The United States tax system operates on a principle of self-assessment and voluntary compliance. This means that individuals are responsible for accurately calculating and reporting their tax liability, and then paying what they owe by the established deadlines. The Internal Revenue Service (IRS) is the agency tasked with enforcing these tax laws. While the IRS does send reminders and notifications, it’s ultimately your responsibility to file your taxes. Forgetting to do so, whether intentionally or unintentionally, can lead to a cascade of consequences, ranging from minor inconveniences to significant financial penalties and legal repercussions. Understanding these potential outcomes is crucial for any taxpayer.

The Immediate Aftermath: Missed Deadlines and Initial Repercussions

The most immediate consequence of forgetting to file your taxes is, of course, missing the tax deadline. In the United States, the primary tax filing deadline for individuals is typically April 15th of each year, though this can shift slightly if it falls on a weekend or holiday. If you realize you’ve missed this deadline, the first and most important step is to determine whether you owe money to the IRS.

Failure to File Penalty

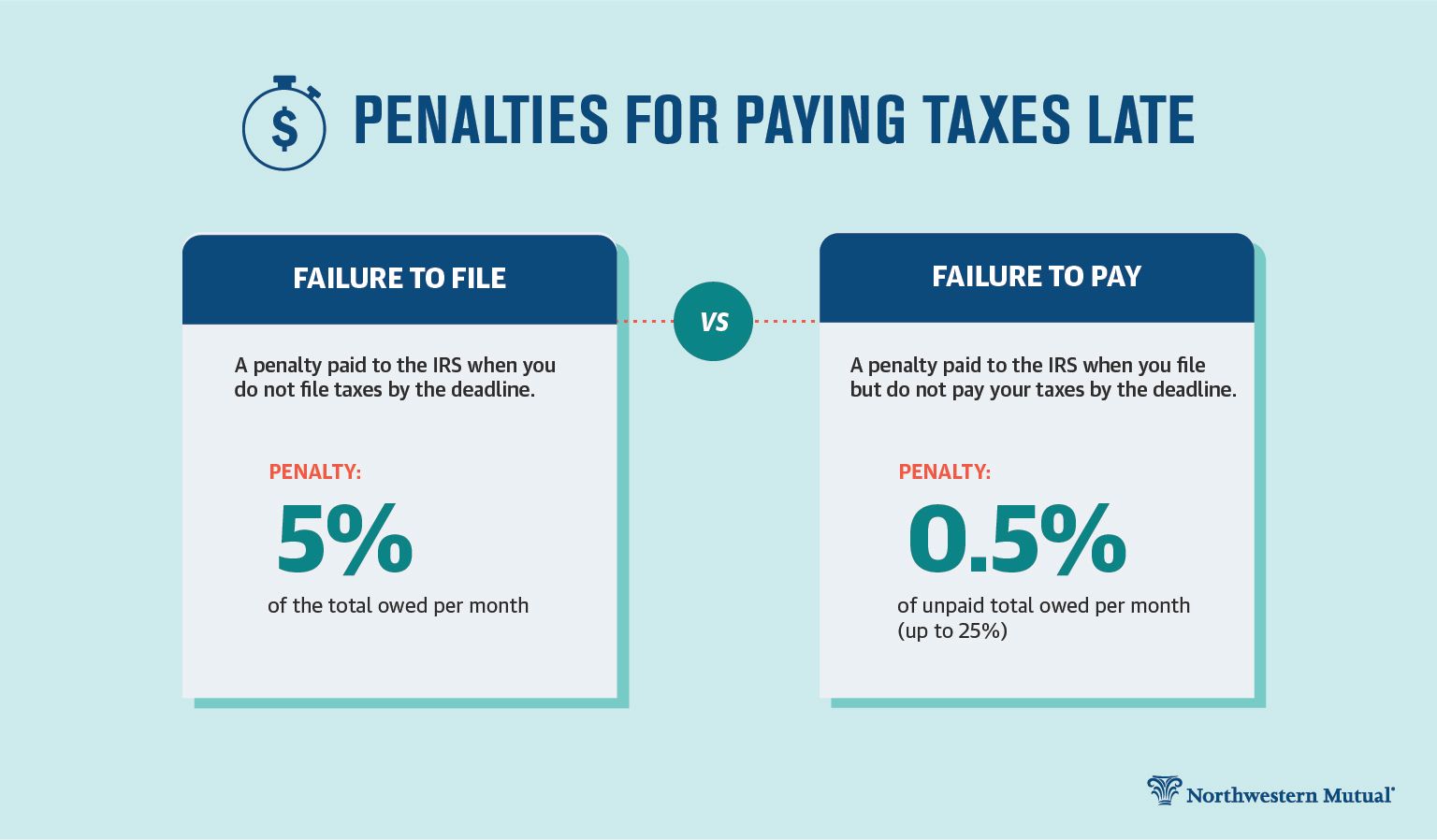

If you owe taxes and do not file your return by the deadline, you will generally be subject to a failure-to-file penalty. This penalty is calculated as a percentage of the unpaid taxes for each month or part of a month that a tax return is late. The penalty typically caps out at 25% of your unpaid taxes. This penalty can be substantial, especially if you have a significant tax liability and delay filing for an extended period. It’s important to note that this penalty is assessed on the unpaid tax. If you are due a refund, there is no penalty for filing late, though you may forfeit your refund if you wait too long to claim it (typically three years from the original due date).

Failure to Pay Penalty

In addition to the failure-to-file penalty, if you owe taxes and do not pay them by the due date (even if you have filed an extension), you will also be subject to a failure-to-pay penalty. This penalty is usually 0.5% of the unpaid taxes for each month or part of a month that the taxes remain unpaid, up to a maximum of 25% of your unpaid taxes.

Interest Charges

Beyond penalties, the IRS also charges interest on underpayments of tax. Interest accrues from the due date of the tax return until the date the tax is paid in full. The interest rate is determined quarterly and is based on the federal short-term rate plus three percentage points. This interest can significantly increase the total amount you owe over time, compounding the financial burden.

