The concept of a “pro rata share” is fundamental to understanding fairness and equitable distribution in various financial and legal contexts. At its core, it signifies a proportional division of something – be it profits, losses, assets, or obligations – among individuals or entities based on their respective ownership, investment, or contribution. The Latin phrase “pro rata” itself translates to “in proportion,” perfectly encapsulating the principle. Understanding how pro rata shares are calculated and applied is crucial for investors, business partners, beneficiaries of estates, and anyone involved in shared ventures.

The application of pro rata shares spans a wide spectrum, from the distribution of dividends to shareholders to the division of inheritance among heirs, and even the allocation of costs in shared projects. The underlying idea is to ensure that each party receives or contributes their fair portion, reflecting their stake or commitment. This principle promotes transparency and prevents arbitrary or unfair outcomes.

Understanding the Core Principle of Pro Rata

The foundation of a pro rata share lies in the concept of proportionality. It’s not about an equal split, but rather a split that accurately reflects the relative size of each participant’s involvement. Imagine a pie that needs to be divided. If one person contributed twice as much money to buy the pie as another person, they would logically expect to receive twice as large a slice. This is the essence of a pro rata share – a division that aligns with established proportions.

Defining the Basis of Proportion

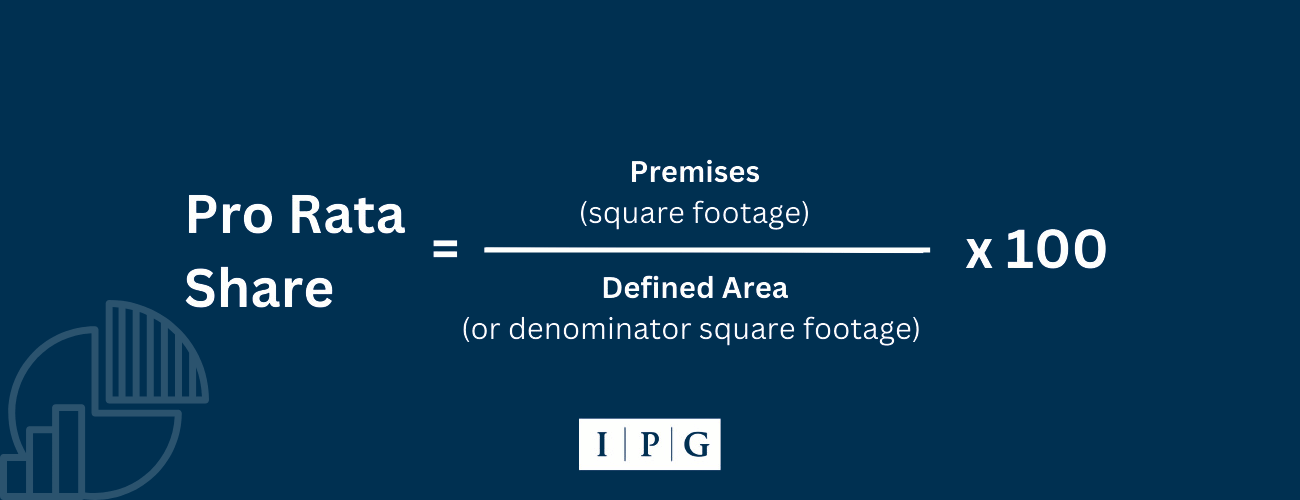

The “basis of proportion” is the key metric used to determine how a pro rata share is calculated. This basis can vary significantly depending on the context. In a corporate setting, the basis is typically the number of shares owned. If a company has 1,000 shares outstanding and you own 100 shares, your pro rata share of any dividend distribution would be 10% (100/1000).

However, the basis isn’t always so straightforward. In partnerships, it might be the capital contribution, the profit-sharing ratio stipulated in the partnership agreement, or even the amount of time and effort contributed, as defined by the partners. For beneficiaries of an estate, the basis is usually determined by the deceased’s will or intestacy laws, specifying the proportion each heir is entitled to receive.

