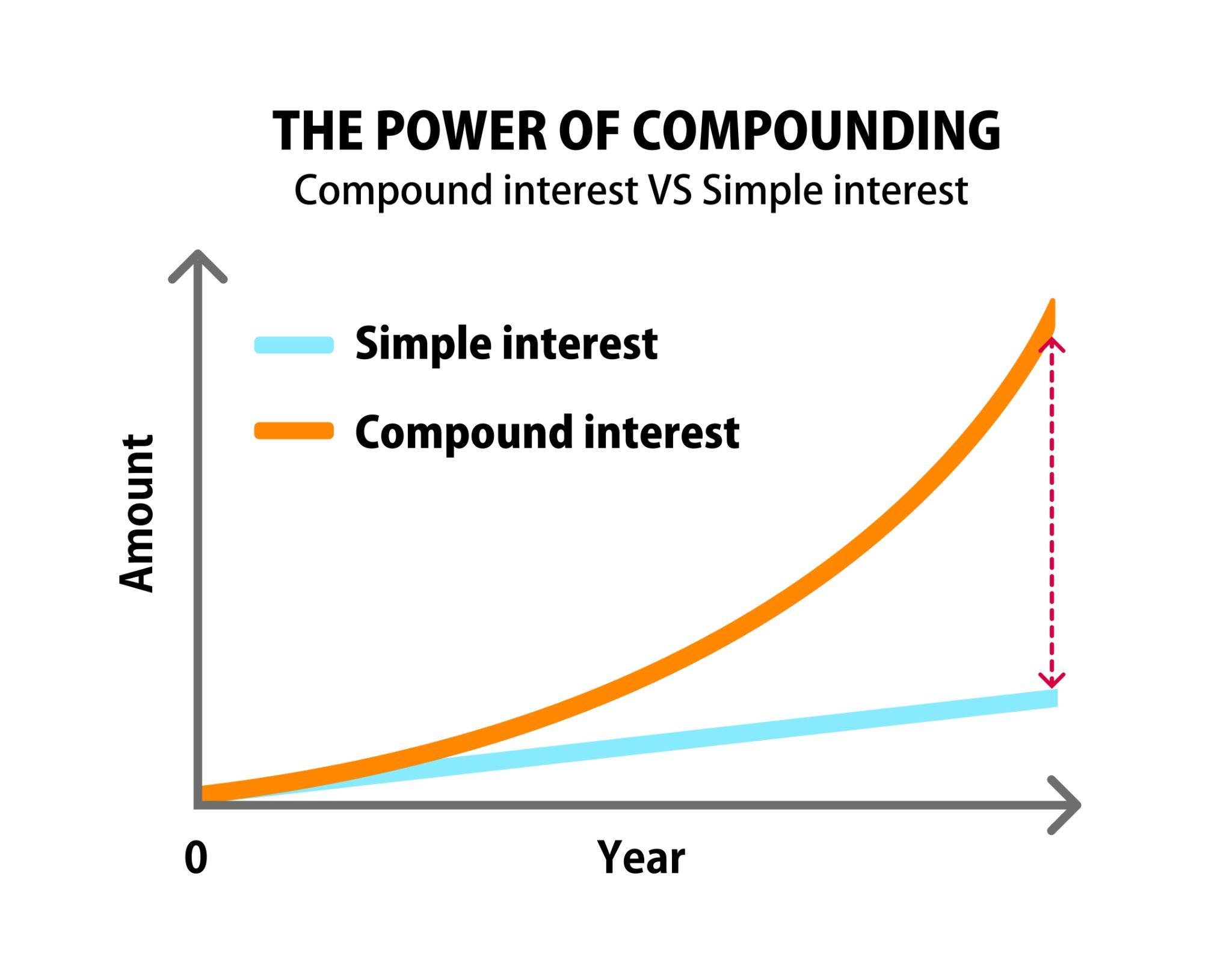

The power of compounding lies in its seemingly simple yet profoundly impactful mechanism: reinvestment. Instead of withdrawing earnings, allowing them to be added back to the principal amount, they then begin to generate their own returns. This continuous cycle of growth is what differentiates compounding from simple interest, where earnings are solely based on the initial principal.

Simple Interest vs. Compound Interest: A Tale of Two Growth Paths

To truly appreciate compounding, it’s essential to contrast it with simple interest. Simple interest is calculated only on the original principal amount over a specific period. For instance, if you invest $1,000 at a 5% simple annual interest rate, you would earn $50 each year ($1,000 * 0.05). After 10 years, your total interest earned would be $500 ($50 * 10), bringing your total to $1,500. While this is a positive return, it’s a linear progression.

