Debentures represent a fundamental component of corporate finance, offering a crucial mechanism for companies to raise capital without immediately diluting shareholder equity. Unlike stocks, which represent ownership, debentures are a form of debt. They are essentially long-term loans issued by a company to investors, backed by the general creditworthiness and reputation of the issuing entity rather than specific assets. This distinction is paramount: while secured bonds are collateralized by tangible assets, debentures rely on the promise of the issuer to repay the principal amount on a specified maturity date and to make regular interest payments.

The concept of debentures is deeply rooted in the evolution of financial markets. As businesses grew in scale and complexity, the need for substantial capital investment became more pronounced. Initially, companies relied on equity financing or bank loans. However, the limitations of these methods – equity dilution for the former and potential rigid repayment terms for the latter – paved the way for more flexible and scalable debt instruments. Debentures emerged as a sophisticated solution, allowing companies to access a broader pool of investors and manage their capital structure more strategically. Their versatility has made them a cornerstone of financial engineering, supporting everything from infrastructure projects to technological innovation.

Understanding debentures is not merely an academic exercise; it is essential for investors seeking diversified income streams and for corporate treasurers managing their financial obligations. The nuances of their structure, the factors influencing their valuation, and the diverse types available all contribute to a comprehensive understanding of this vital financial instrument. This exploration will delve into the core characteristics of debentures, their advantages and disadvantages for both issuers and investors, and the various forms they can take, providing a thorough overview of this significant debt instrument.

The Fundamental Nature of Debentures

At their core, debentures are unsecured debt securities. This “unsecured” aspect is the defining characteristic that differentiates them from other types of bonds. While the absence of specific collateral might seem like a disadvantage, it is crucial to understand the underlying principles that make debentures a viable and often attractive investment. The issuer’s creditworthiness becomes the primary security for the debenture holder.

Definition and Key Characteristics

A debenture is a debt instrument issued by a corporation, municipality, or government entity, promising to repay a specific amount of money (the principal or face value) at a future date (maturity date) and to pay periodic interest at a fixed or floating rate. Unlike mortgage bonds or collateral trust bonds, debentures are not backed by any specific physical assets or collateral. Instead, the repayment of debentures relies entirely on the issuer’s general creditworthiness, its reputation, and its ability to generate future earnings. This means that debenture holders are essentially general creditors of the issuing entity.

The key characteristics of debentures include:

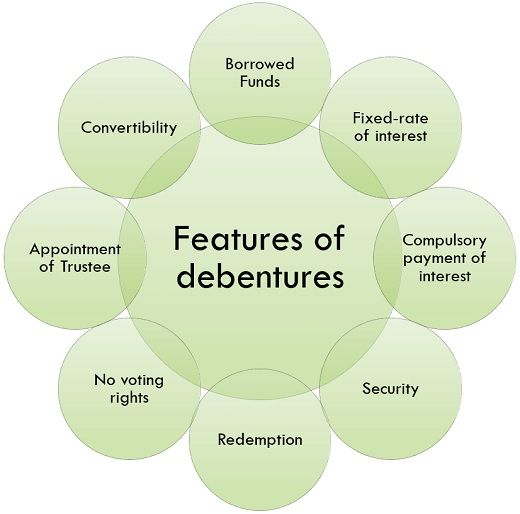

- Unsecured Nature: This is the most defining feature. They are not backed by specific assets.

- Promise to Pay: The issuer makes a contractual promise to repay the principal and interest.

- Maturity Date: Debentures have a predetermined date by which the principal must be repaid.

- Interest Payments: Regular interest payments (coupons) are typically made, though zero-coupon debentures also exist.

- Creditworthiness as Security: The financial health and reputation of the issuer are the primary forms of security.

Distinction from Other Debt Instruments

It is vital to distinguish debentures from other common debt instruments, such as secured bonds and commercial paper.

- Secured Bonds: These bonds are backed by specific assets of the issuer. For example, a mortgage bond is secured by real estate, and a collateral trust bond is secured by other securities held in trust. In the event of default, holders of secured bonds have a prior claim on the specified collateral. Debenture holders, being unsecured creditors, stand behind secured creditors in the event of liquidation.

- Government Bonds: While government bonds can be unsecured, they are generally considered to have extremely low risk due to the taxing power and sovereign status of the issuer. Corporate debentures, by contrast, carry a higher degree of credit risk tied to the specific company’s performance.

- Commercial Paper: This is a short-term, unsecured promissory note typically issued by corporations to finance short-term liabilities. Debentures are generally long-term instruments.

