In the rapidly evolving landscape of unmanned aerial vehicles (UAVs), the leap from consumer-grade quadcopters to enterprise-level technology is often measured in tens of thousands of dollars. Whether you are an aerial cinematographer looking to acquire a heavy-lift rig for 8K RAW production or a surveyor integrating LiDAR-equipped platforms into your workflow, the acquisition of this technology is a major capital expenditure. Just as a consumer asks “what does APR mean when buying a car” to understand their long-term financial commitment, drone professionals and tech entrepreneurs must master the nuances of Annual Percentage Rate (APR) to scale their operations sustainably.

Understanding APR is not merely a task for the accounting department; it is a critical skill for any tech-driven business. In the context of tech and innovation, APR represents the true cost of borrowing the capital required to stay at the cutting edge.

The Core of APR: Why It Is the Gold Standard for UAV Investment

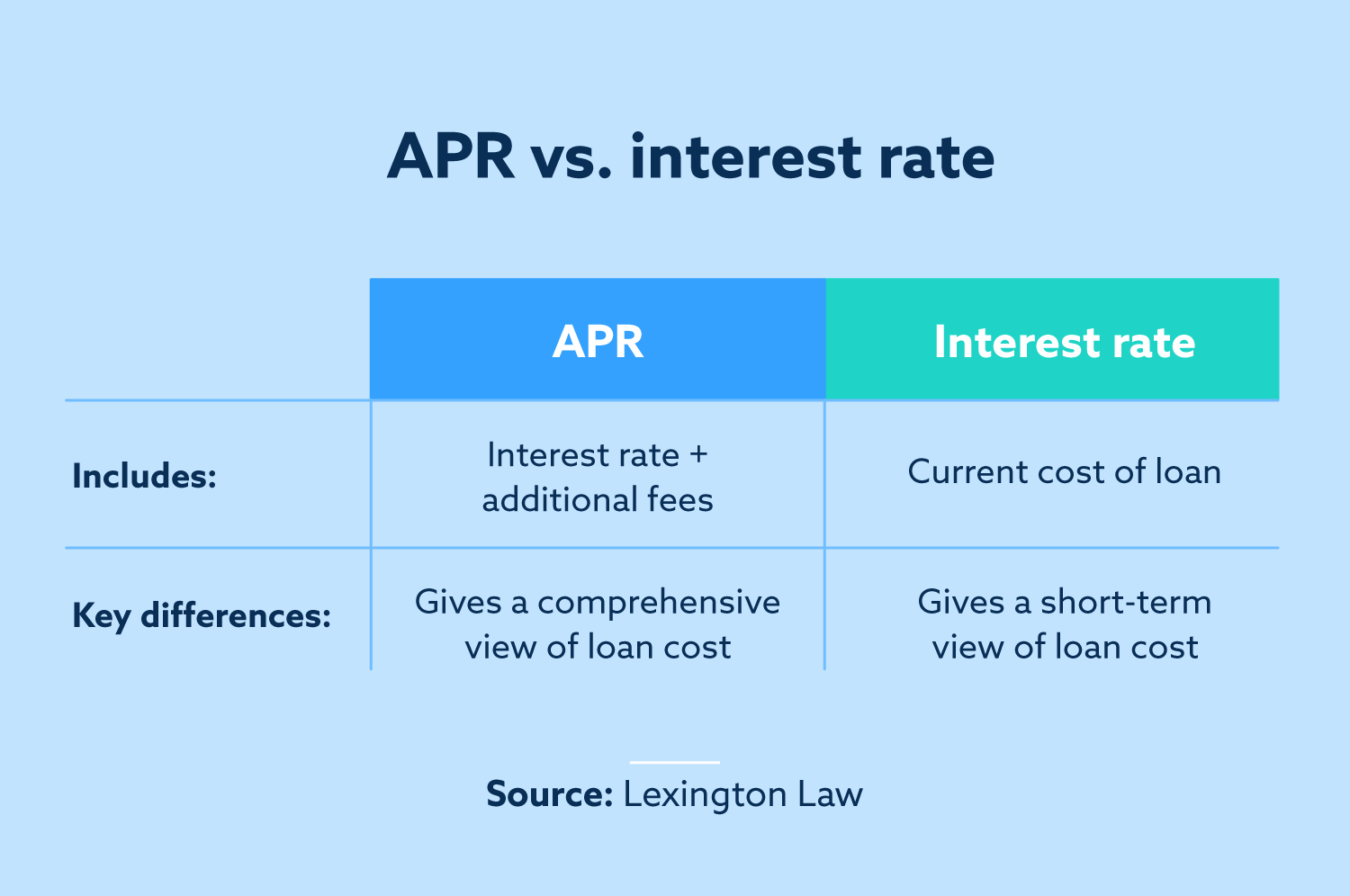

When you look at a financing offer for a new fleet of autonomous drones, you will see two numbers: the interest rate and the APR. While the interest rate tells you the cost of the principal, the APR provides a more holistic view of the total cost of the loan. In the tech industry, where specialized equipment often requires specific insurance, documentation fees, and setup costs, the APR is the only way to compare different financing options accurately.

Defining Annual Percentage Rate for Tech Acquisitions

APR is a percentage that represents the actual yearly cost of funds over the term of a loan. This includes any fees or additional costs associated with the transaction. When purchasing high-end drone technology—such as a DJI Matrice 350 RTK or a WingtraOne—the purchase price is only the beginning. Financing these units often involves origination fees, processing charges, and sometimes mandatory tech-support contracts. By looking at the APR, you are seeing all these “hidden” costs bundled into a single, comparable figure.

