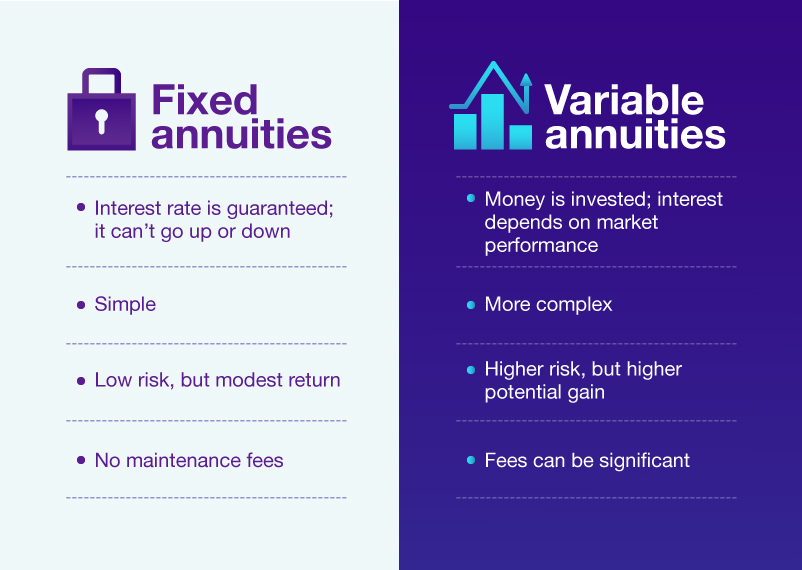

Fixed annuities represent a cornerstone of conservative financial planning, offering a guaranteed return on investment coupled with a secure income stream. For individuals seeking stability and predictability in their retirement savings, fixed annuities present an attractive proposition. Unlike market-linked investments that can fluctuate with economic cycles, fixed annuities provide a predetermined interest rate, shielding your principal from market volatility. This inherent safety makes them a popular choice for risk-averse investors, particularly those nearing or in retirement.

