Understanding the intricacies of sales tax is a crucial aspect of conducting business in Arizona. Whether you are a seasoned entrepreneur or just embarking on your entrepreneurial journey, a clear grasp of Arizona’s sales tax regulations can prevent costly missteps and ensure compliance. This guide delves into the fundamental principles of AZ sales tax, covering its definition, application, rates, and the responsibilities of businesses operating within the Grand Canyon State.

The Fundamentals of Arizona Sales Tax

Arizona operates on a Transaction Privilege Tax (TPT) system, which is often colloquially referred to as sales tax. However, it’s important to distinguish TPT from a traditional retail sales tax. In a retail sales tax model, the tax is levied on the final consumer. In Arizona’s TPT system, the tax is technically imposed on the seller for the privilege of doing business in the state. This means that while the seller is responsible for remitting the tax, the ultimate burden of the tax typically falls on the consumer through the price of goods and services.

Key Characteristics of Arizona TPT

- Seller Imposed: The tax is placed upon the seller for the privilege of engaging in business within Arizona.

- Broad Application: TPT applies to a wide range of business activities, including the sale of tangible personal property, the provision of certain services, and the rental or lease of property.

- Jurisdictional Variations: A significant aspect of Arizona TPT is that tax rates and rules can vary not only by county but also by city and even by special taxing districts within a city. This means that a business might be subject to multiple TPT rates depending on its physical location and the location of its customers.

- Prime Contracting: For businesses involved in construction, Arizona has specific rules for “prime contracting.” This involves the tax treatment of materials purchased by a contractor for use in a construction project. The tax liability often depends on whether the project is considered “fixed for realty” (attached to the land) or personal property.

Who is Liable for AZ TPT?

Any person or business engaging in business in Arizona that is subject to TPT is liable for collecting and remitting the tax. This includes:

- Retailers: Businesses selling tangible personal property to consumers.

- Wholesalers: In some cases, wholesalers may also be subject to TPT depending on the specific nature of their sales.

- Service Providers: Businesses offering services subject to TPT, such as repair services, cleaning services, or commercial rental services.

- Contractors: As mentioned, prime contractors and subcontractors have specific TPT obligations related to construction projects.

- Manufacturers: Manufacturers are generally subject to TPT on their sales, although there may be exemptions or deductions for certain manufacturing activities or sales for resale.

It is crucial for businesses to determine if their activities fall under the purview of Arizona’s TPT laws. The Arizona Department of Revenue (AZDOR) provides extensive resources and guidance on these classifications.

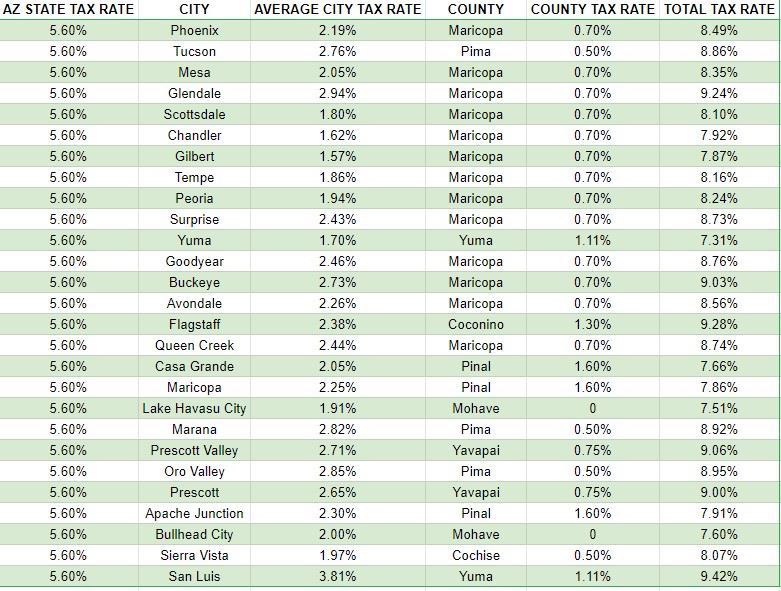

Navigating AZ Sales Tax Rates

The complexity of AZ sales tax rates is a significant challenge for many businesses. Unlike states with a single statewide sales tax rate, Arizona’s TPT rates are a composite of several layers, leading to a multi-faceted tax structure.

Components of AZ TPT Rates

- State TPT Rate: This is the base rate applied across the state.

- County TPT Rate: Each county in Arizona can impose its own TPT rate.

- City TPT Rate: Cities within counties can also levy their own TPT rates, which can vary significantly from one city to another.

- Special Taxing Districts: In some areas, special taxing districts, such as transit districts or public safety districts, may also impose TPT.

The combined TPT rate for a specific transaction is the sum of all applicable state, county, city, and special taxing district rates at the point of sale or delivery.

Determining the Applicable Rate

The primary factor in determining the correct TPT rate is the location of the sale. Arizona generally uses a destination-based sourcing rule for the sale of tangible personal property. This means that the tax rate applied is the rate in effect at the location where the customer takes possession of the property. For services, the sourcing rule can be more complex and often depends on where the service is performed or where the benefit of the service is received.

Examples:

- If a business located in Phoenix sells a product to a customer in Scottsdale, and the customer picks up the product in Phoenix, the TPT rate for Phoenix would apply.

- If the same business in Phoenix sells a product to a customer in Scottsdale, and the business delivers the product to the customer’s address in Scottsdale, the combined TPT rate for Scottsdale (including any relevant county and special taxing district rates) would apply.

