Navigating the landscape of healthcare savings can be a complex undertaking. Two of the most prominent tools available to individuals and employers alike are Health Reimbursement Arrangements (HRAs) and Health Savings Accounts (HSAs). While both offer tax advantages for healthcare expenses, their structure, eligibility, and functionality differ significantly. Understanding these distinctions is crucial for making informed decisions about personal health and financial planning, particularly in the context of employer-sponsored benefits. This exploration delves into the core mechanics of HRAs and HSAs, examining their defining characteristics and how they serve distinct purposes in managing healthcare costs.

Understanding Health Reimbursement Arrangements (HRAs)

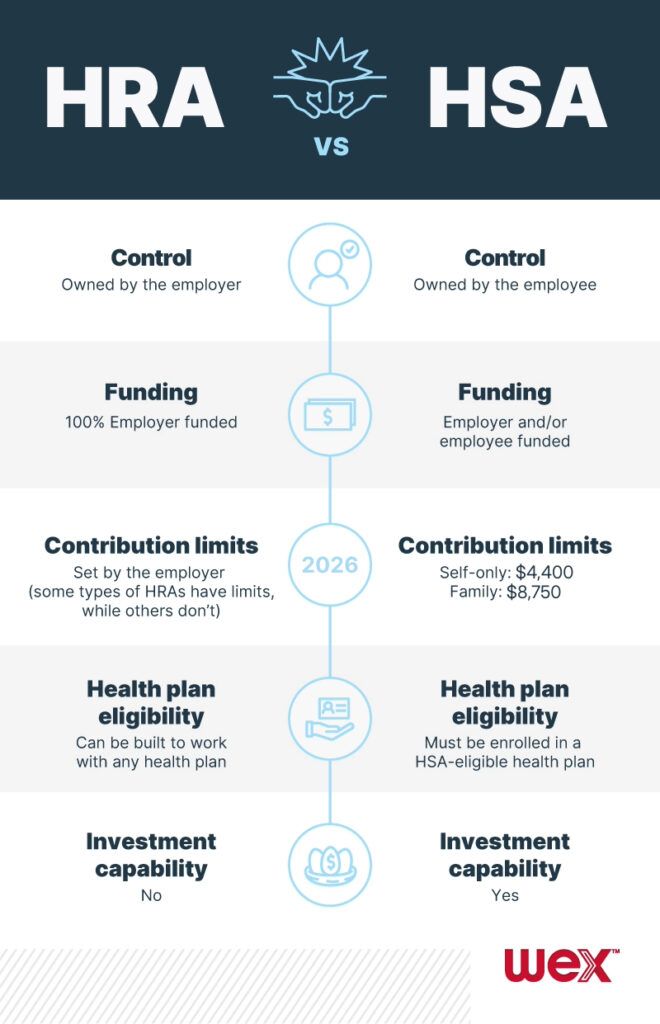

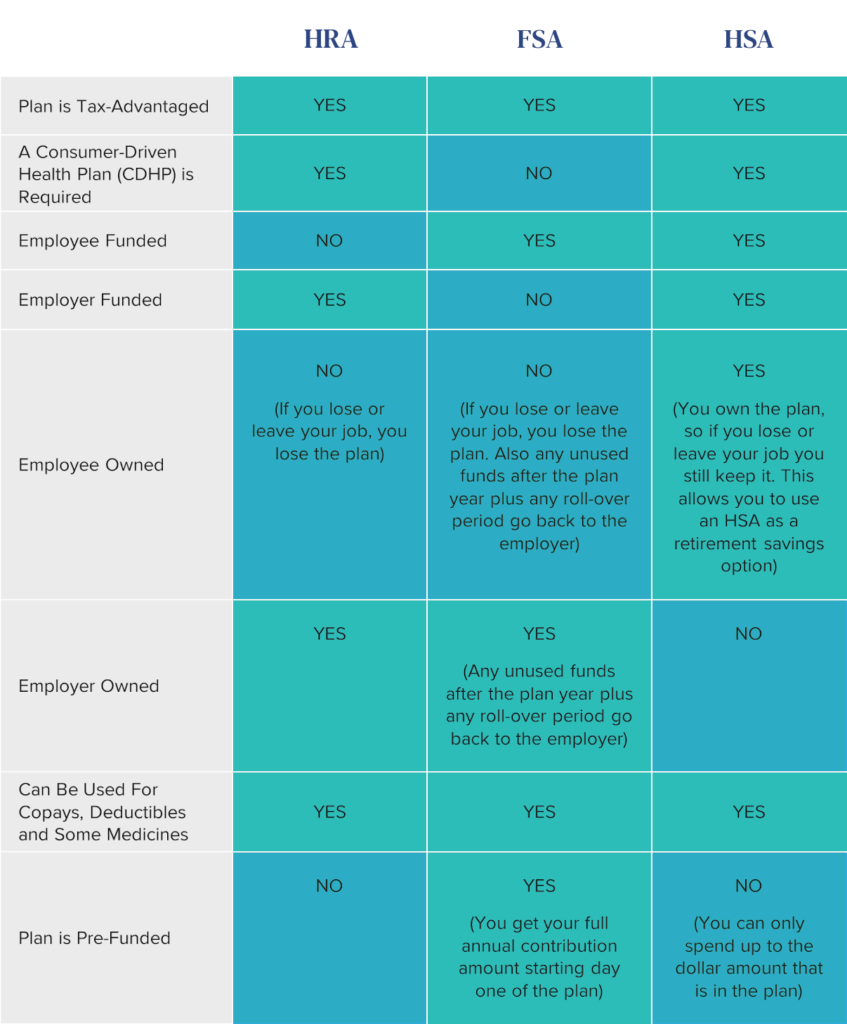

A Health Reimbursement Arrangement (HRA) is an employer-funded health benefit that allows employers to reimburse employees for qualified medical expenses up to a certain dollar amount set by the employer. Unlike HSAs, HRAs are entirely funded and controlled by the employer. This means employees do not contribute their own money to an HRA, nor do they own the account. The funds within an HRA are employer assets, and the employer dictates the specific eligible expenses, reimbursement process, and any potential carryover rules.

Key Characteristics of HRAs

The fundamental nature of an HRA is rooted in its employer-centric design. This has several implications for how it operates and who benefits.

Employer Control and Funding

The most defining feature of an HRA is that it is solely funded and administered by the employer. The employer decides how much money will be allocated to the HRA each year, and this amount can vary between different employee groups, though employers must ensure fairness and non-discrimination in their plan design. This allows employers to tailor their health benefits to the specific needs and financial capabilities of their organization. Employers can choose to offer different types of HRAs, such as:

- Traditional HRAs: These offer broad reimbursement for a wide range of medical expenses, often covering deductibles, copayments, and coinsurance.

- Limited HRAs: These are designed to supplement other health insurance plans, typically covering only specific types of expenses like dental or vision care, or to be used after a deductible has been met.

- Post-Deductible HRAs: As the name suggests, these HRAs are designed to reimburse employees for qualified medical expenses only after they have met a certain deductible amount in their primary health insurance plan.

- Integrated HRAs: These are HRAs that are designed to be paired with a High Deductible Health Plan (HDHP). They can reimburse employees for deductibles and other qualified medical expenses.

Employee Eligibility and Access

