The landscape of home financing can often feel complex, with a myriad of terms and product variations designed to cater to diverse financial situations and risk appetites. Among these, the adjustable-rate mortgage (ARM) stands out as a popular, albeit sometimes misunderstood, option. Within the ARM family, the 5/1 ARM is a prevalent choice, offering a unique blend of initial rate stability and potential future adjustments. Understanding its mechanics is crucial for any prospective homeowner navigating the mortgage market. This article delves into the intricacies of the 5/1 ARM, dissecting its structure, exploring its advantages and disadvantages, and highlighting who might benefit most from this type of loan.

Deconstructing the 5/1 ARM: The Hybrid Approach

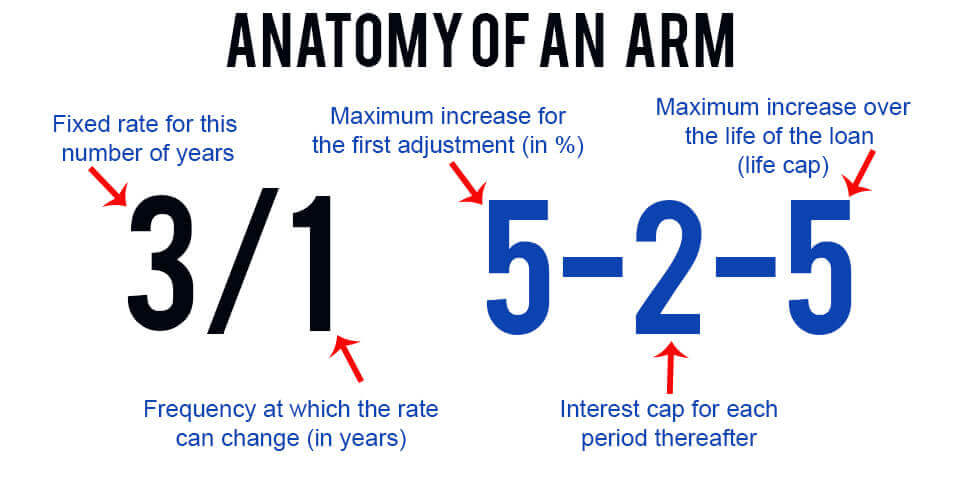

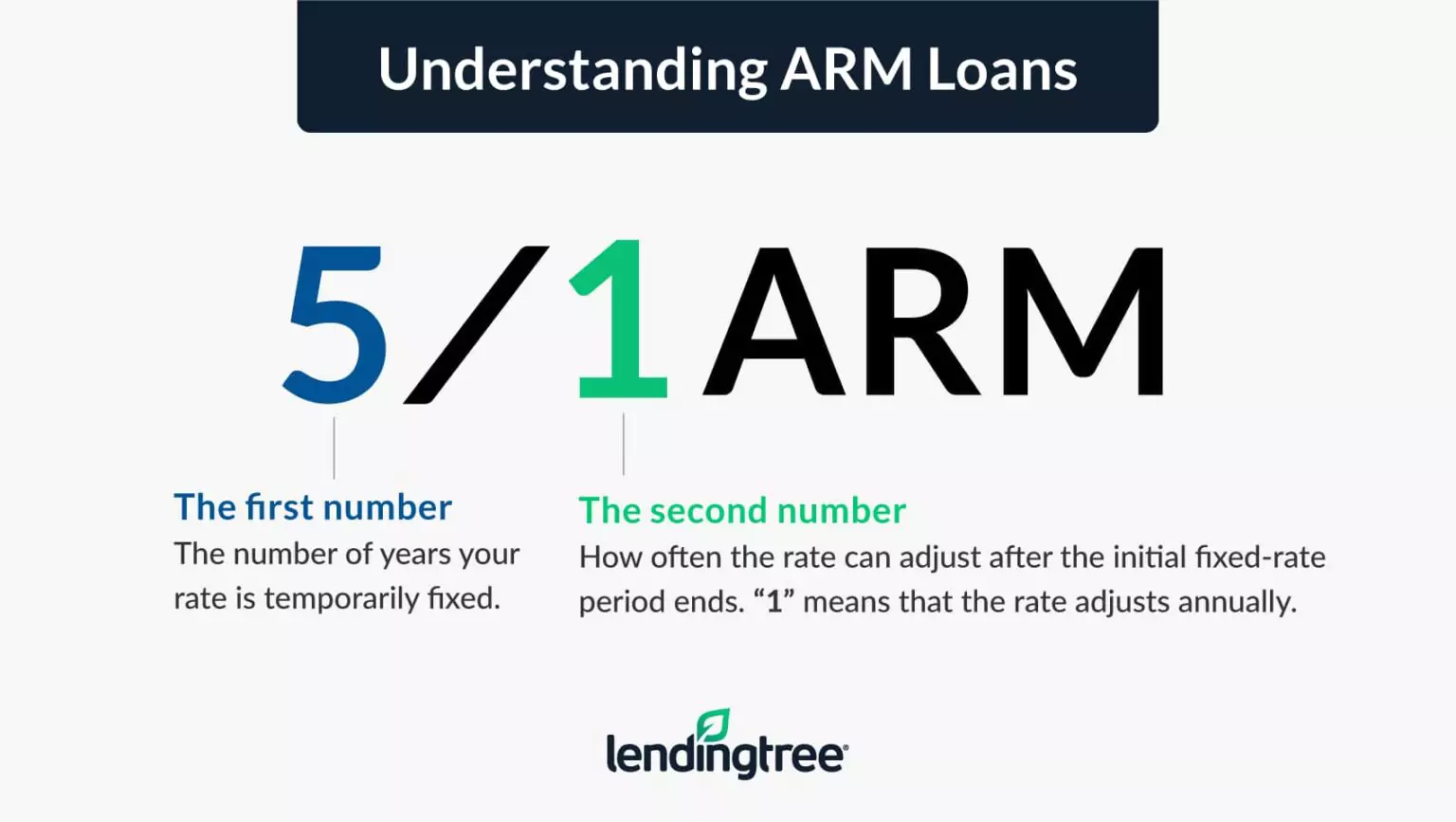

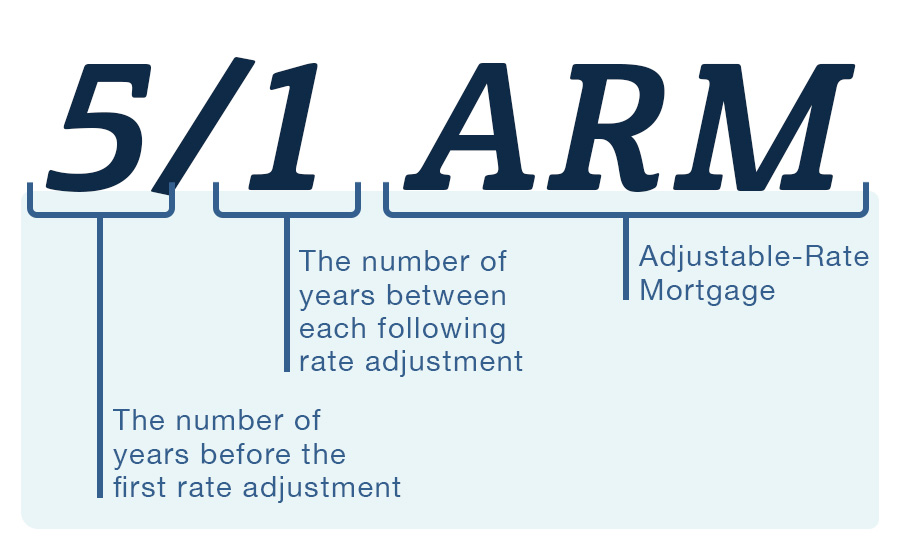

The designation “5/1” in a 5/1 ARM is a shorthand that encapsulates its core feature: a hybrid interest rate structure. This hybrid nature means the mortgage begins with a fixed interest rate for a predetermined period, after which the rate becomes variable and adjusts periodically.

The Fixed-Rate Period: Five Years of Predictability

The “5” in 5/1 ARM signifies the initial period during which the interest rate remains constant. For five years from the loan’s inception, the borrower will pay interest at the same rate, leading to predictable monthly principal and interest payments. This period of stability is a significant draw for many borrowers, as it allows for consistent budgeting and financial planning without the immediate worry of fluctuating housing costs. During these first five years, the borrower is protected from any upward movements in market interest rates.

