In the realm of personal finance and employment, the W-2 form stands as a critical document, detailing an individual’s annual wages and the taxes withheld by their employer. While most individuals are familiar with the standard boxes on this form, such as wages earned and federal income tax withheld, certain boxes, particularly Box 12, can present a more complex landscape. Box 12 is a versatile section used by employers to report various types of compensation and benefits that may be subject to or exempt from federal income tax, social security tax, or Medicare tax. Among the numerous codes that can appear in Box 12, the code “DD” holds specific significance, particularly for employees participating in employer-sponsored health coverage. Understanding the implications of “DD” is crucial for accurate tax filing and for comprehending the value of the benefits received.

This section of the W-2 form is designed to accommodate a wide array of specific compensation and benefit details that don’t fit into the more general categories. Employers utilize a system of letter codes, ranging from A to HH, to denote the nature of the payments or benefits being reported. These codes help the IRS and the taxpayer distinguish between different types of income and withholding, ensuring proper tax treatment. For instance, codes might relate to retirement plan contributions, dependent care benefits, educational assistance, or, as in the case of “DD,” the cost of group health coverage. The inclusion of “DD” specifically addresses the Affordable Care Act’s (ACA) reporting requirements, aiming to provide transparency about the value of employer-provided health insurance.

Understanding Code DD: The Cost of Employer-Sponsored Health Coverage

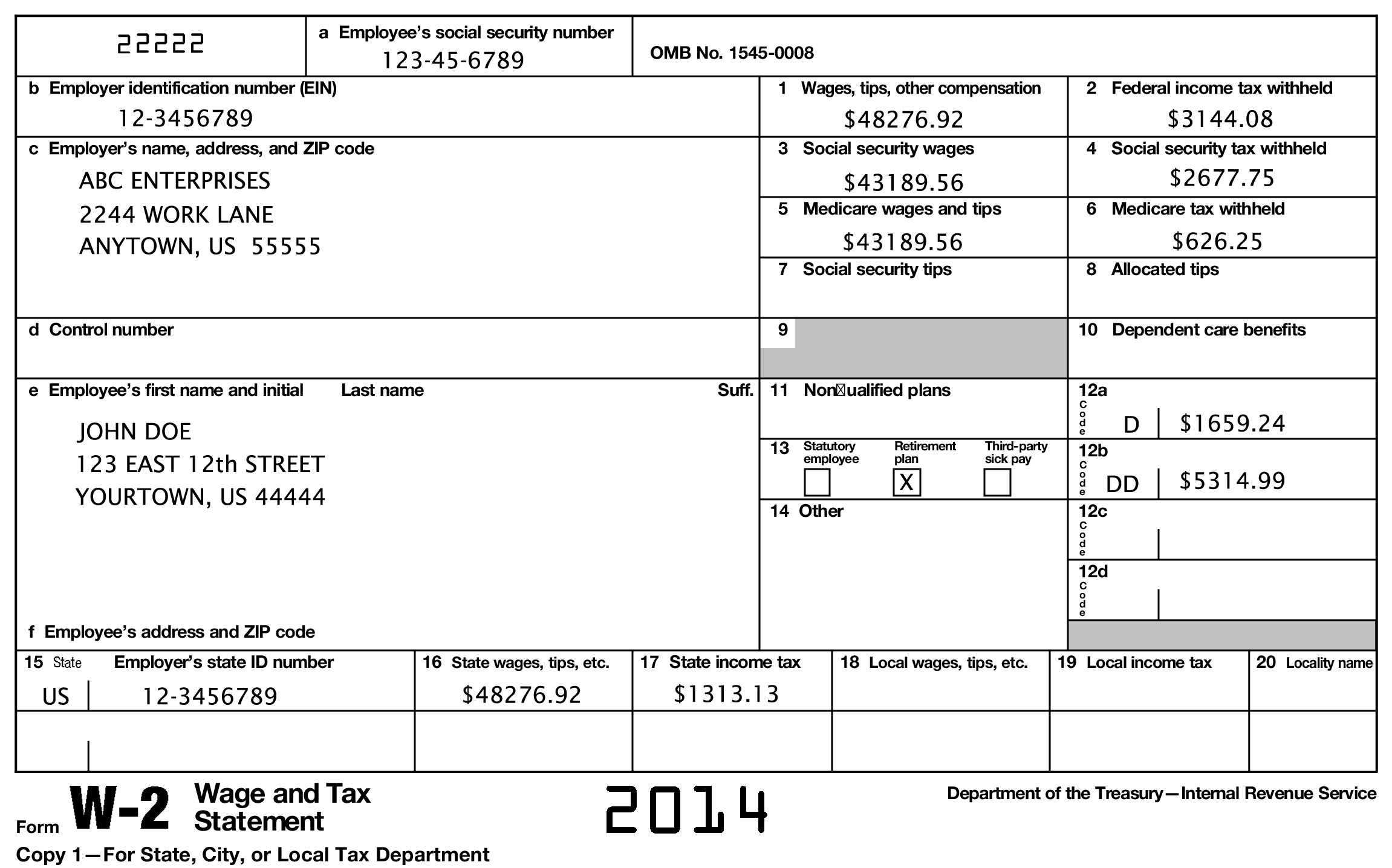

Code “DD” on a W-2 form signifies the aggregate cost of employer-sponsored health coverage. This amount includes the portion paid by the employer and any portion paid by the employee through pre-tax deductions. It’s important to note that the amount reported under code DD is for informational purposes only. It is generally not taxable income. The purpose of this reporting is to provide employees with a clearer picture of the significant benefit their employer provides in the form of health insurance. For many employees, the value of this coverage can be substantial, and seeing it explicitly stated on their W-2 can highlight the total compensation package they receive, which often extends beyond their base salary.

What Constitutes “Employer-Sponsored Health Coverage”?

Employer-sponsored health coverage encompasses a range of plans and benefits provided by an employer to its employees and their dependents. This typically includes:

- Medical Insurance: This is the most common form of employer-provided health coverage, covering doctor visits, hospital stays, prescription drugs, and other medical services.

- Dental Insurance: Many employers offer separate dental plans to cover routine check-ups, cleanings, fillings, and more complex procedures.

- Vision Insurance: This type of coverage typically helps pay for eye exams, eyeglasses, and contact lenses.

- Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs): While the contributions themselves might be reported under different codes, the employer’s contributions to these accounts, which are used to pay for qualified medical expenses, are often factored into the total cost of health coverage reported under DD.

