When navigating the complexities of homeownership, understanding the various components of a mortgage payment is crucial. Among these, the concept of “escrow” often arises, particularly regarding how your property taxes and homeowner’s insurance are managed. Escrow, in the context of a mortgage, is a system designed to simplify and ensure timely payment of these essential property-related expenses by pooling funds from your monthly mortgage payment.

Understanding the Basics of Escrow

At its core, an escrow account is a special type of bank account held by your mortgage lender, or a third-party escrow company, on your behalf. This account serves as a holding place for funds specifically designated for your property taxes and homeowner’s insurance premiums. Each month, a portion of your total mortgage payment is allocated to this escrow account. When these bills become due, the lender or escrow company uses the accumulated funds to pay them directly.

The Components of Your Monthly Mortgage Payment

A standard monthly mortgage payment is typically divided into two main parts:

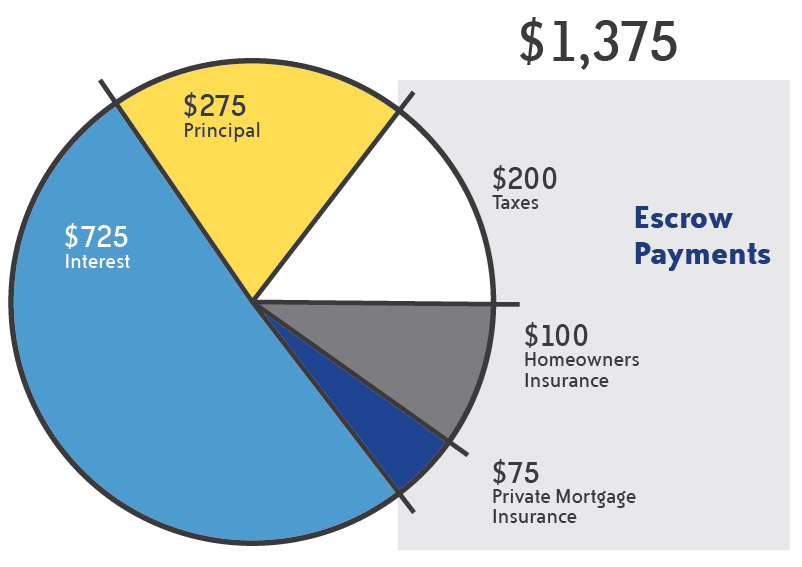

- Principal and Interest (P&I): This is the portion that goes towards paying down the actual loan amount (principal) and the interest charged by the lender for borrowing the money. This is a fixed amount throughout the life of a fixed-rate mortgage.

- Escrow Payment: This is the part of your payment that covers your property taxes and homeowner’s insurance. This amount can fluctuate annually based on changes in tax assessments and insurance premiums.

When you obtain a mortgage, particularly for a home purchase, lenders almost always require you to establish an escrow account. This requirement is primarily to protect their investment. If property taxes go unpaid, the local government can place a lien on your property, potentially forcing a sale. Similarly, if your homeowner’s insurance lapses, a disaster like a fire or flood could devastate the property, leaving the lender with little recourse to recover their loan amount. By managing these payments through escrow, lenders ensure these critical obligations are met.

Who Manages the Escrow Account?

In most cases, your mortgage lender will act as the servicer of your escrow account. They collect the funds from you and then disburse them to the relevant authorities (tax assessor’s office, insurance company) when payments are due. In some instances, a separate third-party escrow company might be hired by the lender to manage these accounts. Regardless of who manages it, the principle remains the same: your money is held securely and used for its intended purpose.

How Escrow Funds Are Calculated and Managed

The amount you contribute to your escrow account each month is not arbitrary. It’s carefully calculated to ensure that sufficient funds are available when your tax and insurance bills are due.

Initial Escrow Deposit

When you close on your mortgage, you will typically be required to make an initial deposit into the escrow account. This deposit is often calculated to cover a few months of anticipated tax and insurance payments, plus a cushion. This ensures that even if the first payments are due shortly after closing, there are funds readily available.

Monthly Escrow Contributions

The ongoing monthly contribution to your escrow account is determined by dividing your estimated annual property taxes and homeowner’s insurance premiums by 12. For example, if your annual property taxes are $3,600 and your annual homeowner’s insurance is $1,200, your total annual escrow expense is $4,800. This would translate to a monthly escrow contribution of $400 ($4,800 / 12).

The Escrow Cushion

Lenders are generally permitted to hold a certain amount of extra funds in your escrow account as a “cushion.” This cushion acts as a buffer to absorb unexpected increases in property taxes or insurance premiums. Federal law (the Real Estate Settlement Procedures Act, or RESPA) limits this cushion to the equivalent of two months of your estimated escrow payments. So, in the example above, the lender could hold up to $800 (two months of $400) as a cushion. This means your total escrow balance could be higher than just the amount needed for the next immediate payment.

