Understanding the fundamental principles of accounting is crucial, not just for seasoned financial professionals, but for anyone seeking to grasp the financial health of a business, whether it’s a small startup or a large corporation. At the heart of this understanding lie debits and credits. These terms, often misunderstood or perceived as overly complex, are in fact the building blocks of the double-entry bookkeeping system, a method that has remained the standard for centuries due to its inherent accuracy and comprehensiveness.

The Double-Entry System: A Foundation of Financial Accuracy

The double-entry bookkeeping system is built on a simple yet powerful concept: every financial transaction has two equal and opposite effects. Imagine a set of scales; for the scales to remain balanced, any weight added to one side must be matched by an equal weight added to the other. Similarly, in accounting, every debit entry must have a corresponding credit entry of the same amount. This inherent balance ensures that the accounting equation—Assets = Liabilities + Equity—always holds true.

This system was largely formalized by Luca Pacioli in the late 15th century, though its roots likely extend further back. Its enduring legacy is a testament to its effectiveness in tracking financial flows, preventing errors, and providing a clear picture of an entity’s financial standing. Without the dual recording of debits and credits, it would be nearly impossible to maintain accurate financial records, as a single entry could easily lead to discrepancies that go unnoticed.

The Accounting Equation: Assets, Liabilities, and Equity

The fundamental accounting equation, Assets = Liabilities + Equity, is the bedrock upon which debits and credits operate.

- Assets represent everything a business owns that has value and can be used to generate future economic benefits. This includes tangible items like cash, inventory, equipment, and buildings, as well as intangible assets like patents and copyrights.

- Liabilities represent what a business owes to others. These are its obligations to external parties, such as accounts payable (money owed to suppliers), loans, and accrued expenses.

- Equity, also known as owner’s equity or shareholders’ equity, represents the residual interest in the assets of an entity after deducting all its liabilities. It’s essentially the net worth of the business from the owners’ perspective.

Every transaction impacts at least two accounts, and the double-entry system ensures that the accounting equation remains in balance. Understanding how debits and credits affect these components is key to mastering financial record-keeping.