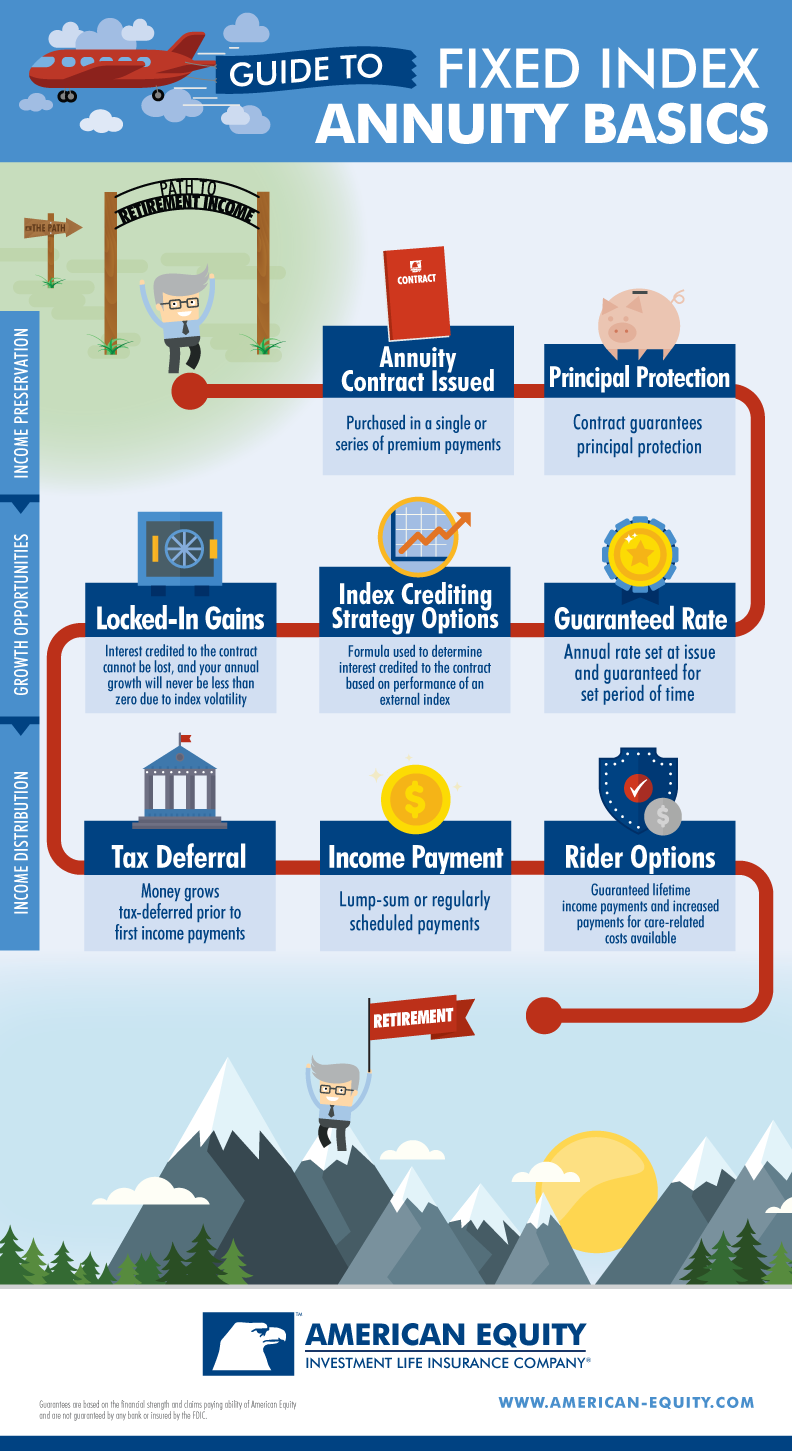

The fundamental structure of a fixed annuity involves an individual purchasing a contract from an insurance company. In exchange for an upfront lump sum payment or a series of premium payments, the insurance company promises to pay the annuity holder a specified rate of interest for a set period. This period can range from a few years to the annuitant’s entire lifetime. At the end of this accumulation phase, the contract owner can elect to receive the accumulated value as a lump sum, or more commonly, as a stream of guaranteed income payments. This income stream can be structured in various ways to suit individual needs, offering a reliable source of funds for living expenses, healthcare costs, or other financial commitments during retirement.

Understanding the Mechanics of Fixed Annuities

At their core, fixed annuities operate on a simple principle of guaranteed growth and predictable payouts. The insurance company invests the premiums it receives into conservative, fixed-income instruments such as government bonds and corporate debt. The returns generated from these investments are then used to credit interest to the annuity holder’s account at the guaranteed rate. This mechanism ensures that regardless of market performance, the principal amount invested and the earned interest are protected.

The Accumulation Phase

The initial phase of a fixed annuity is known as the accumulation period. During this time, the annuity owner deposits funds into the contract. These funds then begin to earn interest at the rate specified in the annuity contract. This interest is typically tax-deferred, meaning that taxes are not owed on the earnings until the money is withdrawn from the annuity. This tax deferral can significantly enhance the long-term growth potential of the investment, allowing earnings to compound more effectively over time.

Interest Rate Guarantees

A defining characteristic of fixed annuities is the guaranteed interest rate. This rate is established at the inception of the contract and remains fixed for a specified term, often referred to as the “guarantee period.” This guarantee provides unparalleled certainty regarding the growth of the annuity’s value. For example, if a fixed annuity offers a 3% guaranteed interest rate for five years, the annuity owner can be confident that their investment will grow by exactly 3% each year for that duration, irrespective of economic conditions or market fluctuations.

Payout Options

Once the accumulation phase concludes, the annuity owner can choose how to receive their funds. The most common and advantageous option for retirement income is annuitization, which converts the accumulated value into a stream of regular payments. There are several ways to structure these payouts to meet diverse needs:

Life Income Option

This option provides guaranteed payments for the remainder of the annuitant’s life. This is particularly valuable for individuals concerned about outliving their savings. The payments are calculated based on the accumulated value, the annuitant’s age and life expectancy, and the prevailing interest rates at the time of annuitization.