Annual Escrow Analysis

A crucial part of the escrow process is the annual escrow analysis. At least once a year, your mortgage lender or servicer is required to review your escrow account. This analysis involves:

- Reviewing Actual Payments: Checking the actual amounts paid for property taxes and homeowner’s insurance during the past year.

- Estimating Future Payments: Projecting the costs for the upcoming year, taking into account any known or anticipated increases in tax rates or insurance premiums.

- Reconciling the Balance: Comparing the projected future payments against the current balance in your escrow account.

Based on this analysis, your monthly escrow payment may be adjusted.

- If your escrow account is projected to have a deficit: Meaning, the funds in the account are not expected to be enough to cover the upcoming bills, your monthly escrow payment will be increased to make up the difference. This increase will be spread out over the remaining months until the next analysis.

- If your escrow account is projected to have a surplus: Meaning, there are more funds in the account than needed to cover upcoming bills, your monthly escrow payment may be decreased.

- If your escrow account has a surplus exceeding the legal cushion limit: The lender is typically required to refund this excess amount to you. This usually happens after the annual analysis.

You will receive an escrow statement detailing this analysis, including your current balance, payments made, projected disbursements, and any adjustments to your monthly payment.

Benefits of Using an Escrow Account

While the idea of an escrow account might seem like an added complexity or expense, it offers several significant benefits to homeowners:

Convenience and Peace of Mind

The primary benefit of an escrow account is the convenience it provides. Instead of manually tracking multiple due dates for property taxes and homeowner’s insurance, and then remembering to make those payments, the entire process is automated. This frees you from the mental burden of managing these separate financial obligations, offering peace of mind that these essential payments are being handled consistently and on time.

Avoidance of Late Fees and Penalties

Property taxes and homeowner’s insurance premiums have strict due dates. Missing these deadlines can result in substantial late fees, penalties, and even the cancellation of your insurance policy, which could have dire financial consequences. By having these payments automatically handled through escrow, you significantly reduce the risk of incurring such penalties.

Protection Against Default and Foreclosure

As mentioned earlier, unpaid property taxes can lead to a lien on your property and potentially foreclosure. Similarly, a lapse in homeowner’s insurance leaves your property vulnerable to damage without coverage, jeopardizing your investment. The escrow system ensures these obligations are met, thus protecting you from these severe risks and safeguarding your home.

Stability in Budgeting (to a degree)

While your total mortgage payment can fluctuate due to changes in escrow, the P&I portion of a fixed-rate mortgage remains constant. The escrow component, while variable, is managed and adjusted on an annual basis, providing a predictable framework for these expenses. This allows for more stable long-term financial planning compared to managing these large, infrequent payments entirely on your own.

When Escrow Might Not Be Required

In certain situations, mortgage lenders may not require an escrow account. This is typically based on the borrower’s demonstrated financial responsibility and the amount of equity they have in their home.

Escrow Waivers

Some lenders offer an “escrow waiver” or “impound waiver” under specific conditions. These conditions often include:

- High Credit Score: Borrowers with excellent credit ratings may be considered for an escrow waiver.

- Significant Equity: Having a substantial amount of equity in the home (e.g., 20% or more down payment, or a loan-to-value ratio below a certain threshold) can also lead to an escrow waiver.

- Established Payment History: For existing homeowners refinancing their mortgage, a proven track record of timely payments might be sufficient.

If an escrow waiver is granted, you will be responsible for paying your property taxes and homeowner’s insurance premiums directly. You will likely need to provide proof of payment to your lender on a regular basis.

Risks of Waiving Escrow

While waiving escrow can simplify your monthly payment by reducing it, it also places the full responsibility for timely payments directly on you. This means you must be diligent in managing due dates, ensuring funds are available, and keeping records of payments. Failure to do so can still lead to the same negative consequences as if you had an escrow account that was mismanaged. For many, the convenience and built-in protection of an escrow account outweigh the perceived benefits of a waiver.

Conclusion: The Role of Escrow in Homeownership

In summary, an escrow account is an integral part of the mortgage process for most homeowners. It acts as a vital intermediary, ensuring that your property taxes and homeowner’s insurance premiums are paid on time and in full. While it adds a component to your monthly mortgage payment, its purpose is to safeguard your investment, prevent costly penalties, and provide a streamlined approach to managing these significant homeownership expenses. Understanding how your escrow account works, how it’s calculated, and how it’s analyzed annually empowers you to be a more informed and financially secure homeowner.