Eligibility for an HRA is determined by the employer. Typically, only employees are eligible to receive reimbursements from an HRA. However, employers can extend eligibility to the employee’s dependents as well, depending on the plan design. The funds in an HRA are generally accessible through a reimbursement process. Employees incur a medical expense, pay for it out-of-pocket, and then submit a claim to their employer with supporting documentation (e.g., receipts, Explanation of Benefits). The employer then reimburses the employee from the HRA funds, subject to the plan’s rules.

Tax Advantages

HRAs offer significant tax advantages. The employer contributions to an HRA are tax-deductible business expenses, reducing the employer’s taxable income. For the employee, reimbursements received from an HRA for qualified medical expenses are not considered taxable income. This means employees can use the funds for healthcare without incurring any income tax liability on the reimbursed amount.

Fund Carryover and Portability

The rules surrounding fund carryover in an HRA are determined by the employer. Some HRAs allow employees to carry over unused funds to the next plan year, often with a limit on the amount that can be carried over. This can be a valuable benefit for employees who anticipate higher medical expenses in the future. However, HRAs are generally not portable. If an employee leaves the company, they typically forfeit any remaining HRA funds. The funds belong to the employer, and their continued availability is tied to current employment status.

Understanding Health Savings Accounts (HSAs)

A Health Savings Account (HSA) is a tax-advantaged savings account that allows individuals to set aside money for qualified medical expenses. Unlike HRAs, HSAs can be funded by the individual, their employer, or both. The key distinguishing feature of an HSA is that the account holder owns the funds, and these funds remain with the individual regardless of employment status. HSAs are specifically designed to be paired with High Deductible Health Plans (HDHPs).

Key Characteristics of HSAs

The ownership, funding, and flexibility of HSAs set them apart as a powerful tool for long-term health savings.

Individual Ownership and Control

The most significant differentiator for HSAs is individual ownership. The account holder, not the employer, owns the HSA. This ownership provides a high degree of control over the funds. The individual decides how much to contribute (within IRS limits), how to invest the funds, and when to use them for qualified medical expenses. This personal ownership fosters a sense of financial responsibility and empowerment when it comes to healthcare planning.

Triple Tax Advantage

HSAs are renowned for their “triple tax advantage”:

- Tax-Deductible Contributions: Contributions made by the individual or employer are tax-deductible, reducing the taxable income for the year.

- Tax-Free Growth: Any earnings on the funds within the HSA (if invested) grow tax-free.

- Tax-Free Withdrawals: Withdrawals made for qualified medical expenses are completely tax-free.

This triple tax advantage makes HSAs an exceptionally effective savings vehicle for healthcare expenses, offering substantial long-term financial benefits.