The Mathematical Calculation: A Simple Framework

The actual calculation of a pro rata share, while seemingly complex in some scenarios, boils down to a straightforward mathematical formula. The general approach involves identifying the total amount to be divided and the total basis for that division. Then, for each individual or entity, their specific basis is divided by the total basis, and this ratio is multiplied by the total amount to be divided.

Let’s consider an example: Suppose a company decides to distribute $10,000 in dividends. The company has 500 shares outstanding, and you own 50 of those shares.

- Total Amount to be Divided: $10,000

- Total Basis (Total Shares): 500 shares

- Your Basis (Your Shares): 50 shares

Your pro rata share would be calculated as follows:

(Your Basis / Total Basis) * Total Amount to be Divided

(50 shares / 500 shares) * $10,000 = 0.10 * $10,000 = $1,000

Therefore, you would receive a pro rata share of $1,000 in dividends. This simple framework can be adapted to various situations by changing the “basis” and the “total amount to be divided.”

Pro Rata Shares in Corporate Finance and Investment

In the realm of corporate finance and investment, pro rata shares are a ubiquitous concept, impacting everything from stock ownership to rights offerings and corporate actions. Shareholders, by virtue of their ownership stake, are entitled to a pro rata share of the company’s profits, assets, and voting rights. This principle ensures that those who have invested more capital and thus bear more risk, also stand to gain proportionally more from the company’s success.

Shareholder Rights and Dividend Distribution

One of the most common applications of pro rata shares is in the distribution of dividends. When a company declares a dividend, it is typically paid out to shareholders on a pro rata basis. This means that each shareholder receives an amount of dividend proportional to the number of shares they hold. If a company declares a $1 per share dividend, a shareholder with 100 shares will receive $100, while a shareholder with 1,000 shares will receive $1,000. This system directly links the return on investment to the extent of ownership.

Beyond dividends, shareholders also have pro rata rights to other corporate benefits. For example, if a company issues new shares, existing shareholders may have preemptive rights, allowing them to purchase a pro rata portion of the new shares before they are offered to the public. This ensures that their ownership percentage is not diluted by the issuance of new stock, maintaining their relative voting power and claim on future profits.

Dilution and Preemptive Rights

Shareholder dilution occurs when the issuance of new shares by a company reduces the ownership percentage of existing shareholders. Pro rata principles are central to understanding and preventing unfair dilution. Preemptive rights are a mechanism designed to protect existing shareholders from this dilution.

For instance, if a company with 100,000 shares outstanding decides to issue an additional 20,000 shares, a shareholder who owns 1,000 shares currently holds 1% of the company (1,000 / 100,000). Without preemptive rights, after the new issuance, the company will have 120,000 shares, and that same shareholder will now hold approximately 0.83% (1,000 / 120,000). Their claim on future profits and voting power has been diminished.

However, if the shareholder has preemptive rights, they have the right to purchase a pro rata portion of the new shares. In this scenario, they would have the right to purchase 1% of the new shares, which is 200 shares (1% of 20,000). By exercising this right, they can maintain their 1% ownership stake (1,000 + 200 = 1,200 shares out of 120,000 total shares). This ensures that their proportional ownership and the associated rights are preserved.

Pro Rata in Legal and Estate Planning

The principle of pro rata distribution is equally vital in legal contexts, particularly in estate planning and bankruptcy proceedings. It provides a framework for ensuring fairness and equity when dividing assets among multiple claimants or beneficiaries. The clarity offered by pro rata calculations helps to avoid disputes and ensures that legal directives are followed accurately.

Estate Distribution and Inheritance

When an individual passes away, their assets are distributed to their beneficiaries according to their will or, in the absence of a will, according to intestacy laws. If there are multiple beneficiaries entitled to a share of the estate, and the assets are insufficient to satisfy all bequests fully, or if a specific asset is to be divided among several individuals, pro rata principles often come into play.

