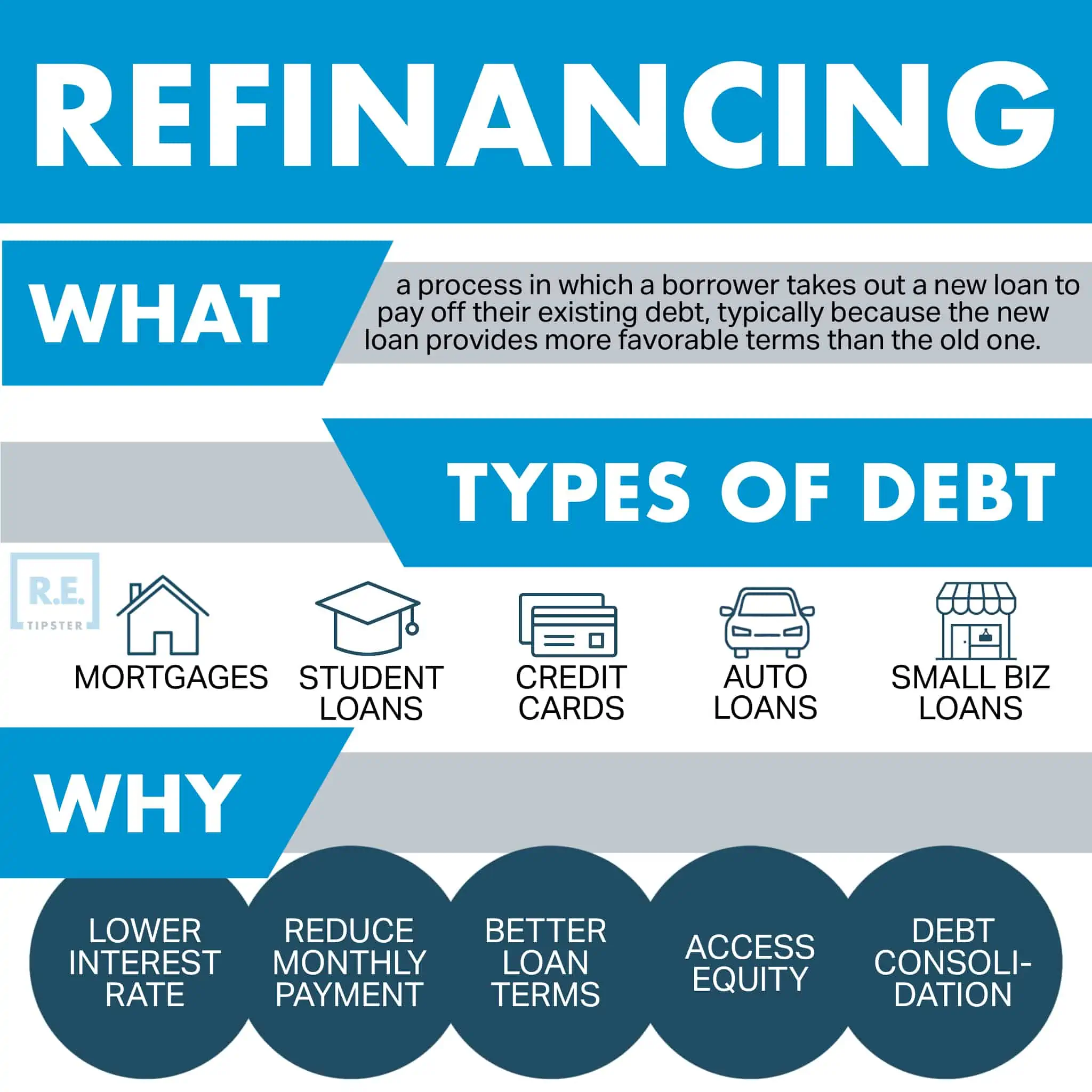

The term “refinancing” is often encountered in financial discussions, but its precise meaning and implications can sometimes be misunderstood. At its core, refinancing refers to the process of replacing an existing debt or loan with a new one, typically on different terms. This new loan is usually obtained from a different lender or through a renegotiation with the original lender. The primary motivations behind refinancing are often to secure more favorable interest rates, reduce monthly payments, shorten the loan term, or access cash.

While the concept of refinancing is broadly applicable to various types of debt, it is most commonly associated with mortgages, auto loans, and personal loans. Understanding the nuances of refinancing is crucial for consumers looking to optimize their financial obligations and improve their overall financial health. This article will delve into the fundamental meaning of refinancing, explore the various reasons why individuals choose to refinance, and examine the key considerations involved in the process.

The Core Mechanics of Refinancing

Refinancing involves obtaining a new loan to pay off an old loan. This might seem like a simple transaction, but it entails a thorough evaluation of existing financial commitments and a comparison of new loan offers. The new loan effectively “replaces” the old one, and the borrower then makes payments on the new loan. This process is distinct from merely making payments on an existing loan.