Debits and Credits: Not Good or Bad, But Directions of Change

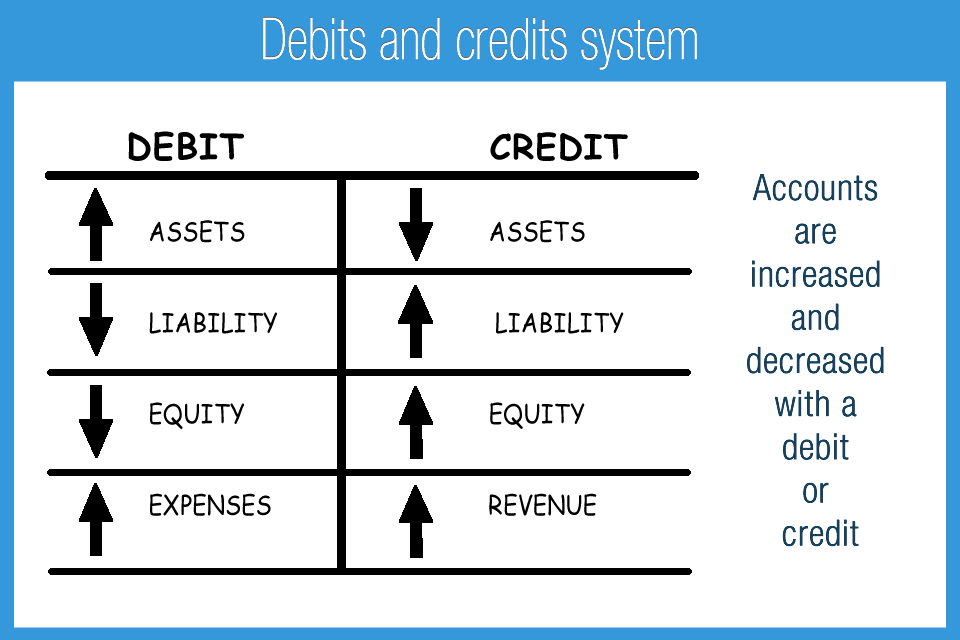

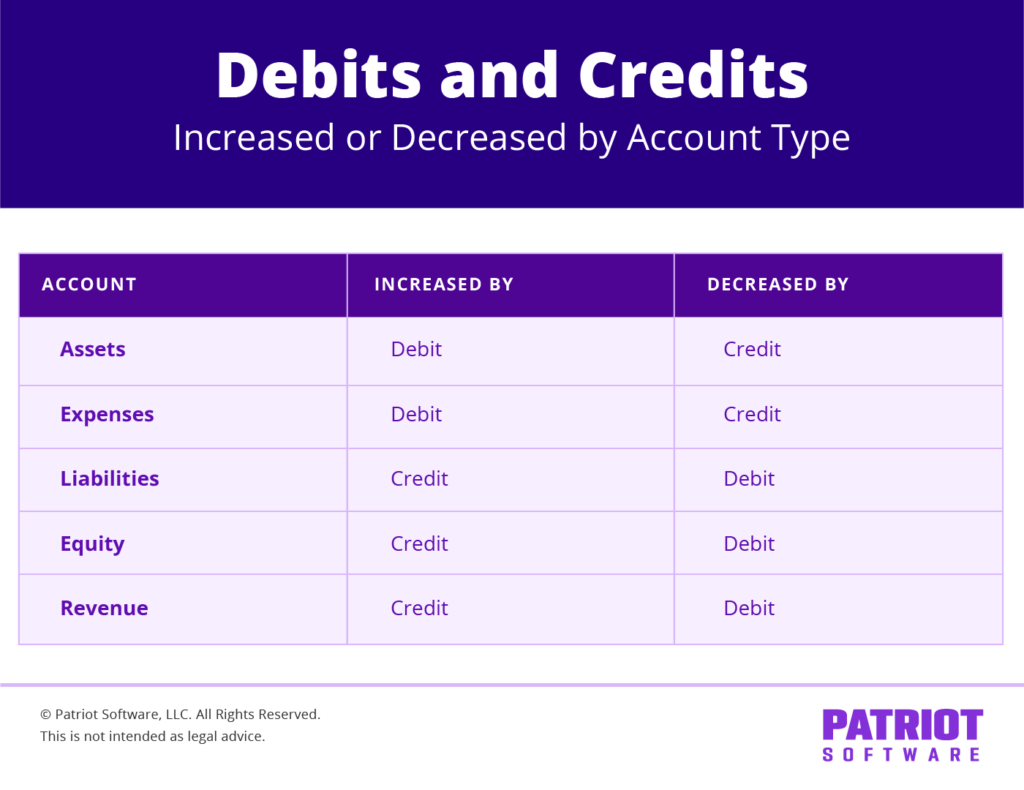

The most common misconception surrounding debits and credits is that they are inherently positive (credit) or negative (debit). This is incorrect. Instead, think of them as directional indicators within the accounting equation.

- Debits (Dr.): Generally, debits increase assets and expenses, and decrease liabilities, equity, and revenue.

- Credits (Cr.): Generally, credits increase liabilities, equity, and revenue, and decrease assets and expenses.

The impact of a debit or credit depends on the type of account it is applied to. This is where the five main account types come into play.

The Five Main Account Types

To effectively understand debits and credits, one must be familiar with the five primary categories of accounts in accounting:

1. Assets

As discussed, assets are resources owned by the business.

- How Debits and Credits Affect Assets:

- Debit: An increase in an asset account is recorded as a debit. For example, when a business receives cash, its cash account (an asset) increases, and this is recorded as a debit to cash. Similarly, when a business purchases equipment, its equipment account increases, and this is a debit to equipment.

- Credit: A decrease in an asset account is recorded as a credit. If a business uses cash to pay a supplier, its cash account decreases, and this is a credit to cash. If equipment is sold, its equipment account decreases, and this is a credit to equipment.

2. Liabilities

Liabilities represent obligations to external parties.

- How Debits and Credits Affect Liabilities:

- Debit: A decrease in a liability account is recorded as a debit. If a business repays a loan, its loan payable account (a liability) decreases, and this is a debit to the loan payable.

- Credit: An increase in a liability account is recorded as a credit. When a business takes out a new loan, its loan payable account increases, and this is a credit to loan payable. Purchasing goods on credit from a supplier also increases accounts payable, which is a credit.

3. Equity

Equity represents the owners’ stake in the business.

