Direct deposit, a fundamental pillar of modern financial transactions, represents the electronic transfer of money from one account to another. It has revolutionized how individuals and businesses receive and disburse funds, moving away from the cumbersome and often inefficient methods of paper checks. At its core, direct deposit is about speed, security, and convenience, fundamentally altering the landscape of personal finance and business operations. This article will delve into the intricacies of direct deposit, exploring its mechanisms, benefits, and the underlying technology that makes it a ubiquitous and indispensable financial tool.

The Mechanics of Direct Deposit: How Your Money Moves Electronically

Direct deposit is not a single, monolithic process but rather a sophisticated orchestration of systems designed to facilitate the secure and rapid movement of funds. Understanding these underlying mechanisms is key to appreciating the efficiency and reliability of this financial service.

Initiation: The Trigger for Electronic Funds Transfer

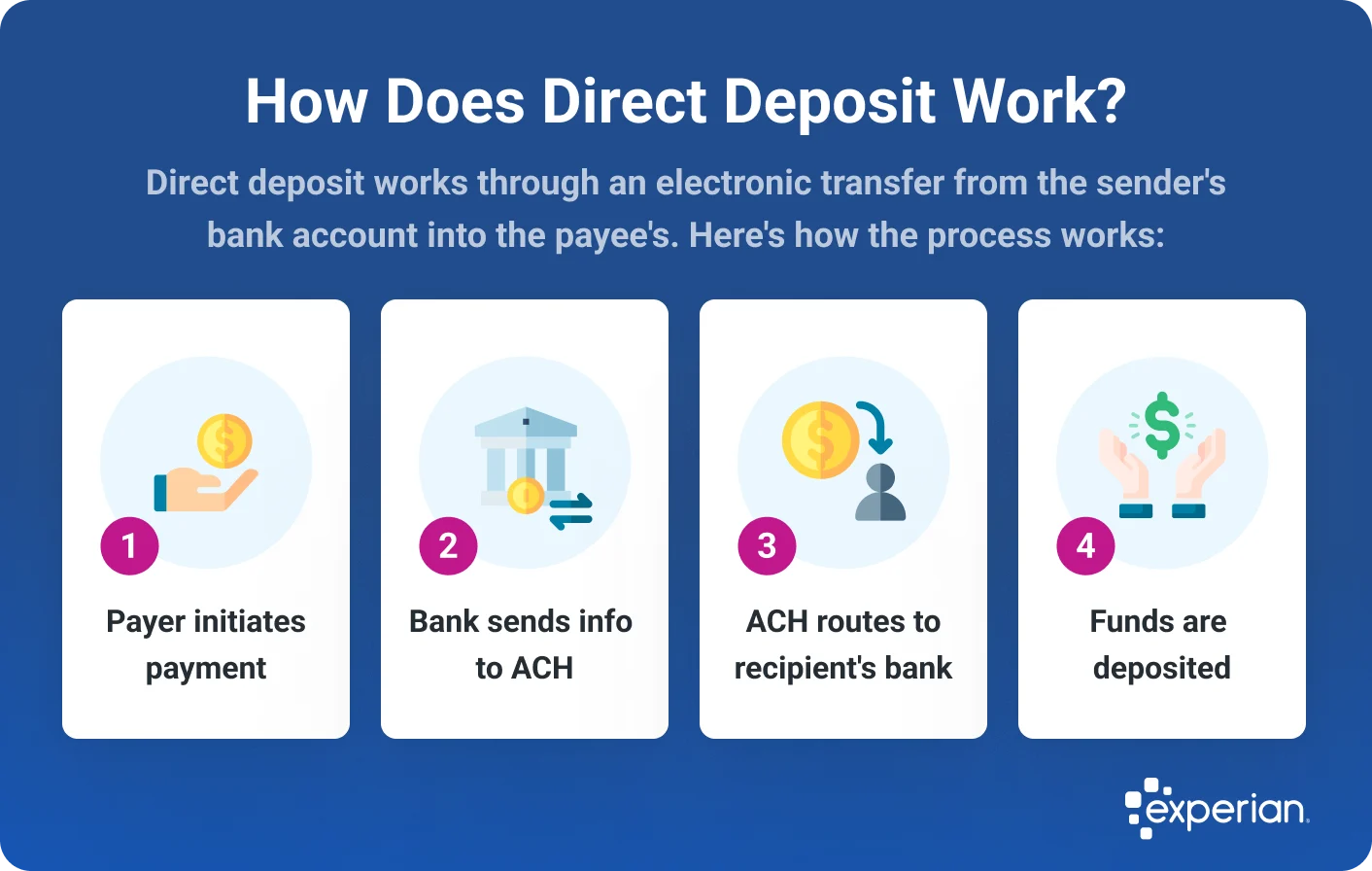

The journey of a direct deposit begins with an authorization. For payroll, this typically involves an employee providing their bank account and routing numbers to their employer. This authorization grants the employer permission to deposit wages directly into the specified account. For other types of deposits, such as government benefits or tax refunds, the initiating agency will have the necessary account information to execute the transfer.

