An Individual Retirement Arrangement (IRA) is a powerful financial tool designed to help individuals save for retirement with significant tax advantages. In essence, it’s a type of investment account where your contributions grow tax-deferred or tax-free, depending on the type of IRA you choose. The primary goal of an IRA is to encourage long-term saving by making it more financially appealing to set aside funds for your future, rather than consuming them in the present. Understanding the nuances of IRAs is crucial for anyone looking to secure their financial future and build a nest egg that can sustain them during their post-working years.

The concept of an IRA emerged from the U.S. tax code, aiming to provide a retirement savings vehicle for individuals who might not have access to employer-sponsored plans like 401(k)s, or for those who wish to supplement their existing retirement savings. Over the years, IRAs have evolved, with different types offering varying benefits and contribution rules. Whether you’re just starting your career or are a seasoned professional, a well-structured IRA strategy can significantly impact your retirement security. This article will delve into the fundamental aspects of what an IRA account is, its core benefits, and the different types available, providing a comprehensive overview for informed decision-making.

The Core Purpose and Benefits of an IRA

At its heart, an IRA is a mechanism for long-term wealth accumulation, specifically earmarked for retirement. The overarching benefit stems from its tax-advantaged nature. This means the government offers incentives – in the form of tax breaks – to encourage individuals to save for their golden years. These benefits can manifest in several ways, significantly enhancing the growth potential of your investments compared to a taxable brokerage account.

Tax Advantages: The Driving Force Behind IRA Popularity

The primary allure of an IRA lies in its tax treatment. This is not a one-size-fits-all approach; different types of IRAs offer distinct tax advantages. Understanding these distinctions is key to maximizing the benefit for your personal financial situation.

Tax-Deferred Growth: Letting Your Money Work Harder

In most IRAs, known as Traditional IRAs, your investments grow tax-deferred. This means you don’t pay any taxes on the dividends, interest, or capital gains your investments generate year after year, as long as the money remains within the IRA. This deferral allows your earnings to compound more effectively. Imagine your earnings in a taxable account being taxed annually, reducing the principal that can then earn further returns. In an IRA, the entire amount continues to grow, potentially leading to a substantially larger nest egg over time. This compounding effect is a powerful engine for wealth creation, and tax deferral is its fuel.

Tax-Free Withdrawals: Enjoying Your Retirement Income

The most attractive aspect of Roth IRAs is the prospect of tax-free withdrawals in retirement. With a Roth IRA, you contribute after-tax dollars, meaning you don’t get an upfront tax deduction. However, the magic happens later. All qualified withdrawals in retirement – including both your contributions and all the investment earnings – are completely tax-free. This provides immense certainty and predictability regarding your retirement income, as you won’t have to worry about the tax implications of accessing your savings. For many, this predictability is invaluable, especially if they anticipate being in a higher tax bracket in retirement than they are currently.

Encouraging Long-Term Savings Habits

Beyond the direct tax benefits, IRAs serve as a powerful psychological tool, encouraging individuals to adopt and maintain consistent savings habits. The designation of the account specifically for retirement creates a mental separation from funds needed for short-term goals. This separation makes it less tempting to dip into retirement savings for immediate expenses. The rules surrounding early withdrawals, which often come with penalties and taxes, further reinforce the long-term nature of these accounts. By making it slightly inconvenient to access these funds prematurely, IRAs help protect your retirement nest egg from the erosive effects of impulsive spending or short-sighted financial decisions.

Flexibility and Investment Control

While IRAs offer significant tax advantages, they also provide a substantial degree of flexibility in terms of investment choices. Unlike some employer-sponsored plans that might limit your options to a curated list of mutual funds, IRAs generally allow you to invest in a broad range of assets. This can include stocks, bonds, mutual funds, exchange-traded funds (ETFs), and even, with some custodians, alternative investments like real estate or precious metals. This control empowers you to tailor your investment portfolio to your specific risk tolerance, time horizon, and financial goals, allowing for a more personalized retirement savings strategy.

Key Types of Individual Retirement Arrangements

The landscape of IRAs is not monolithic. Several distinct types cater to different financial situations and retirement planning preferences. The two most prominent are the Traditional IRA and the Roth IRA, each with its own set of rules regarding contributions, deductions, and withdrawals. Understanding these differences is fundamental to choosing the IRA that best aligns with your financial trajectory.