This destination-based sourcing rule necessitates that businesses have robust systems in place to accurately calculate and collect TPT based on the delivery address or the location where the service is rendered.

The Arizona Transaction Privilege Tax Rate Schedules

The AZDOR publishes detailed TPT rate schedules that are updated periodically. These schedules are essential for businesses to accurately determine the correct tax rate for any given location within the state. Navigating these schedules can be daunting due to the numerous jurisdictions and their specific rates. Many businesses utilize specialized tax software or consult with tax professionals to ensure accuracy.

Registration, Reporting, and Remittance

Compliance with Arizona’s TPT laws involves several key steps: registering with the AZDOR, accurately reporting taxable transactions, and timely remitting the collected taxes.

Business Registration

Before engaging in any business activity subject to TPT in Arizona, businesses must register with the Arizona Department of Revenue. This is typically done online through the AZTaxes.gov portal. Upon registration, businesses are issued an Arizona Transaction Privilege Tax (TPT) license number. This number is essential for all TPT-related filings and communications with the AZDOR.

Filing TPT Returns

Arizona TPT returns are typically filed on a monthly basis. However, depending on the business’s tax liability, the AZDOR may assign them to a different filing frequency, such as quarterly or annually. Returns are filed electronically through the AZTaxes.gov portal.

Key information required for TPT returns includes:

- Gross Sales: The total amount of sales made during the reporting period.

- Deductions and Exemptions: Specific sales that are not subject to TPT (e.g., sales for resale, sales to government entities, or certain exempt services). Properly documenting and claiming these deductions is critical.

- Taxable Sales: The portion of gross sales that are subject to TPT.

- TPT Due: The calculated amount of tax owed based on the applicable rates and taxable sales.

Remitting TPT

Once the TPT return is filed, the calculated tax amount must be remitted to the AZDOR. Payments are also typically made electronically through the AZTaxes.gov portal. Timely remittance is crucial to avoid penalties and interest. The due date for TPT returns and payments is generally the 20th day of the month following the close of the reporting period. For example, January’s TPT liability is typically due on February 20th.

Common TPT Exemptions and Deductions in Arizona

While Arizona’s TPT system is broad, there are several recognized exemptions and deductions that businesses can utilize to reduce their tax liability. Understanding and properly applying these can lead to significant tax savings.

Sales for Resale

One of the most common deductions is for sales made for resale. If a business purchases goods and intends to resell them to another business or consumer, the initial purchase is generally not subject to TPT. The subsequent sale by the reseller will then be subject to TPT. Businesses claiming this deduction must obtain a valid resale certificate from their customer.

Manufacturing and Research & Development

Arizona provides incentives for manufacturing and research and development activities. Certain purchases of machinery, equipment, and materials used directly in manufacturing or R&D processes may be exempt from TPT. These exemptions are often subject to strict definitions and requirements.

Sales to Government Entities

Sales made to the U.S. Government or the State of Arizona and its political subdivisions are often exempt from TPT. Again, proper documentation, such as a government exemption certificate, is usually required.

Food for Home Consumption

Prepared food intended for home consumption is generally not subject to TPT. However, this exemption typically does not apply to food sold in restaurants or similar establishments for immediate consumption on the premises.

Services

Certain services are exempt from TPT. For example, basic cable television services, certain types of insurance premiums, and professional services like legal or medical services may be exempt. The specific services that are subject to or exempt from TPT can be found in Arizona statutes and AZDOR publications.

Prime Contracting Exemptions

For prime contractors, there are specific rules and potential exemptions related to the purchase of materials used in construction. For instance, materials purchased by a prime contractor for use in constructing, altering, or improving real property for the federal government or the state and its political subdivisions are generally exempt.

It is imperative for businesses to consult the official Arizona Department of Revenue guidance and relevant statutes to ensure they are correctly applying any exemptions or deductions. Misapplication can lead to significant tax liabilities, penalties, and interest.

Staying Compliant in a Dynamic Tax Environment

Arizona’s TPT landscape is dynamic, with tax laws and rates subject to change. Staying informed and proactive is essential for maintaining compliance and optimizing tax strategies.

Resources for Businesses

The Arizona Department of Revenue (AZDOR) is the primary resource for all TPT-related information. Their website (azdor.gov) offers a wealth of resources, including:

- TPT Rate Tables: Comprehensive lists of TPT rates by jurisdiction.

- Guides and Publications: Detailed explanations of TPT laws, exemptions, and reporting requirements.

- Online Filing and Payment System (AZTaxes.gov): The portal for registration, filing, and remittance.

- FAQs and Contact Information: Answers to common questions and ways to reach AZDOR for assistance.

The Importance of Professional Advice

Given the complexity of Arizona’s TPT system, many businesses find it beneficial to engage with tax professionals, such as CPAs or tax attorneys. These professionals can:

- Provide expert guidance on TPT liabilities and obligations.

- Assist with proper registration and licensing.

- Ensure accurate TPT return preparation and filing.

- Identify potential tax savings through the strategic application of exemptions and deductions.

- Represent businesses in case of audits or disputes with the AZDOR.

By understanding the fundamentals of Arizona sales tax, navigating its intricate rate structure, adhering to registration and reporting requirements, and leveraging available exemptions, businesses can confidently operate within the state and ensure their financial health and legal standing. Proactive engagement with tax compliance is not just a regulatory necessity; it’s a strategic imperative for sustainable business success in Arizona.