- Payroll Authorization: Employees are usually required to fill out a form that captures their bank name, account number, and the financial institution’s routing number. This form serves as the official authorization for the employer to initiate electronic deposits. Some employers also offer direct deposit enrollment through online portals or HR software, streamlining the process further.

- Government and Other Initiating Bodies: Agencies like the Social Security Administration, the IRS, or companies issuing refunds will have established procedures for collecting and verifying recipient bank details. These processes are designed with security and accuracy in mind to prevent erroneous or fraudulent transactions.

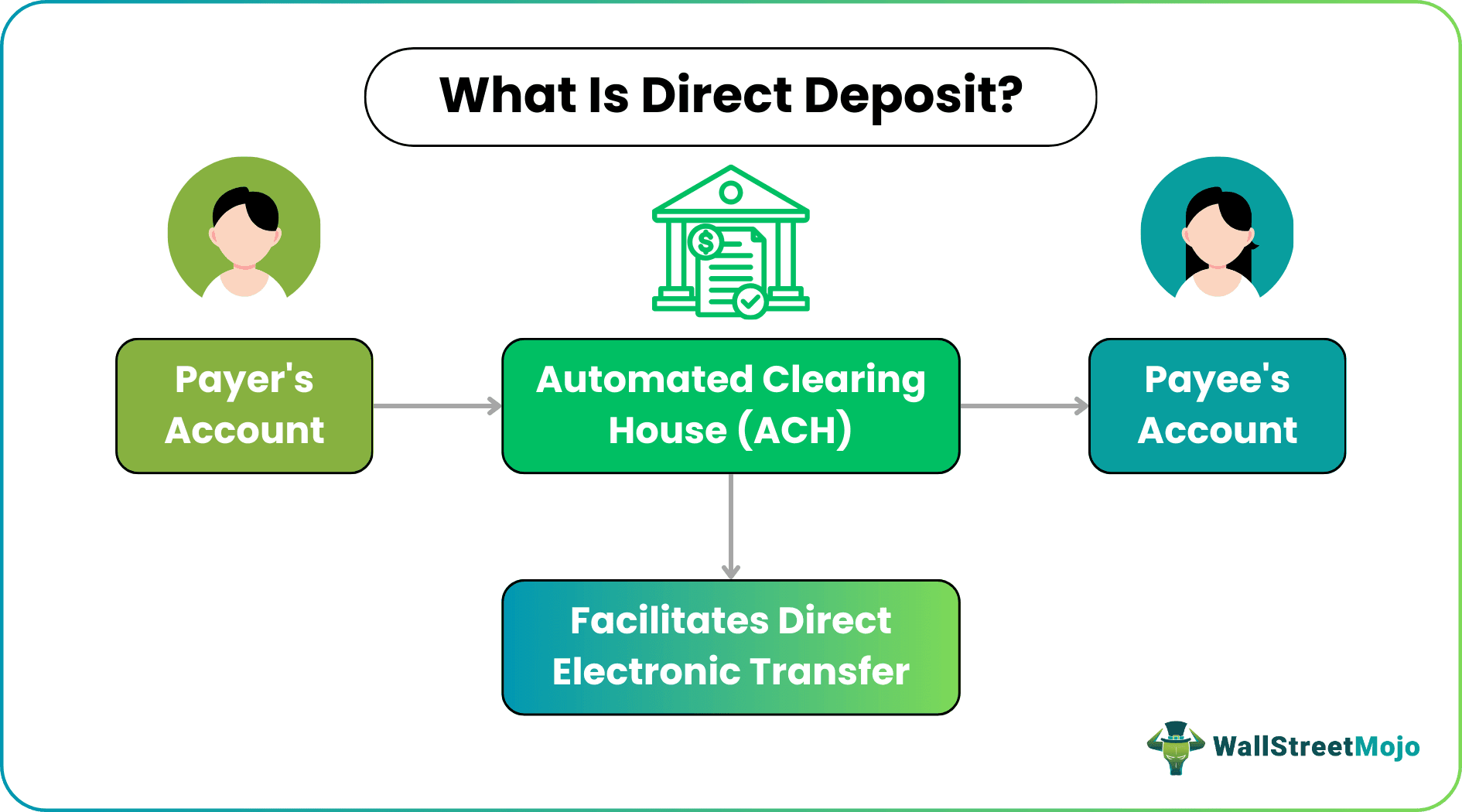

The Role of the Automated Clearing House (ACH) Network

The backbone of direct deposit in the United States is the Automated Clearing House (ACH) network. Operated by Nacha (formerly the National Automated Clearing House Association), the ACH network is a batch processing system that facilitates electronic payments and money transfers between financial institutions. It’s a highly secure and efficient infrastructure that underpins a vast majority of electronic transactions, including direct deposit.