The unsecured nature of debentures means that investors must carefully assess the financial stability and credit rating of the issuing company. A higher credit rating signifies a lower risk of default, making the debenture more attractive.

Types and Variations of Debentures

Debentures are not a monolithic entity. They come in various forms, each with specific features that cater to different investor preferences and issuer needs. These variations primarily revolve around how interest is paid, whether they are convertible into other securities, and the priority of their claims.

Callable vs. Non-Callable Debentures

The ability of the issuer to redeem debentures before their maturity date is a significant factor.

- Callable Debentures: These debentures give the issuer the right, but not the obligation, to repurchase the debentures from the holders at a predetermined price before the maturity date. Issuers typically call debentures when interest rates fall significantly, allowing them to refinance their debt at a lower cost. For investors, callable debentures carry reinvestment risk, as they may have to reinvest the principal at a lower interest rate if the debenture is called. To compensate for this risk, callable debentures often offer a slightly higher coupon rate than comparable non-callable debentures.

- Non-Callable Debentures: As the name suggests, these debentures cannot be redeemed by the issuer before their maturity date. This provides greater certainty for investors regarding their income stream and maturity date. They are generally preferred by investors who prioritize predictable cash flows and longer-term investment horizons.

Convertible Debentures

Convertible debentures offer investors a unique hybrid feature: the right to convert the debenture into a predetermined number of common shares of the issuing company.

- Mechanism of Conversion: The conversion ratio is set at the time of issuance. If the company’s stock price rises significantly, investors may choose to convert their debentures into shares, potentially realizing a capital gain. This feature makes convertible debentures attractive to investors who want the income stability of a bond combined with the potential for capital appreciation from equity.

- Advantages for Issuers: Companies may issue convertible debentures to raise capital at a lower interest rate than they would on straight debt, as the conversion feature adds value for investors. Furthermore, if the debentures are converted, the company effectively reduces its debt burden without an immediate cash outflow for repayment.

Fixed-Rate vs. Floating-Rate Debentures

The manner in which interest is determined is another key differentiator.

- Fixed-Rate Debentures: These debentures pay a constant rate of interest throughout their life. This provides investors with predictable income and makes it easier to budget and manage cash flows. However, fixed-rate debentures are more sensitive to interest rate fluctuations; if market interest rates rise, the market value of existing fixed-rate debentures with lower coupon rates will fall.

- Floating-Rate Debentures (FRNs): These debentures have an interest rate that is periodically adjusted, typically based on a benchmark rate such as LIBOR (or its successor, SOFR) or a prime rate, plus a fixed spread. Floating-rate debentures offer protection against rising interest rates for investors, as their coupon payments will increase with market rates. For issuers, they can be beneficial in a rising interest rate environment, as their interest expense will also rise.

Advantages and Disadvantages of Debentures

The issuance and investment in debentures come with a distinct set of benefits and drawbacks for both the corporations raising capital and the investors providing it. A thorough understanding of these trade-offs is crucial for informed financial decision-making.

For Issuing Companies

Advantages:

- No Dilution of Ownership: Unlike issuing equity, issuing debentures does not dilute the ownership stake of existing shareholders. This is particularly attractive for established companies that wish to maintain control and maximize earnings per share.

- Tax Deductibility of Interest: The interest paid on debentures is typically a tax-deductible expense for the issuing company. This reduces the company’s overall tax liability, making debt financing more cost-effective than equity financing.

- Financial Leverage: Issuing debt can increase financial leverage, which can boost returns on equity if the company’s investments generate returns higher than the interest rate on the debentures. This can lead to higher profits for shareholders.

- Flexibility in Capital Structure: Debentures provide companies with a flexible way to raise substantial amounts of capital for various purposes, such as expansion, acquisitions, or research and development, without resorting to selling ownership stakes.

Disadvantages:

- Fixed Obligation: The obligation to pay interest and repay principal is fixed and mandatory, regardless of the company’s profitability. In times of financial distress, these fixed payments can strain cash flows and increase the risk of bankruptcy.

- Increased Financial Risk: A higher debt-to-equity ratio increases a company’s financial risk. If the company fails to meet its debt obligations, it could lead to default, bankruptcy, and severe damage to its reputation.

- Restrictive Covenants: Debentures often come with restrictive covenants, which are conditions imposed on the issuer to protect the debenture holders. These covenants can limit the company’s ability to take on more debt, pay dividends, sell assets, or engage in certain business activities, thus restricting management’s operational flexibility.