The Adjustment Period: The “1” in 5/1

The “1” in 5/1 ARM refers to the frequency of interest rate adjustments after the initial fixed period concludes. Once the five-year fixed-rate period expires, the mortgage’s interest rate will begin to adjust every one year thereafter. This means that, from year six onwards, the interest rate can change annually based on prevailing market conditions. These adjustments are not arbitrary; they are typically tied to a specific financial index, such as the Secured Overnight Financing Rate (SOFR) or the London Interbank Offered Rate (LIBOR) (though LIBOR is being phased out and replaced). A margin is then added to this index to determine the new interest rate.

The Index and Margin: The Drivers of Adjustment

The specific index to which a 5/1 ARM is tied is a critical component. Lenders choose an index that reflects broader market interest rate trends. As this index fluctuates, so too does the potential for the ARM’s interest rate to change.

- Index: This is a benchmark interest rate that is publicly available and commonly used in financial markets. Examples include SOFR, which is a broad measure of the cost of borrowing cash overnight collateralized by U.S. Treasury securities. The movement of the chosen index directly influences the interest rate on the ARM.

- Margin: The margin is a fixed percentage that the lender adds to the index to determine the new interest rate. This margin represents the lender’s profit and is set at the time the loan is originated. Unlike the index, the margin does not change over the life of the loan.

The formula for the adjusted interest rate is typically: New Interest Rate = Index + Margin.

Rate Caps: Safeguarding Against Extreme Fluctuations

To prevent drastic and potentially unmanageable payment increases, 5/1 ARMs incorporate interest rate caps. These caps act as limitations on how much the interest rate can change over specific periods and over the lifetime of the loan.

- Periodic Adjustment Caps: These caps limit how much the interest rate can increase or decrease at each adjustment period (in this case, annually). For example, a common cap might be 2% per adjustment. This means the rate cannot jump by more than 2% in any single year after the fixed period.

- Lifetime Caps: This is the maximum interest rate the loan can ever reach over its entire term. A typical lifetime cap might be 5% or 6% above the initial fixed rate. This provides a crucial safety net, ensuring that even in a rapidly rising interest rate environment, the borrower’s rate will not exceed a certain predetermined ceiling.

Understanding these caps is vital, as they define the boundaries of potential payment volatility.

Advantages of the 5/1 ARM

The 5/1 ARM offers several compelling benefits, making it an attractive option for a specific segment of homebuyers.

Lower Initial Interest Rate and Monthly Payments

The most immediate advantage of a 5/1 ARM is its typically lower initial interest rate compared to a traditional 30-year fixed-rate mortgage. Because the lender’s risk is mitigated by the fact that the rate will eventually adjust, they can offer a more favorable rate during the initial fixed period. This translates to lower monthly principal and interest payments for the first five years. For borrowers who can leverage this savings, it can mean more disposable income or the ability to qualify for a larger loan amount than they might otherwise.

Potential for Savings if Rates Decline

If market interest rates fall after the initial five-year period, the borrower could benefit from lower monthly payments. As the index used to set the new rate decreases, the overall interest rate on the ARM will also decrease (assuming the margin remains constant), leading to reduced mortgage payments. This flexibility is a key differentiator from fixed-rate mortgages, which do not offer this potential for downside benefit.

Suitable for Short-Term Homeownership

Borrowers who anticipate selling their home or refinancing their mortgage before the initial five-year fixed-rate period expires may find the 5/1 ARM particularly advantageous. If the loan is paid off or replaced before the rate starts adjusting, the borrower will have enjoyed the benefit of the lower initial rate without ever experiencing an increase. This strategy can be a smart way to acquire a home and then move on before the variable rate period commences.

Ability to Qualify for a Larger Loan

The lower initial monthly payments associated with a 5/1 ARM can help borrowers qualify for a larger mortgage amount. Lenders assess a borrower’s ability to repay based on their debt-to-income ratio, which is heavily influenced by monthly housing expenses. By offering a lower initial payment, a 5/1 ARM can expand purchasing power, enabling borrowers to afford a more expensive home.