- Batch Processing Explained: Unlike real-time gross settlement (RTGS) systems, which process transactions individually, the ACH network operates on a batch basis. This means that transactions are collected and processed in groups at specific times throughout the day. This batch processing model allows for economies of scale, making it a cost-effective solution for high-volume transactions like payroll.

- Key Players in the ACH Network: The ACH network involves several key entities:

- Originating Financial Institutions (OD FIs): These are the banks or credit unions where the payer (e.g., employer, government agency) holds their account. They initiate the ACH transaction by sending the payment instructions to an ACH operator.

- ACH Operators: These are the entities that facilitate the clearing and settlement of ACH transactions. In the U.S., the two primary ACH operators are the Federal Reserve and The Clearing House. They receive payment files from ODFIs and distribute them to the appropriate Receiving Financial Institutions.

- Receiving Financial Institutions (RDFIs): These are the banks or credit unions where the payee (e.g., employee, recipient of benefits) holds their account. They receive the ACH payment files and credit the designated accounts.

- Nacha: As the governing body, Nacha sets the rules and standards for the ACH network, ensuring the security, reliability, and integrity of all ACH transactions.

Settlement and Crediting: Funds Arrive in Your Account

Once the ACH operator has processed the transaction, the receiving financial institution is responsible for crediting the payee’s account. This process is typically very swift, often occurring within the same business day or by the next business day, depending on the transaction cut-off times.

- Cut-off Times: Financial institutions and ACH operators have specific cut-off times for processing transactions on any given business day. Transactions initiated after a cut-off time will generally be processed on the next business day. This is a crucial factor in understanding when funds will become available.

- Funds Availability: The availability of funds from a direct deposit can vary slightly depending on the policies of the receiving financial institution. While many institutions make funds available on the same day they are received, some may have a brief holding period for certain types of deposits. However, direct deposits are generally made available much faster than funds from a deposited paper check.

The Multifaceted Benefits of Direct Deposit

The widespread adoption of direct deposit is a testament to its significant advantages for both individuals and organizations. These benefits range from enhanced financial security and convenience to increased operational efficiency and reduced costs.

For Individuals: Speed, Security, and Control

Direct deposit fundamentally improves the personal financial experience by offering a secure, reliable, and timely method for receiving money.

- Unparalleled Convenience: The most immediate benefit is the elimination of the need to physically deposit a check. Funds are automatically credited to the account, freeing up individuals’ time and eliminating trips to the bank or ATM. This convenience is particularly valuable for those with busy schedules or limited mobility.

- Enhanced Security: Paper checks are susceptible to loss, theft, and forgery. Direct deposit bypasses these risks entirely, as funds are transferred electronically through secure networks. This reduces the anxiety associated with handling and storing physical checks.

- Timely Access to Funds: With direct deposit, paychecks, benefits, or refunds are available on the designated payday or disbursement date, often as soon as the transaction is processed. This predictable access to funds allows for better budgeting and financial planning, preventing potential cash flow issues.

- Reduced Risk of Fraud: Compared to paper checks, direct deposits are significantly less prone to fraudulent activities. The electronic nature of the transfer and the robust security measures within the ACH network make it far more difficult for malicious actors to intercept or alter funds.

- Facilitating Automatic Payments: Direct deposit seamlessly integrates with other financial management tools. It makes setting up automatic bill payments, savings transfers, or contributions to investment accounts incredibly simple and reliable. This automation further enhances financial control and reduces the risk of missed payments.

For Businesses: Efficiency, Cost Savings, and Employee Satisfaction

The advantages of direct deposit extend powerfully to businesses, impacting their bottom line and operational effectiveness.

- Streamlined Payroll Processing: Direct deposit significantly simplifies and automates the payroll process. Employers can send payments to multiple employees simultaneously, reducing the administrative burden associated with printing, signing, and distributing paper checks. This automation leads to substantial time savings for payroll departments.