Period Certain Option

With this option, payments are guaranteed for a specific number of years, regardless of whether the annuitant is still living. If the annuitant passes away before the end of the period certain, the remaining payments are typically distributed to a designated beneficiary.

Life Income with Period Certain

This hybrid option combines elements of both life income and period certain. Payments are guaranteed for the annuitant’s lifetime, but also for a minimum number of years. This ensures a baseline income for a set duration, with the added benefit of lifetime coverage.

Joint and Survivor Option

This option provides income for two individuals, typically a married couple. Payments continue as long as at least one of the annuitants is alive, offering comprehensive financial security for couples planning for their retirement together.

Types of Fixed Annuities

While the core concept of a fixed annuity remains consistent, variations exist to cater to different financial strategies and objectives. These variations primarily differ in how premiums are paid and when income payments begin.

Single Premium Immediate Annuity (SPIA)

A Single Premium Immediate Annuity (SPIA) is characterized by a single, upfront payment made by the annuitant. In return for this lump sum, the insurance company immediately begins to issue income payments. This makes SPIAs ideal for individuals who have a substantial sum of money readily available and wish to start receiving a guaranteed income stream without delay. The income payments are calculated based on the lump sum invested, the annuitant’s age, and current interest rates.

Single Premium Deferred Annuity (SPDA)

In contrast to SPIAs, Single Premium Deferred Annuities (SPDAs) involve a single lump sum payment, but the income payments are deferred to a future date chosen by the annuitant. This allows the invested funds to grow tax-deferred for a period, potentially accumulating a larger sum before income payments commence. SPDAs offer flexibility in terms of when retirement income begins, allowing individuals to align payout with their specific retirement timeline.

Flexible Premium Deferred Annuity (FPDA)

Flexible Premium Deferred Annuities (FPDAs) allow the annuitant to make multiple premium payments over time. This flexibility is beneficial for individuals who may not have a large lump sum available at once but prefer to contribute gradually to their retirement savings. Like SPDAs, FPDAs also feature tax-deferred growth and deferred income payments, providing a systematic approach to building retirement wealth.

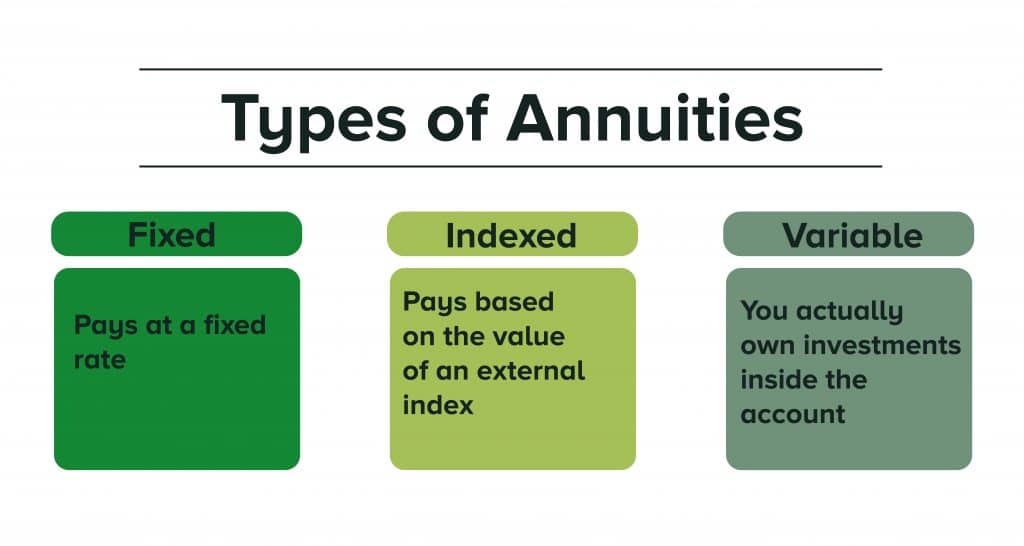

Fixed Index Annuities (FIAs)

While not strictly a “fixed” annuity in the traditional sense, Fixed Index Annuities (FIAs) warrant mention due to their popularity and the inclusion of a fixed component. FIAs offer principal protection like fixed annuities, but their growth potential is linked to the performance of a market index, such as the S&P 500. However, they do not directly invest in the market, mitigating downside risk. They typically offer a floor (often 0%) guaranteeing no loss of principal, while offering participation in market gains up to a certain cap or through a participation rate. This provides a middle ground between the absolute safety of a fixed annuity and the potential higher returns (and risks) of direct market investment.