For example, if a will states that a specific piece of jewelry is to be divided equally among three children, each child receives one-third. However, if the will indicates that a particular fund is to be distributed among heirs in proportion to their age, the eldest would receive the largest share, the youngest the smallest, and the middle child a proportion in between, all calculated pro rata based on their ages relative to the total age of all beneficiaries. This ensures that the testator’s intentions, as expressed in the will or by law, are executed fairly based on the specified proportions.

Bankruptcy and Creditor Claims

In bankruptcy proceedings, the concept of pro rata shares is fundamental to how creditors are repaid. When a company or individual declares bankruptcy, their assets are liquidated, and the proceeds are distributed among creditors. Often, the total amount of debt owed to creditors exceeds the value of the assets available for distribution. In such cases, creditors do not typically receive 100% of what they are owed.

Instead, the available funds are distributed on a pro rata basis. Each creditor receives a proportion of their outstanding claim that is equal to the proportion of the total available assets to the total debt owed to all creditors. For instance, if there are $100,000 in assets to be distributed and $500,000 in total debt, each dollar owed to a creditor will be paid back at a rate of $0.20 ($100,000 / $500,000). A creditor owed $10,000 would receive $2,000 ($10,000 * 0.20). This equitable distribution aims to ensure that all creditors are treated fairly, even if they cannot be fully compensated.

Nuances and Considerations in Pro Rata Calculations

While the principle of pro rata shares is generally straightforward, several nuances and considerations can arise, particularly when dealing with complex financial instruments, fluctuating values, or specific contractual agreements. Understanding these factors is essential for accurate calculations and to avoid potential misunderstandings.

Fluctuating Values and Timing

One of the critical aspects of pro rata calculations is the timing and the value of the asset or profit being distributed. In some cases, the value of an asset might fluctuate significantly over time, or the timing of a distribution might be subject to change. This can impact the final pro rata share received.

For example, if a mutual fund decides to distribute capital gains to its investors, the value of the fund might change between the declaration of the distribution and the actual payout. Similarly, if a partnership agreement outlines profit distribution based on the capital account balance at the end of the fiscal year, any changes in capital contributions or withdrawals during the year can affect the pro rata share. It is crucial to adhere to the specific valuation dates and methodologies stipulated in relevant agreements or regulations.

Contractual Agreements and Modifications

The application of pro rata shares can often be modified or superseded by specific contractual agreements. While the default legal principle might dictate a proportional distribution, parties can mutually agree to different terms. For instance, a partnership agreement might explicitly state that profits are to be divided not by capital contribution but by a fixed ratio or based on performance metrics.

Similarly, in mergers and acquisitions, the terms of the deal can alter how assets or liabilities are distributed. While pro rata is a common starting point, complexities in negotiations might lead to different allocation methods. It is always imperative to carefully review all contractual clauses and legal documents to understand the exact terms governing any pro rata distribution, as these agreements often take precedence over general legal principles.

Tax Implications of Pro Rata Distributions

Pro rata distributions often have significant tax implications for the recipients. Dividends, for example, are typically considered taxable income. The tax treatment can vary depending on the type of dividend (qualified vs. non-qualified) and the tax jurisdiction. Similarly, distributions from estates or capital gains from investment redemptions can trigger tax liabilities.

It is essential for individuals and entities to understand the tax consequences associated with their pro rata shares. This often involves consulting with tax professionals to ensure proper reporting and compliance with tax laws. For instance, when a company issues rights that are exercised, the tax treatment of those rights and any subsequent stock acquired can be complex. Understanding how the pro rata nature of these events impacts tax liabilities is crucial for financial planning.

In conclusion, the pro rata share is a fundamental concept of equitable division, ensuring fairness and proportionality in a myriad of financial and legal scenarios. Whether in corporate finance, estate planning, or bankruptcy, understanding how to calculate and apply pro rata shares is essential for informed decision-making, transparent dealings, and the equitable distribution of resources. Its adaptability, coupled with the underlying principle of fairness, makes it an indispensable tool in our financial and legal frameworks.