Disadvantages and Risks of the 5/1 ARM

Despite its attractions, the 5/1 ARM carries inherent risks that potential borrowers must carefully consider. The primary concern revolves around the potential for rising interest rates and subsequent payment increases.

Risk of Rising Interest Rates and Payments

The most significant drawback of an ARM is the unpredictability of future payments. If market interest rates rise after the initial five-year period, the interest rate on the 5/1 ARM will also increase, leading to higher monthly payments. This escalation can strain a borrower’s budget, especially if their income does not keep pace with the rising costs. The annual adjustments mean that significant payment increases can occur relatively quickly if market conditions are volatile.

Payment Shock

The possibility of “payment shock” is a critical concern. This refers to a sudden and substantial increase in monthly mortgage payments after the fixed-rate period ends. If rates rise significantly, the borrower’s payments could jump considerably, potentially making the mortgage unaffordable. This is particularly a risk if the borrower has not factored in potential payment increases into their long-term financial planning or if their income is not flexible.

Complexity and Misunderstanding

Adjustable-rate mortgages can be more complex to understand than fixed-rate mortgages. Borrowers may not fully grasp the implications of the index, margin, and caps, leading to unexpected financial outcomes. It is imperative for borrowers to fully comprehend all the terms and conditions, including the potential for rate increases and the mechanisms that govern them, before committing to a 5/1 ARM.

Impact on Long-Term Budgeting

While the initial period offers stability, the long-term financial picture becomes less certain. Budgeting for a mortgage with a variable rate requires flexibility and contingency planning. Borrowers need to be prepared for the possibility of higher payments and ensure they have sufficient financial reserves or income growth potential to absorb these increases.

Who Should Consider a 5/1 ARM?

The 5/1 ARM is not a one-size-fits-all mortgage product. It is best suited for individuals and families who meet specific criteria and have a clear understanding of the associated risks and benefits.

Those Planning to Sell or Refinance Within Five Years

As mentioned earlier, this is perhaps the most straightforward scenario where a 5/1 ARM shines. If you are confident that you will move or refinance your mortgage before the five-year fixed period ends, you can capitalize on the lower initial rate without facing the risk of rate adjustments. This could be individuals in jobs that require frequent relocation, or those who foresee significant life changes that would necessitate a move.

Borrowers Expecting Income Growth

Individuals who anticipate a substantial increase in their income over the next five to ten years may be well-positioned to handle potential payment increases. For example, young professionals in rapidly advancing careers, or those expecting significant bonuses or promotions, might strategically use the lower initial payments to acquire a home, knowing they can comfortably manage higher payments in the future.

Those Who Can Afford Higher Payments

Even with the potential for rate increases, some borrowers may still find the 5/1 ARM advantageous if they have a strong financial cushion and can comfortably afford the maximum possible payment under the loan’s caps. This approach provides the benefit of a lower initial payment while simultaneously offering peace of mind that even in the worst-case scenario, the payments remain manageable.

Investors or Second-Home Buyers

For investors who plan to rent out a property, or for those purchasing a second home that may not be their primary residence, the risk tolerance and financial planning might differ from that of a primary homeowner. The initial lower payment could improve cash flow for rental properties, and the flexibility of an ARM might be less of a concern if the property is not expected to be held for the entire loan term.

Conclusion: A Calculated Approach to Homeownership

The 5/1 adjustable-rate mortgage is a valuable tool in the mortgage market, offering a compelling balance between initial rate stability and the potential for future savings or risks. Its hybrid nature, characterized by a five-year fixed-rate period followed by annual adjustments, requires a thorough understanding of its mechanics, including indexes, margins, and rate caps. While it can provide significant advantages, such as lower initial payments and the opportunity to benefit from declining interest rates, it also carries the inherent risk of payment increases if market rates rise.

Ultimately, the decision to opt for a 5/1 ARM should be a deliberate one, based on a careful assessment of one’s financial situation, future income projections, and tolerance for risk. For those who plan to move or refinance within the initial fixed period, or who are confident in their ability to manage potentially higher future payments, the 5/1 ARM can be a strategic and financially sound choice. However, a comprehensive understanding and diligent planning are paramount to navigating its complexities and ensuring it aligns with long-term homeownership goals. Consulting with a qualified mortgage professional is always recommended to explore all available options and determine the best fit for individual circumstances.