Advantages and Disadvantages of Fixed Annuities

Like any financial product, fixed annuities come with a specific set of benefits and drawbacks that potential investors must carefully consider. Understanding these nuances is crucial for making an informed decision that aligns with individual financial goals and risk tolerance.

Advantages

The primary allure of fixed annuities lies in their inherent safety and predictability.

-

Principal Protection: The most significant advantage is the guarantee of principal. Regardless of market performance, the initial investment in a fixed annuity is protected by the issuing insurance company. This eliminates the risk of losing money due to market downturns, a primary concern for many conservative investors.

-

Guaranteed Rate of Return: The fixed interest rate ensures a predictable and stable growth of your investment. This allows for clear financial planning and a reliable estimation of future wealth accumulation.

-

Tax-Deferred Growth: Earnings within a fixed annuity grow on a tax-deferred basis. This means you don’t pay taxes on the interest earned until you withdraw the funds, allowing for greater compounding of returns over time.

-

Guaranteed Income Stream: The ability to annuitize a fixed annuity provides a reliable and often lifelong income stream. This can be a crucial component of a secure retirement, covering essential living expenses and providing peace of mind.

-

Simplicity and Ease of Understanding: Compared to more complex investment products, fixed annuities are relatively straightforward to understand, making them accessible to a broad range of investors.

Disadvantages

Despite their advantages, fixed annuities also have certain limitations.

-

Lower Potential Returns: The guarantee of principal and a fixed rate of return typically means that fixed annuities offer lower growth potential compared to market-linked investments like stocks or variable annuities. In periods of high inflation or robust market performance, the fixed return may lag behind.

-

Inflation Risk: While the principal is protected, the purchasing power of a fixed income stream can be eroded by inflation over time. If the rate of inflation exceeds the annuity’s interest rate, the real value of your savings and future income payments will decrease.

-

Liquidity Concerns: Annuities are long-term investments, and accessing funds before the maturity date or annuitization often incurs surrender charges. These charges can be substantial, making annuities illiquid for those who might need immediate access to their capital.

-

Interest Rate Risk (for payouts): While the initial interest rate is fixed for a period, if interest rates rise significantly after the guarantee period, future contract renewals or new annuities might offer higher rates, potentially leaving existing annuitants with a lower return than available in the market.

-

Insurance Company Solvency: The guarantees provided by a fixed annuity are dependent on the financial strength and solvency of the issuing insurance company. While rare, if an insurance company fails, the annuity holder could potentially lose some or all of their investment. It is therefore advisable to choose annuities from highly rated insurance companies.

Who Should Consider a Fixed Annuity?

Fixed annuities are best suited for a specific demographic of investors who prioritize security and predictable income above all else.

Individuals who are nearing retirement or are already retired and are looking for a conservative way to preserve their capital and generate a reliable income stream are prime candidates. Those who are risk-averse and prefer to avoid market volatility will find the principal protection and guaranteed returns of fixed annuities highly appealing. Furthermore, individuals seeking to supplement other retirement income sources, such as Social Security or pensions, with a guaranteed payment can benefit from the predictability offered by fixed annuities.

For those who have already maximized contributions to other tax-advantaged retirement accounts like 401(k)s and IRAs, a fixed annuity can offer an additional avenue for tax-deferred growth. However, it’s crucial for potential buyers to conduct thorough research, understand the contract terms, including fees and surrender charges, and consider consulting with a qualified financial advisor to ensure a fixed annuity aligns with their overall financial plan and long-term objectives.