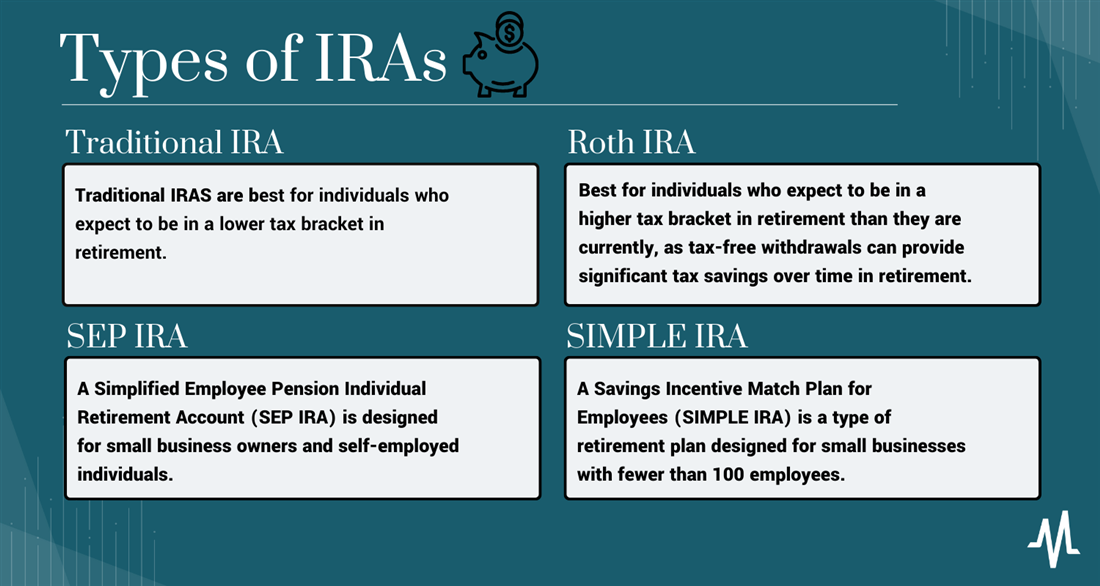

The Traditional IRA: The Classic Tax-Deferred Approach

The Traditional IRA has been a cornerstone of retirement planning for decades. Its primary appeal lies in the potential for an upfront tax deduction on contributions, which can lower your taxable income in the present year. This makes it particularly attractive for individuals who expect to be in a lower tax bracket during their retirement years than they are currently.

Contribution Limits and Deductibility

The IRS sets annual limits on how much an individual can contribute to a Traditional IRA. These limits are subject to change and are often indexed for inflation. For those under age 50, there’s a standard contribution limit. Individuals aged 50 and over can make “catch-up” contributions, allowing them to save even more. The deductibility of your contributions is a crucial element. If you and your spouse are covered by a retirement plan at work, your ability to deduct Traditional IRA contributions may be phased out based on your modified adjusted gross income (MAGI). If neither you nor your spouse is covered by a workplace retirement plan, you can generally deduct your full contribution, regardless of your income.

Required Minimum Distributions (RMDs)

A key characteristic of Traditional IRAs is the requirement for Required Minimum Distributions (RMDs). Once you reach a certain age, typically 73 as of current regulations (this age has been subject to legislative changes), you are mandated by the IRS to start withdrawing a minimum amount from your Traditional IRA each year. These withdrawals are treated as taxable income. The RMD calculation is based on your account balance at the end of the previous year and your life expectancy. This rule ensures that individuals eventually pay taxes on the retirement savings that have benefited from tax deferral over many years.

The Roth IRA: The Power of Tax-Free Retirement Income

The Roth IRA, introduced in 1997, offers a fundamentally different approach to retirement savings by prioritizing tax-free withdrawals in retirement. While you don’t receive an upfront tax deduction, the long-term benefit of tax-free income in your retirement years can be incredibly valuable, especially for those who anticipate higher tax rates in the future or want to ensure a predictable stream of income.

