The rapid proliferation of unmanned aerial vehicles (UAVs) has transformed industries ranging from precision agriculture to high-end cinematography. However, as drone technology becomes more sophisticated and expensive, the financial risks associated with hardware failure, pilot error, and environmental hazards have grown exponentially. For professional pilots and dedicated hobbyists alike, drone insurance is no longer an optional luxury but a fundamental component of operational safety. Central to any insurance policy is the concept of the “deductible.”

In the context of the drone industry, a deductible represents the out-of-pocket expense an operator must pay before the insurance provider covers the remaining costs of a claim. Whether you are flying a compact FPV racing drone or a high-end enterprise platform equipped with LiDAR sensors, understanding how deductibles function is critical to managing your overhead and protecting your investment.

The Mechanics of Drone Insurance Deductibles

At its core, a deductible is a risk-sharing mechanism between the drone operator and the insurance company. By requiring the pilot to pay a portion of the repair or replacement costs, insurers ensure that operators maintain a high standard of care and flight discipline. In the drone niche, deductibles typically apply to “Hull Coverage”—the portion of the policy that protects the physical aircraft and its mounted components.

The Relationship Between Premiums and Deductibles

One of the most important concepts for a UAV pilot to grasp is the inverse relationship between the policy premium and the deductible. The premium is the recurring cost you pay to keep the insurance active (monthly or annually), while the deductible is the one-time cost paid at the time of an incident.

Generally, choosing a higher deductible will lower your premium. This is because the insurance company is taking on less financial risk for minor accidents. Conversely, a “zero-deductible” or low-deductible policy will result in higher monthly premiums, as the insurer is responsible for almost the entire cost of even minor “fender benders” in the sky. For a commercial operation managing a fleet of DJI Matrice 300 RTK units, deciding where to strike this balance is a significant financial strategy.

Fixed vs. Percentage-Based Deductibles

In the drone world, deductibles usually manifest in two ways: fixed dollar amounts or a percentage of the total insured value.

- Fixed Deductibles: These are straightforward. Regardless of whether the repair cost is $1,000 or $5,000, the pilot pays a set amount, such as $250 or $500.

- Percentage-Based Deductibles: These are common in high-end enterprise insurance. The deductible might be set at 5% or 10% of the drone’s total value. If you are flying an enterprise rig worth $20,000, a 10% deductible means you are responsible for the first $2,000 of any claim. This structure is particularly prevalent in policies covering expensive specialized payloads like thermal cameras or multispectral sensors.

Types of Coverage and Where Deductibles Apply

Not all drone insurance is created equal. Understanding where a deductible applies requires a clear distinction between liability coverage and hull coverage. In many drone-specific policies, the deductible only applies to the hardware itself, while liability claims might be handled differently.

Hull Coverage and Physical Damage

Hull coverage is the equivalent of “comprehensive” or “collision” protection. It covers the drone if it crashes into a tree, suffers a mid-air collision, or experiences a sudden technical malfunction that results in a “flyaway.” This is the primary area where deductibles come into play.