- Credit Rating Impact: Issuing a significant amount of debt can negatively impact a company’s credit rating, making future borrowing more expensive.

For Investors

Advantages:

- Regular Income Stream: Debentures typically offer regular interest payments, providing investors with a predictable and stable source of income. This is particularly attractive for retirees or those seeking income-generating investments.

- Lower Risk than Equity: Generally, debentures are considered less risky than equity investments. In the event of liquidation, debenture holders have a higher priority claim on the company’s assets than shareholders.

- Potential for Capital Appreciation (Convertible Debentures): Convertible debentures offer investors the possibility of capital gains if the issuing company’s stock price increases significantly.

- Diversification: Debentures can be a valuable tool for portfolio diversification, as their performance may not always be directly correlated with the stock market.

Disadvantages:

- Lower Potential Returns: Compared to equity investments, debentures generally offer lower potential returns. The upside is capped by the interest payments and the principal repayment.

- Credit Risk: The primary risk for debenture holders is the credit risk of the issuer. If the issuer defaults, investors may lose part or all of their investment. This risk is amplified for unsecured debentures.

- Interest Rate Risk: For fixed-rate debentures, rising market interest rates can lead to a decrease in the market value of the debentures. If an investor needs to sell before maturity, they may incur a capital loss.

- Inflation Risk: Fixed-rate interest payments can lose purchasing power over time if inflation rates are high, eroding the real return on the investment.

- Liquidity Risk: While some debentures are actively traded, others may have limited liquidity, making it difficult for investors to sell them quickly at a fair price before maturity.

Debentures in the Modern Financial Landscape

In today’s dynamic financial environment, debentures continue to play a significant role, adapting to new economic conditions and evolving investor demands. The proliferation of sophisticated financial instruments has not rendered debentures obsolete; rather, it has led to their refinement and integration within broader investment strategies. Their continued relevance is a testament to their fundamental utility in bridging the gap between capital needs and investment opportunities.

Role in Corporate Finance and Investment Strategies

Debentures remain a primary tool for corporations to manage their capital structure. Companies utilize them for a variety of strategic purposes:

- Funding Growth and Expansion: Large-scale projects, such as building new facilities, acquiring other companies, or investing in research and development, often require substantial capital that debentures can help provide.

- Refinancing Existing Debt: As mentioned, companies may issue new debentures at lower interest rates to replace older, higher-cost debt, thereby reducing their interest expenses.

- Share Buybacks: Sometimes, companies issue debentures to fund share buyback programs, aiming to increase earnings per share and return capital to shareholders without diluting ownership.

For investors, debentures are integral to building diversified portfolios. They offer a balance between risk and return, providing a more stable income stream than equities while offering potentially higher yields than government bonds. The existence of various types of debentures allows investors to tailor their fixed-income holdings to specific risk appetites and market outlooks. For example, an investor concerned about rising interest rates might favor floating-rate debentures, while one seeking long-term stable income might opt for non-callable fixed-rate debentures.

Regulatory and Market Considerations

The issuance and trading of debentures are subject to various regulatory frameworks designed to protect investors and ensure market integrity. Securities commissions and financial regulatory bodies oversee the disclosure requirements for issuers, ensuring that investors receive adequate information to make informed decisions. This includes detailed financial statements, risk factors, and terms of the debenture offering.

Market conditions significantly influence the issuance and valuation of debentures. Factors such as prevailing interest rates, the overall economic outlook, inflation expectations, and the creditworthiness of the issuing sector all play a crucial role. During periods of economic uncertainty or rising interest rates, the demand for corporate debentures might decrease, leading to higher yields (lower prices) for new issues. Conversely, in stable economic environments with falling interest rates, debenture issuance can be robust, and their market prices tend to appreciate.

Furthermore, credit rating agencies (e.g., Standard & Poor’s, Moody’s, Fitch) play a vital role in assessing and communicating the creditworthiness of debenture issuers. Their ratings provide investors with an independent evaluation of the likelihood of the issuer defaulting on its obligations, significantly influencing the interest rates at which debentures can be issued and traded. A higher credit rating generally translates to a lower coupon rate and a more attractive investment from a risk perspective.

In conclusion, debentures are versatile and indispensable financial instruments. They facilitate corporate growth by providing access to capital, and they offer investors a crucial avenue for income generation and portfolio diversification. While they carry inherent risks, particularly credit and interest rate risk, their fundamental role in the capital markets remains undeniable, underpinned by ongoing regulatory oversight and market dynamics.