- Health Reimbursement Arrangements (HRAs): Similar to HSAs and FSAs, employer contributions to HRAs are part of the overall health benefit.

The specific components included in the “DD” code can vary slightly depending on the employer’s benefit offerings and how they administer their health plans. However, the core principle remains consistent: it represents the total value of the health insurance benefits provided to the employee.

The Employer’s Responsibility in Reporting DD

Employers are mandated by the IRS to report the cost of applicable employer-sponsored health coverage under Box 12 with the code “DD” for employees enrolled in such plans. This reporting requirement was introduced as part of the Affordable Care Act (ACA) to offer transparency and to help employees understand the value of their health benefits. The calculation of this amount involves summing up all employer and employee contributions towards the health coverage for the tax year. This includes premiums paid by the employer, premiums paid by the employee through payroll deductions (both pre-tax and post-tax), and any employer contributions to HSAs, FSAs, or HRAs that are specifically tied to the health plan.

The employer must determine the “applicable employer cost” for the year. This calculation generally involves:

- Employer Portion of Premiums: The amount the employer pays directly for the employee’s health insurance premiums.

- Employee Portion of Premiums: The amount the employee pays for health insurance premiums, usually deducted from their paycheck. If these deductions are made on a pre-tax basis, they are still included in the total cost reported under DD.

- Employer Contributions to HSAs/FSAs/HRAs: Any funds contributed by the employer to these health spending accounts that are linked to the health plan.

It’s crucial for employers to have accurate record-keeping systems to properly calculate and report this figure. Errors in reporting can lead to confusion for employees and potential issues with tax authorities.

Why is Code DD Included on Your W-2?

The primary reason for the inclusion of code “DD” on your W-2 is to provide you with a clear understanding of the financial value of the health insurance benefits your employer provides. This figure serves as an important piece of information for several reasons:

Informational Purposes and Benefit Valuation

The amount reported under “DD” is intended to be purely informational. It is not added to your taxable income, meaning you do not pay federal income tax on this amount. However, it gives you a tangible representation of a significant component of your total compensation package. For instance, if your annual salary appears to be $60,000, but your employer-sponsored health coverage is valued at $15,000 annually, your true total compensation is closer to $75,000. This insight is invaluable when evaluating job offers, negotiating salaries, or simply understanding the full scope of your employment benefits. It helps you appreciate the cost savings you realize by having health insurance provided by your employer, as obtaining similar coverage independently could be significantly more expensive.