Contribution Eligibility and Income Limits

Eligibility to contribute directly to a Roth IRA is subject to income limitations. The IRS sets MAGI thresholds, and if your income exceeds these limits, you may not be able to contribute directly to a Roth IRA. However, there are often “backdoor Roth IRA” strategies available for high-income earners, allowing them to contribute indirectly. Like Traditional IRAs, Roth IRAs also have annual contribution limits, with catch-up contributions available for those aged 50 and over.

Qualified Withdrawals and Flexibility

The primary advantage of a Roth IRA is that qualified withdrawals in retirement are entirely tax-free. To be considered qualified, withdrawals of both contributions and earnings must meet specific criteria. Generally, you must be at least 59½ years old, and the account must have been open for at least five years. One significant benefit of Roth IRAs is that your original contributions can be withdrawn at any time, tax- and penalty-free, without needing to meet the age or five-year rule. This offers a level of flexibility not available with Traditional IRAs for accessing principal. Unlike Traditional IRAs, Roth IRAs do not have RMDs for the original account owner. This means you can leave the money to grow tax-free for as long as you live and even pass it on to beneficiaries.

Other Considerations and Strategic Uses of IRAs

Beyond the fundamental distinctions between Traditional and Roth IRAs, there are other important considerations and strategic ways these accounts can be leveraged to enhance retirement planning and financial well-being. These include understanding withdrawal rules, the potential for rollovers, and how IRAs can complement other retirement savings vehicles.

Early Withdrawal Penalties and Exceptions

Accessing funds from an IRA before the age of 59½ typically incurs a 10% early withdrawal penalty on top of ordinary income taxes (for Traditional IRAs) or on the earnings portion (for Roth IRAs). However, the IRS provides several exceptions to this penalty. These exceptions are designed to offer relief in specific life events. Common qualified exceptions include using the funds for qualified higher education expenses, a first-time home purchase (up to a lifetime limit), unreimbursed medical expenses exceeding a certain percentage of your adjusted gross income, or distributions made due to disability. It’s crucial to consult the IRS guidelines or a financial advisor to determine if your withdrawal qualifies for an exception to avoid unexpected penalties.

Rollovers and Transfers: Maintaining Tax Advantages

Life circumstances can change, and so can your retirement savings strategy. IRAs offer flexibility through the process of rollovers and transfers. A rollover allows you to move funds from one IRA to another, or from an employer-sponsored plan (like a 401(k) or 403(b)) into an IRA, without incurring taxes or penalties, provided certain rules are followed. There are two main types of rollovers: direct rollovers, where the funds are transferred directly from the old custodian to the new one, and indirect rollovers, where you receive the distribution and have 60 days to deposit it into a new account. Indirect rollovers involve mandatory 20% withholding, which you must make up from other funds to avoid taxes on that portion. Understanding the intricacies of rollovers is essential for seamless transitions and preserving the tax-advantaged status of your retirement savings.

Complementing Employer-Sponsored Plans

For many individuals, particularly those with access to employer-sponsored retirement plans like 401(k)s or 403(b)s, IRAs are not mutually exclusive options. Instead, they serve as valuable complements. If you contribute enough to your employer plan to receive the full employer match (which is essentially free money), you can then consider opening an IRA to further boost your retirement savings. The choice between a Traditional and Roth IRA, in conjunction with an employer plan, often depends on your current income, anticipated future income, and tax situation. Some individuals max out their employer plan and then contribute to an IRA, while others might prioritize IRA contributions if they offer more desirable investment options or tax benefits for their specific circumstances.

Estate Planning Considerations

IRAs also play a significant role in estate planning. When the account holder passes away, the remaining assets in the IRA are transferred to their beneficiaries. The tax treatment of inherited IRAs depends on the type of IRA and the beneficiary. Beneficiaries of Traditional IRAs will generally owe income tax on the distributions they take, while beneficiaries of Roth IRAs will typically receive the distributions tax-free. Rules governing inherited IRAs, including distribution requirements and timelines, have been subject to change, making it essential to have a clear beneficiary designation on your IRA and to review it periodically. Consulting with an estate planning attorney and a financial advisor can ensure your IRA assets are distributed according to your wishes and in the most tax-efficient manner for your heirs.