Eligibility Requirements

To be eligible for an HSA, an individual must be covered by a High Deductible Health Plan (HDHP). An HDHP is defined by the IRS and generally has a higher deductible than traditional health insurance plans. Individuals cannot be enrolled in Medicare, nor can they be claimed as a dependent on someone else’s tax return to be eligible. If an individual has other health coverage that is not an HDHP, they generally cannot contribute to an HSA, with some exceptions (like dental or vision insurance).

Funding Flexibility

HSAs can be funded by the individual, the employer, or a combination of both. Many employers offer HSAs as part of their benefits package, contributing to the employee’s HSA, often as an incentive to enroll in an HDHP. Individuals can also make their own contributions, up to annual IRS limits. These limits are set by the IRS and vary annually, with higher limits for individuals over age 55 who can make additional “catch-up” contributions.

Portability and Investment Options

A major advantage of HSAs is their portability. The funds in an HSA belong to the individual and remain with them even if they change employers, lose their job, or retire. This makes HSAs a valuable long-term savings tool, not tied to a specific employer. Furthermore, many HSA providers offer investment options, allowing account holders to grow their savings over time. This investment potential can transform an HSA from a simple savings account into a significant retirement asset, especially for those who use it primarily for long-term healthcare needs in retirement.

HRA vs. HSA: Key Differences Summarized

The fundamental distinctions between HRAs and HSAs revolve around ownership, funding, eligibility, and portability. Understanding these core differences is paramount for individuals and employers seeking to optimize their healthcare spending and savings strategies.

Ownership and Control

The most significant divergence lies in who owns and controls the funds. With an HRA, the employer owns and controls the funds. The employee is a beneficiary of the employer’s generosity and plan design. Conversely, an HSA is owned by the individual. This personal ownership empowers the individual with direct control over their contributions, investments, and spending decisions within the account’s framework.

Funding Sources

HRAs are exclusively funded by employers. The employer determines the contribution amount and frequency. HSAs, on the other hand, can be funded by the individual, the employer, or both. This dual funding capability offers greater flexibility, allowing individuals to supplement employer contributions and take full advantage of tax-deductible savings.

Eligibility

Eligibility for an HRA is determined by the employer’s benefit plan design. Employees are typically eligible if they are active participants in the company. HSA eligibility is tied to enrollment in a High Deductible Health Plan (HDHP). Without an accompanying HDHP, an individual cannot contribute to an HSA.

Portability

HSAs are fully portable. The funds remain with the individual regardless of their employment status. HRAs are generally not portable. Upon leaving an employer, any remaining HRA funds are typically forfeited. This makes HSAs a more attractive option for individuals seeking long-term, portable healthcare savings.

Investment Potential

While some HRAs may have limited rollover features, they generally do not offer investment opportunities. HSAs, however, often come with investment options. This allows account holders to grow their healthcare savings through market participation, potentially turning their HSA into a substantial financial asset for future healthcare needs, including retirement.

Strategic Considerations for Employers and Employees

The choice between offering or enrolling in an HRA or HSA often depends on the specific goals and circumstances of both employers and employees. Each offers unique advantages that can be leveraged for optimal healthcare management.

Employer Perspectives

For employers, offering an HRA can be a strategic way to control healthcare costs while providing employees with valuable benefits. HRAs allow employers to set a fixed budget for reimbursements, offering predictability in healthcare spending. They can be particularly useful for smaller businesses that may not have the resources to offer more complex and expensive health insurance plans. Employers can also design HRAs to incentivize healthy behaviors or to cover specific out-of-pocket costs that are common for their workforce. The primary advantage for employers is the direct control over the benefit’s financial parameters.

Employee Perspectives

For employees, the decision between an HRA and an HSA hinges on their personal financial situation, healthcare utilization, and long-term savings goals. If an employee is primarily looking for employer-funded assistance with immediate healthcare costs like deductibles and copays, an HRA might be sufficient. However, if an employee is seeking a portable, long-term savings vehicle with investment potential to cover future healthcare expenses, including retirement, an HSA paired with an HDHP is likely the more advantageous choice. The triple tax advantage and portability of HSAs make them a powerful tool for building significant healthcare wealth over time. Employees should carefully consider their anticipated healthcare needs and their propensity for saving and investing when making this decision.

Conclusion: Tailoring Healthcare Savings Strategies

In conclusion, Health Reimbursement Arrangements (HRAs) and Health Savings Accounts (HSAs) represent distinct approaches to managing healthcare finances. HRAs are employer-funded and employer-controlled, offering a way for businesses to reimburse employees for medical expenses within predefined limits. They are a benefit provided by an employer and are typically forfeited upon leaving that employer. HSAs, on the other hand, are individual-owned, tax-advantaged accounts that are paired with High Deductible Health Plans. They offer unparalleled flexibility, portability, and a powerful triple tax advantage, making them an exceptional tool for both short-term healthcare cost management and long-term financial planning, including retirement healthcare needs. Understanding the nuanced differences between these two powerful savings vehicles is essential for individuals and employers aiming to create robust and effective healthcare savings strategies tailored to their unique circumstances.