How APR Differs from Simple Interest in the Drone Sector

Simple interest is calculated solely on the principal amount of the loan. However, very few tech loans are that straightforward. For instance, if a lender offers a 5% interest rate on a $50,000 drone fleet but charges a $2,000 “tech inspection and setup fee” upfront, your actual cost of borrowing is much higher than 5%. The APR calculation takes that $2,000 and spreads it across the life of the loan, giving you a real-world percentage that might look more like 7.5%. Understanding this distinction prevents “sticker shock” when the monthly payments don’t seem to align with the advertised interest rate.

Factors That Influence Your Drone Financing Rates

In the world of tech and innovation, risk is a constant variable. Lenders view drone technology differently than they view traditional assets like real estate or automobiles. Because drones are high-risk assets—prone to crashes, rapid obsolescence, and regulatory shifts—the APR offered to a business is often a reflection of the perceived risk of the technology itself.

Creditworthiness and Business History in Tech Markets

Just as with a car loan, your business credit score is a primary driver of your APR. However, in the drone industry, lenders also look at the “use case.” A startup focusing on speculative R&D might face a higher APR than an established construction firm using drones for routine site inspections. Lenders want to see a clear path to ROI (Return on Investment) because the drone itself is a depreciating asset. A higher credit score signals to the lender that even if the technology fails or becomes obsolete, the borrower has the financial integrity to fulfill the obligation.

The Impact of Rapid Tech Depreciation on Loan Terms

One of the most significant challenges in drone innovation is the speed of progress. A drone purchased today might be surpassed by a more efficient, autonomous model in 24 months. This rapid depreciation affects the “residual value” of the equipment. Because drones lose value faster than cars or heavy machinery, lenders may charge a higher APR to offset the risk that the collateral (the drone) might be worth very little if they have to repossess it halfway through the loan term. Understanding this helps drone operators decide whether to opt for shorter-term financing with higher APRs or longer-term leases that might offer more flexibility.

Evaluating Manufacturer Financing vs. Traditional Tech Lenders

As the drone industry has matured, various financing ecosystems have emerged. Choosing between manufacturer-backed financing and independent tech lenders can significantly impact the APR and the overall health of your business’s cash flow.

Manufacturer-Backed Financing Programs

Companies like DJI and Autel often partner with financial institutions to offer “promotional APRs.” These are frequently lower than market rates—sometimes as low as 0% for the first 12 months—designed to encourage the adoption of their latest tech platforms. While these low APRs are attractive, it is vital to read the fine print. Often, these deals require a large down payment or are only available for specific, high-margin enterprise bundles. The “innovation” here isn’t just in the hardware, but in how the manufacturers lower the barrier to entry for their ecosystems.

Third-Party Lenders and Equipment Leasing

For firms that require a mix of brands—perhaps a fleet comprising Skydio drones for autonomous indoor flight and Parrot drones for thermal mapping—third-party lenders are more common. These lenders specialize in “equipment financing.” The APR might be slightly higher than a manufacturer’s promotional rate, but they offer more flexibility in terms of bundling software subscriptions, extra batteries, and ground control stations into a single loan. In this scenario, the APR serves as the benchmark to determine if the convenience of a single loan is worth the potentially higher cost of capital.

Hidden Costs: Insurance and Software Subscriptions

In the tech and innovation niche, a drone is rarely a standalone product. It requires a suite of software (SaaS) for data processing and a robust insurance policy (Hull and Liability). Some financing packages include these costs in the loan principal. While this increases the total amount borrowed, it can sometimes lower the APR if the lender views the inclusion of insurance as a risk-reduction measure. When evaluating an APR, always ask if it accounts for the “all-in” cost of the technology ecosystem or just the carbon fiber and motors.

Strategic Implications: How APR Affects Fleet Scaling and R&D

For a drone-based enterprise, the APR you accept today dictates your ability to innovate tomorrow. Financial overhead is one of the leading reasons tech startups fail, and miscalculating the cost of debt can lead to “tech debt” that hampers future growth.

Calculating the Total Cost of Ownership (TCO)

Strategic drone operators use APR to calculate the Total Cost of Ownership. If you are choosing between two drone platforms—one that costs $20,000 at a 4% APR and another that costs $18,000 at an 8% APR—the cheaper drone might actually be more expensive over a three-year term. By using the APR to project the TCO, businesses can make data-driven decisions about which technology provides the best value per flight hour. This is the same logic used in large-scale logistics and automotive fleet management, applied to the high-stakes world of UAVs.

Leveraging APR to Maintain Cash Flow for Innovation

In the tech sector, cash is king. Even if a company has the liquid assets to buy a $100,000 drone fleet outright, they might choose to finance it if the APR is low enough. If you can borrow at a 5% APR but your internal R&D projects yield a 15% return, it makes more sense to finance the equipment and keep your cash working on innovation. Understanding APR allows drone entrepreneurs to play this “spread,” using low-cost debt to fuel high-growth technological advancements.

Conclusion: The Financial Foundation of Flight

The question “what does APR mean when buying a car” is a gateway to understanding the broader economics of asset acquisition. In the drone industry, where innovation moves at the speed of flight, APR is the metric that bridges the gap between a visionary idea and a scalable reality. By mastering the factors that influence APR—from creditworthiness to tech depreciation—and by comparing the true costs of manufacturer vs. third-party financing, drone professionals can ensure their tech stack is built on a solid financial foundation. In the end, the most advanced obstacle avoidance system or the highest-resolution thermal camera is only as valuable as the financial strategy that put it in the air. Professional-grade innovation requires professional-grade financing, and that begins with a deep, nuanced understanding of APR.