- How Debits and Credits Affect Equity:

- Debit: A decrease in equity is recorded as a debit. This can happen when the owner withdraws money from the business (drawings or dividends) or when the business incurs a net loss.

- Credit: An increase in equity is recorded as a credit. This typically occurs when the owner invests more capital into the business or when the business generates a net profit.

4. Revenue

Revenue represents the income generated from the business’s primary operations.

- How Debits and Credits Affect Revenue:

- Debit: A decrease in revenue is recorded as a debit. This might occur due to sales returns or allowances.

- Credit: An increase in revenue is recorded as a credit. When a business makes a sale, its revenue account increases, and this is recorded as a credit to revenue.

5. Expenses

Expenses are the costs incurred in the process of generating revenue.

- How Debits and Credits Affect Expenses:

- Debit: An increase in an expense account is recorded as a debit. When a business pays rent, its rent expense account increases, and this is a debit to rent expense. Similarly, paying salaries, utilities, or advertising costs are debits to their respective expense accounts.

- Credit: A decrease in an expense account is recorded as a credit. This is less common but could occur, for instance, if an expense payment was made in error and is subsequently reversed.

T-Accounts: Visualizing Debits and Credits

To better visualize the impact of debits and credits on specific accounts, accountants often use “T-accounts.” A T-account is a simplified representation of a ledger account, shaped like the letter “T.” The left side represents debits, and the right side represents credits.

For example, a T-account for “Cash” would look like this:

Cash

| Debit (Dr.) | Credit (Cr.) |

|---|---|

| (Increases) | (Decreases) |

When cash is received, it’s entered on the debit side. When cash is paid out, it’s entered on the credit side. The balance of the account is determined by subtracting the total credits from the total debits (for asset accounts).

Similarly, a T-account for “Accounts Payable” (a liability) would look like this:

Accounts Payable

| Debit (Dr.) | Credit (Cr.) |

|---|---|

| (Decreases) | (Increases) |

When a debt is paid, it’s debited (decreasing the liability). When new debts are incurred, they are credited (increasing the liability).

The Journal Entry: Recording Transactions

Financial transactions are initially recorded in a journal, often referred to as the “book of original entry.” Each transaction is documented as a journal entry, which clearly shows the date, the accounts affected, whether each account is debited or credited, and the amounts.

A typical journal entry format is as follows:

- Date: The date the transaction occurred.

- Debit Account(s): The account(s) being debited, listed first.

- Credit Account(s): The account(s) being credited, indented below the debit accounts.

- Debit Amount(s): The amount(s) debited.

- Credit Amount(s): The amount(s) credited.

- Description: A brief explanation of the transaction.

Example Journal Entry:

On January 15, 2024, a company purchased $500 worth of office supplies on credit.

| Date | Account | Debit | Credit |

|---|---|---|---|

| 2024-01-15 | Office Supplies Expense | $500 | |

| Accounts Payable | $500 | ||

| To record purchase of office supplies |

In this example:

- “Office Supplies Expense” is debited because expenses increase with debits.

- “Accounts Payable” is credited because liabilities increase with credits.

The total debits ($500) equal the total credits ($500), maintaining the balance of the double-entry system.

The Ledger: Organizing Financial Data

After being recorded in the journal, transactions are then posted to the appropriate accounts in the ledger. The ledger is a collection of all the T-accounts, providing a comprehensive view of each account’s activity over a period. The process of transferring information from the journal to the ledger is called posting.

The balanced nature of debits and credits ensures that once all transactions are posted to the ledger, the trial balance can be prepared. The trial balance is a list of all ledger accounts and their balances (debit or credit). If the total of all debit balances equals the total of all credit balances, it indicates that the ledger is arithmetically in balance. While a balanced trial balance doesn’t guarantee the absence of all errors (e.g., an incorrect account might have been used), it’s a critical step in verifying the accuracy of the accounting system.

Conclusion: Mastering the Language of Business

Debits and credits are the fundamental language of accounting. By understanding their role within the double-entry system and their impact on the five primary account types (assets, liabilities, equity, revenue, and expenses), individuals can gain significant insight into the financial operations and performance of any business. This foundational knowledge is not only essential for accounting professionals but also empowers entrepreneurs, investors, and managers to make informed decisions based on a clear and accurate representation of financial reality. The consistent application of these principles ensures financial integrity and provides the bedrock for robust financial reporting.