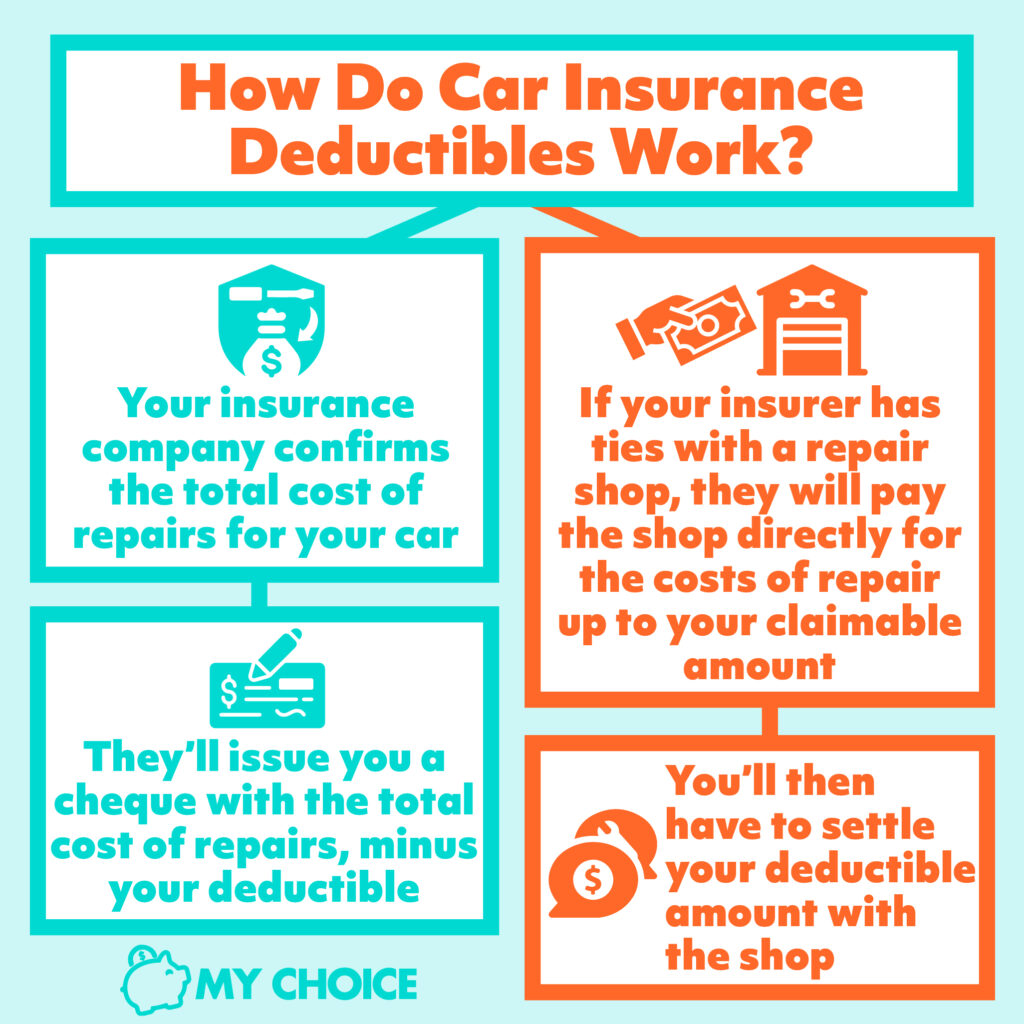

When a claim is filed for physical damage, the adjuster will evaluate the cost of parts (propellers, arms, motors, internal boards) and labor. If the total repair bill is $1,200 and your deductible is $300, the insurance company provides $900. If the drone is a total loss, the insurer typically pays out the “Agreed Value” or “Actual Cash Value” minus the deductible.

Manufacturer-Specific Protection Plans (DJI Care Refresh)

It is important to distinguish between traditional third-party insurance and manufacturer protection plans like DJI Care Refresh or Autel Robotics Care. These programs act as a form of “pseudo-insurance” with very specific deductible structures.

Under these plans, the “deductible” is often referred to as a “replacement fee.” For a fixed price, the manufacturer will replace a crashed drone with a new or “like-new” unit. While these plans are highly efficient for recreational flyers and small-scale professionals using standard quadcopters, they often lack the broad liability protections required for major commercial contracts, making them a supplement to, rather than a replacement for, full-scale drone insurance.

Liability and Third-Party Property Damage

Liability insurance protects the pilot if the drone causes injury to a person or damages someone else’s property (e.g., crashing through a window or hitting a parked car). In many professional drone policies, liability coverage may have a $0 deductible. This is because the legal and medical costs associated with third-party injuries can be astronomical, and insurers prefer to manage these high-stakes claims directly without the friction of a deductible. However, pilots should always verify if a “Property Damage Deductible” applies to third-party claims.

Factors Influencing Deductible Rates for UAV Pilots

Insurance companies do not set deductibles at random. They utilize complex risk assessment models tailored to the specific nuances of flight technology and the pilot’s operational history.

Commercial vs. Recreational Flight Profiles

The intent of the flight significantly impacts the risk profile. A recreational flyer taking scenic photos at a local park represents a different risk level than a Part 107 certified pilot performing a bridge inspection in a high-wind environment or a cinematographer flying a heavy-lift cinema drone over a film set.

Commercial policies often offer more flexibility in deductible choice because professional pilots are expected to have higher levels of training and stricter maintenance logs. A pilot with hundreds of logged hours and a clean safety record may be eligible for lower deductibles or “disappearing deductibles,” where the cost decreases for every year of accident-free flight.

Equipment Value and Technological Complexity

The “tech stack” of the drone plays a massive role in insurance costs. A drone equipped with redundant flight controllers, obstacle avoidance sensors, and dual-battery systems is technically “safer,” which can lead to more favorable insurance terms. However, the sheer cost of these components means that when a crash does occur, the payout is higher.

Insuring a drone with a high-resolution 4K gimbal camera is one thing; insuring a drone with a $30,000 Phase One aerial camera system is another. In the latter case, the deductible is often set higher to ensure the operator has a significant stake in the safety of the mission.

Strategic Decision-Making: Choosing the Right Deductible

Selecting the right deductible is a balancing act between your monthly cash flow and your ability to absorb a sudden financial shock. As a drone operator, you must evaluate your “Risk Tolerance” against the value of your equipment.

Assessing Your Risk Tolerance

If you are a seasoned pilot operating in low-risk environments (wide-open fields, clear weather), you might opt for a higher deductible to keep your monthly operational costs low. You are essentially betting on your own skills and the reliability of your flight technology.

On the other hand, if you specialize in high-risk operations—such as FPV “proximity flying” for commercials or inspecting industrial indoor facilities—the likelihood of a minor “prop strike” or collision is much higher. In these scenarios, a lower deductible is often the smarter financial move, as it ensures that frequent small repairs don’t drain your business capital.

The Total Cost of Ownership (TCO) Approach

When calculating the total cost of owning and operating a drone, insurance must be factored into the hourly rate you charge clients. If you choose a high-deductible plan, you should ideally have a “reserve fund” set aside to cover that deductible at any moment.

For enterprise drone programs, the strategy often involves “Self-Insurance” for small items. For example, an organization might choose a $1,000 deductible, deciding that they will pay for all minor repairs (like replacing a single motor or a set of landing gear) out of pocket and only utilize the insurance policy for major “hull-loss” events. This prevents “claim inflation,” which can lead to higher premiums or policy cancellation in the future.

Conclusion

Deductibles are a fundamental aspect of the drone ecosystem, bridging the gap between technological innovation and financial security. As UAVs continue to integrate into the national airspace, the sophistication of insurance products will only increase. By understanding how deductibles work—from the interplay with premiums to the differences between hull and liability coverage—pilots can make informed decisions that protect both their equipment and their livelihoods. Whether you are navigating a micro-drone through a tight racing course or hovering a heavy-duty industrial platform over a construction site, the right deductible ensures that a single mistake doesn’t ground your operations permanently.