Understanding the Affordable Care Act (ACA)

The reporting of code “DD” is a direct result of the Affordable Care Act (ACA). The ACA aims to expand health insurance coverage and improve its affordability. By requiring employers to report the cost of health coverage, the government seeks to:

- Increase Transparency: Employees gain a better understanding of the value of employer-provided health benefits, which can influence their decisions about choosing health plans and understanding their overall financial well-being.

- Provide Data for Policy Analysis: The aggregated data from these reports can help policymakers assess the effectiveness of the ACA and identify areas for future improvements or adjustments to health insurance regulations.

- Inform Future Benefit Decisions: Employees can use this information when considering future career moves or assessing their current employment situation. Knowing the market value of their health benefits can be a significant factor in these decisions.

While “DD” is not taxable, understanding its implications can empower employees to make more informed financial and career choices. It underscores the substantial investment employers make in their workforce’s health and well-being.

Impact on Tax Filing

As previously mentioned, the amount reported in Box 12, code DD, is generally not considered taxable income. This means you do not need to add this figure to your gross income when calculating your federal income tax liability. The IRS explicitly states that this information is for reporting purposes only.

However, it’s essential to be aware of this distinction. Some other codes in Box 12 might relate to pre-tax contributions that reduce your taxable income (e.g., contributions to a 401(k) plan, code D). In contrast, code DD reflects the total cost of coverage, which is a benefit you receive but do not directly pay income tax on. This is because premiums for employer-sponsored health insurance are often paid with pre-tax dollars, effectively reducing your taxable income before the “DD” amount is even calculated.

Therefore, when you file your taxes, you will typically use your W-2 to report your wages (Box 1), federal income tax withheld (Box 2), and other relevant income and withholding information. The “DD” amount in Box 12 will not directly affect your tax liability. It’s more of a statement of benefit value.

What if You Don’t See Code DD on Your W-2?

Not seeing code “DD” on your W-2 form can occur for several reasons, and it’s important to understand why this might be the case:

Not Enrolled in Employer-Sponsored Health Coverage

The most straightforward reason for not having a “DD” code on your W-2 is that you are not enrolled in an employer-sponsored health plan. If you have chosen not to participate in your employer’s health insurance offerings, or if your employer does not offer such benefits, then there is no cost of coverage to report. This could also happen if you are covered by a spouse’s employer plan, or if you obtain health insurance through a government marketplace like HealthCare.gov. In these scenarios, your employer would have no health coverage costs to report for you.

Employer Size and ACA Reporting Thresholds

The ACA’s reporting requirements for employer-sponsored health coverage (including the “DD” code) primarily apply to “applicable large employers” (ALEs). An ALE is generally defined as an employer with 50 or more full-time employees, including full-time equivalent employees, during the preceding calendar year. Smaller employers (those with fewer than 50 full-time employees) are not subject to the same mandatory reporting requirements for the cost of health coverage under Box 12, code DD. If your employer falls below this threshold, they are not required to report this information on your W-2.

Specific Benefit Plans or Employer Policies

In some rare instances, certain types of health-related benefits, or the way an employer administers them, might not fall under the definition of “applicable employer-sponsored health coverage” for the purpose of the “DD” code reporting. This is less common, as the intent of the ACA is to capture the primary health insurance benefits. However, if you have questions about your specific benefit package and why “DD” might be absent, it’s always best to consult with your employer’s HR department. They can clarify the specifics of your benefits and the reporting practices.

Errors in Reporting

While less frequent, it is possible that there could be an error in the W-2 preparation by your employer. If you are certain that you were enrolled in employer-sponsored health coverage and believe the “DD” code should have been present, you should reach out to your employer’s payroll or HR department to inquire about the discrepancy. They can review your W-2 and make any necessary corrections.

Key Takeaways and Final Considerations

The “DD” code in Box 12 of your W-2 form serves a vital informational purpose, representing the total cost of your employer-sponsored health coverage. It is a reflection of the significant benefit your employer provides, contributing substantially to your overall compensation package, even though this amount is generally not subject to income tax. Understanding this code empowers you to better assess your total compensation, appreciate the value of your employee benefits, and gain insight into the broader implications of the Affordable Care Act.

It’s crucial to remember that the “DD” amount is for informational purposes and does not directly impact your taxable income calculation. If you have any doubts or questions regarding the “DD” code on your W-2, or any other aspect of your tax forms, consulting with a qualified tax professional or referring to official IRS publications is always recommended. Accurate comprehension of your W-2 ensures compliant and confident tax filing.