Compound interest, on the other hand, works differently. If you invest the same $1,000 at a 5% compound annual interest rate, your first year’s interest would still be $50. However, at the beginning of the second year, your new principal becomes $1,050. Therefore, your interest earned in the second year would be $52.50 ($1,050 * 0.05). This might seem like a small difference initially, but over time, it becomes substantial. After 10 years, with compound interest, your investment would grow to approximately $1,628.89. The difference of $128.89 might seem modest at this stage, but the divergence in growth becomes exponential as the investment horizon extends.

The Frequency of Compounding: Accelerating the Growth Engine

The frequency with which interest is compounded significantly impacts the rate of growth. Compounding can occur annually, semi-annually, quarterly, monthly, or even daily. The more frequent the compounding, the sooner the earned interest is added back to the principal, leading to a more rapid acceleration of returns.

- Annual Compounding: Interest is calculated and added to the principal once a year. This is the slowest form of compounding among the common frequencies.

- Semi-Annual Compounding: Interest is calculated and added to the principal twice a year. This provides a slight boost compared to annual compounding.

- Quarterly Compounding: Interest is calculated and added to the principal four times a year. This offers a more noticeable acceleration in growth.

- Monthly Compounding: Interest is calculated and added to the principal twelve times a year. This is a very common compounding frequency for savings accounts and many investments, offering a significant advantage over less frequent compounding.

- Daily Compounding: Interest is calculated and added to the principal every day. This is the most aggressive form of compounding, maximizing the effect of reinvestment and leading to the fastest growth over time.

While daily compounding yields the highest returns, the difference between monthly and daily compounding becomes less pronounced as the interest rate increases. However, in all scenarios, more frequent compounding leads to higher overall returns.

The “Rule of 72”: A Quick Estimation Tool for Compounding Growth

While the actual calculation of compounding can involve complex formulas, especially with varying interest rates and time periods, the “Rule of 72” provides a remarkably simple yet effective way to estimate how long it will take for an investment to double in value, assuming a fixed rate of return.

Understanding the Rule of 72

The Rule of 72 is an approximation that states:

- Number of Years to Double = 72 / Annual Interest Rate

For example, if an investment offers an annual compound interest rate of 8%, it will take approximately 9 years for the investment to double (72 / 8 = 9). If the interest rate is 6%, it would take approximately 12 years (72 / 6 = 12).

Limitations and Applications of the Rule of 72

It’s important to remember that the Rule of 72 is an estimation tool and works best for interest rates between 6% and 10%. For rates outside this range, the approximation becomes less accurate. However, its simplicity makes it an invaluable tool for quickly grasping the potential of compounding and comparing different investment scenarios. It highlights the power of time and interest rates in wealth accumulation. For instance, a seemingly small difference in interest rates can lead to a significant difference in doubling time, and consequently, in the final value of an investment over the long term.

The Timeless Power of Compounding: A Long-Term Perspective

The true magic of compounding is most evident when viewed through a long-term lens. The longer your money is invested and allowed to compound, the more dramatic the growth becomes. This is why starting to save and invest early in life is often cited as a key financial strategy.

The Impact of Time Horizon: Why Early Investing Matters

Imagine two individuals, Sarah and John, both investing $10,000 annually from the age of 25. Sarah continues investing until she turns 65 (40 years of investing), while John only invests from 35 to 55 (20 years of investing) and then stops. Assuming an average annual return of 7%, Sarah would have amassed significantly more wealth than John, even though they both contributed the same total amount over different periods.

Sarah’s consistent, long-term compounding would allow her initial investments to grow and generate returns on those returns for a much longer duration. John’s shorter investment period means his money has less time to benefit from the snowball effect of compounding. This illustrates why time is arguably the most critical factor in maximizing the benefits of compounding.

Compounding in Action: Beyond Financial Investments

While compounding is most commonly discussed in the context of financial investments like stocks, bonds, and savings accounts, the principle extends to other areas:

- Knowledge and Skills: The more you learn and practice a skill, the more adept you become. Each new piece of knowledge builds upon existing understanding, leading to exponential growth in expertise.

- Habits: Positive habits, when consistently practiced, can compound over time. For example, a daily exercise routine, even if short, can lead to significant improvements in health and fitness over months and years. Conversely, negative habits can also compound, leading to detrimental outcomes.

- Relationships: Nurturing relationships with consistent effort, communication, and support can lead to deeper bonds and stronger connections over time, much like compound interest.

Understanding compounding in its broadest sense reveals its pervasive influence on progress and growth in various aspects of life. It underscores the importance of consistent effort, long-term vision, and the strategic reinvestment of gains, whether financial or otherwise.