Replacing Existing Debt with New Terms

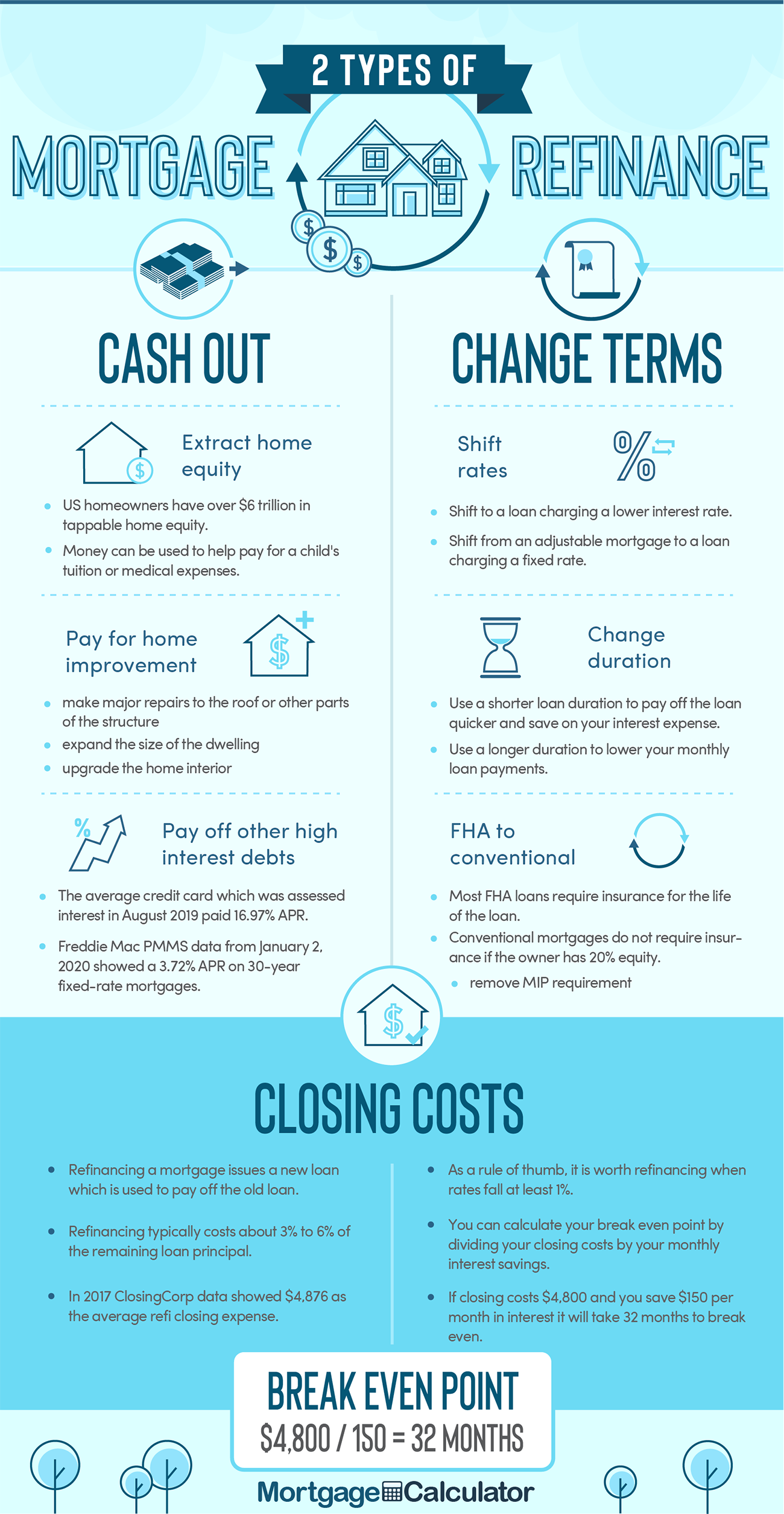

When you refinance, you are essentially creating a new financial agreement. This new agreement will have its own set of terms, including interest rate, loan term (the length of time you have to repay the loan), and potentially fees. The principal amount of the new loan will typically be equal to the outstanding balance of the old loan, plus any closing costs associated with the new loan. However, in some cases, borrowers may choose to “cash out” refinance, meaning the new loan amount exceeds the outstanding balance of the old loan, allowing them to receive the difference in cash.

The Role of Interest Rates

The most significant driver for refinancing is often the change in interest rates. If market interest rates have fallen since the original loan was secured, a borrower may be able to refinance their existing debt at a lower interest rate. This reduction in interest rate directly translates to lower monthly payments and, over the life of the loan, can result in substantial savings in interest paid. Conversely, if interest rates have risen, refinancing might not be financially advantageous.