- Reduced Costs: The cost of issuing paper checks, including printing, postage, and bank fees, can be considerable. Direct deposit eliminates these expenses, leading to direct cost savings for businesses. Furthermore, it reduces the risk of lost or stolen checks, which can incur additional administrative costs for replacement.

- Improved Cash Flow Management: By facilitating timely and predictable disbursements, direct deposit helps businesses better manage their cash flow. Knowing precisely when funds will leave their accounts allows for more accurate financial forecasting and planning.

- Enhanced Employee Morale and Retention: Offering direct deposit is often seen as a standard benefit by employees. Its convenience and security contribute to a positive employee experience, potentially improving morale and aiding in recruitment and retention efforts. Employees appreciate the ease and reliability of receiving their pay directly into their accounts.

- Environmental Benefits: Reducing the reliance on paper checks also contributes to environmental sustainability by decreasing paper consumption and the associated waste.

Direct Deposit Beyond Payroll: A Versatile Financial Tool

While direct deposit is most commonly associated with payroll, its utility extends far beyond this primary application. It has become a versatile tool for a wide array of financial transactions, offering similar benefits of speed, security, and convenience across different scenarios.

Government Benefits and Tax Refunds

Governments at all levels leverage direct deposit to disburse benefits and issue refunds efficiently. This includes:

- Social Security Benefits: Millions of individuals receive their Social Security payments directly into their bank accounts via direct deposit.

- Veterans Affairs (VA) Benefits: Payments to veterans, including disability compensation and pensions, are often made through direct deposit.

- Tax Refunds: The IRS and state tax agencies increasingly encourage taxpayers to opt for direct deposit of their tax refunds, offering faster access to their money.

- Unemployment Benefits: State unemployment agencies utilize direct deposit to deliver benefits to eligible individuals.

Other Common Uses

The reach of direct deposit continues to expand, encompassing a variety of other financial flows:

- Insurance Payouts: Insurance companies may use direct deposit to disburse claim payments, such as for auto accidents, property damage, or medical expenses.

- Pension and Annuity Payments: Retirees often receive their pension or annuity payments directly into their accounts.

- Investment Dividends: Many brokerage firms and corporations can direct dividend payments to an investor’s bank account.

- Rebates and Refunds: Companies issuing product rebates or customer refunds frequently offer direct deposit as an option.

- Gig Economy Payments: Freelancers and independent contractors working for platforms like Uber, Lyft, or Upwork often receive their earnings through direct deposit.

Security and Considerations for Direct Deposit

While direct deposit is inherently secure, like any financial transaction, understanding its security features and potential considerations is crucial for users.

Robust Security Measures

The ACH network is designed with multiple layers of security to protect against fraud and ensure the integrity of transactions.

- Encryption: Data transmitted within the ACH network is encrypted, making it unreadable to unauthorized parties.

- Authentication and Verification: Financial institutions employ rigorous authentication and verification processes to ensure that only authorized parties can initiate or receive direct deposits.

- Rules and Regulations: Nacha’s comprehensive rules and regulations govern the ACH network, setting strict standards for participants and providing a framework for dispute resolution.

- Fraud Monitoring: Banks and ACH operators continuously monitor transactions for suspicious activity, employing sophisticated algorithms to detect and flag potential fraud.

Potential Issues and How to Address Them

While rare, issues can arise with direct deposits. Being aware of these potential problems and knowing how to address them can save significant hassle.

- Incorrect Account Information: The most common issue is an error in the account number or routing number provided. This can lead to the deposit being rejected or, in rare cases, sent to the wrong account.

- Resolution: If a deposit fails due to incorrect information, the funds will typically be returned to the sender. The sender will then need to contact the recipient to obtain the correct account details and re-initiate the deposit. It’s crucial to double-check all banking information when setting up direct deposit.

- Delayed Deposits: While usually prompt, occasional delays can occur due to processing errors, bank holidays, or system issues.

- Resolution: If a direct deposit is significantly delayed, contact your bank first. They can check their records to see if the funds have been received but not yet posted to your account. If the bank has not received the funds, contact the initiating party (e.g., your employer, government agency) to inquire about the status of the payment.

- Unauthorized Deposits: Though uncommon due to robust security, instances of unauthorized deposits can occur.

- Resolution: If you notice any deposits in your account that you do not recognize, immediately contact your financial institution. They have procedures in place to investigate and resolve such discrepancies.

In conclusion, direct deposit has transformed the way we handle our finances. Its efficiency, security, and convenience have made it an indispensable tool for individuals and businesses alike, underpinning the smooth functioning of countless daily transactions. From the fundamental mechanics of the ACH network to its broad applications beyond payroll, direct deposit stands as a prime example of how technological innovation can significantly enhance financial management and accessibility.