Loan Term Adjustments

Refinancing also offers the flexibility to adjust the loan term. Borrowers might opt to refinance into a loan with a shorter term to pay off their debt faster and save on interest, albeit with potentially higher monthly payments. Alternatively, they may choose a longer loan term to reduce their monthly payments, which can improve cash flow but will likely result in paying more interest over the extended period. The decision regarding loan term adjustment depends heavily on the borrower’s financial goals and current circumstances.

Why Refinance? Common Motivations and Benefits

The decision to refinance is driven by a variety of financial objectives. Understanding these motivations is key to determining whether refinancing is the right strategy for an individual. The benefits can range from immediate financial relief to long-term wealth building.

Lowering Monthly Payments

One of the most common reasons for refinancing is to reduce the monthly financial burden. By securing a lower interest rate or extending the loan term, borrowers can often lower their regular payments. This can be particularly beneficial for individuals experiencing temporary financial strain or those looking to free up cash for other expenses, investments, or savings. For example, a homeowner with a mortgage might refinance to reduce their monthly housing payment, easing their budget.

Reducing Total Interest Paid Over Time

While lowering monthly payments is attractive, a more significant long-term benefit of refinancing can be the reduction in the total amount of interest paid over the life of the loan. If a borrower can secure a substantially lower interest rate, even if they maintain the original loan term, the cumulative savings in interest can be considerable. This is especially true for long-term loans like mortgages. A few percentage points difference in interest rate can amount to tens of thousands of dollars saved over 15 or 30 years.

Accessing Equity Through Cash-Out Refinancing

For homeowners, cash-out refinancing offers a way to tap into the equity they have built in their property. Equity is the difference between the home’s market value and the amount owed on the mortgage. In a cash-out refinance, the borrower takes out a new mortgage for a larger amount than their existing mortgage balance. The difference is then disbursed to the borrower in cash. This cash can be used for various purposes, such as home renovations, debt consolidation, education expenses, or investments. It’s important to note that this process increases the total debt and requires careful consideration of the ability to repay the larger loan.

Consolidating Debt

Refinancing can also be a powerful tool for debt consolidation. Individuals with multiple high-interest debts, such as credit card balances or personal loans, may consider refinancing into a single loan with a lower interest rate. This simplifies payments, reduces the overall interest paid, and can make managing finances more straightforward. For example, consolidating several credit card debts into a personal loan or a home equity line of credit (HELOC) can result in significant interest savings.

The Refinancing Process: Key Steps and Considerations

Embarking on a refinancing journey requires careful planning and execution. While the idea of better terms is appealing, the process involves more than just finding a new lender. Understanding the steps involved and the potential costs will help ensure a successful outcome.

Assessing Eligibility and When to Refinance

The first step in refinancing is to assess your eligibility. Lenders will review your credit score, income, debt-to-income ratio, and the value of the asset being refinanced (e.g., your home or car). A good credit score is paramount, as it typically qualifies you for the best interest rates. It’s also important to consider the timing. Generally, it makes sense to refinance when interest rates are significantly lower than your current rate, or when your financial situation has improved in a way that makes you a more attractive borrower.

Comparing Offers and Understanding Fees

Once you’ve determined that refinancing is a viable option, the next crucial step is to shop around and compare offers from various lenders. Different lenders may offer different interest rates, fees, and loan terms. It is essential to look beyond just the advertised interest rate and consider all associated costs, often referred to as “closing costs.” These fees can include appraisal fees, origination fees, title insurance, recording fees, and more. These costs can sometimes offset the savings from a lower interest rate, especially for shorter-term loans.

The Application and Underwriting Process

Applying for refinancing involves submitting a comprehensive application, similar to when you initially took out the loan. You’ll need to provide financial documentation such as pay stubs, tax returns, and bank statements. The lender will then go through an underwriting process, which involves verifying all the information you’ve provided and assessing the risk involved in lending to you. This can include a credit check, income verification, and, for mortgages, a property appraisal to determine its current market value.

Closing the New Loan and Paying Off the Old One

Once your refinancing application is approved, you will proceed to closing. At closing, you will sign all the necessary paperwork for the new loan. The funds from the new loan will then be used to pay off your existing loan in full. This is the point at which the refinancing is complete, and you will begin making payments on your new loan according to its terms. It’s vital to confirm that the old loan has indeed been paid off to avoid any confusion or duplicate payments.

In conclusion, refinancing is a powerful financial tool that allows individuals to restructure existing debt, often leading to significant savings and improved financial flexibility. By understanding the mechanics of refinancing, its various benefits, and the intricacies of the process, consumers can make informed decisions that align with their financial goals and contribute to long-term financial well-being.