The IRS’s Response: Notices and Assessments

The IRS is a massive organization with sophisticated systems for tracking tax filings and payments. When you miss a deadline and owe taxes, they will eventually notice. Their response typically begins with a series of notices, designed to inform you of your non-compliance and provide opportunities to rectify the situation.

Notice CP14: Your First Notice

One of the first notices you might receive is a Notice CP14, “Your New Balance Due.” This notice informs you that you owe a balance to the IRS. It will detail the amount of tax you owe, along with any accrued penalties and interest. It’s crucial to read these notices carefully and respond promptly, as ignoring them will only exacerbate the problem.

Substitute for Return (SFR)

If you fail to file your tax return for an extended period, the IRS may eventually prepare a “Substitute for Return” (SFR) on your behalf. The SFR is based on information reported to the IRS by third parties, such as employers (W-2s) and financial institutions (1099s). The SFR typically calculates your tax liability based on this information, and it often does not take into account any deductions or credits you may be eligible for. The IRS will then send you a notice of deficiency, proposing to assess the tax, penalties, and interest shown on the SFR. It is highly advisable to respond to an SFR notice. You have the right to protest the proposed assessment and file your own tax return to claim any legitimate deductions and credits.

Escalation of Consequences: Liens, Levies, and Legal Action

If you continue to ignore IRS notices and fail to address your tax obligations, the IRS has significant enforcement powers to collect the money owed. These powers can have severe and long-lasting impacts on your financial well-being.

Tax Liens

A federal tax lien is a legal claim by the IRS against all of your current and future property, including real estate, personal property, and financial assets. This lien arises automatically once the IRS assesses your tax liability and you neglect or refuse to pay it. A tax lien is a public record and can significantly harm your credit score, making it difficult to obtain loans, mortgages, or even rent an apartment. The IRS can also take action to enforce the lien, which could lead to the seizure and sale of your assets.

Tax Levies

A levy is the IRS’s actual seizure of your property to satisfy a tax debt. Unlike a lien, which is a claim on your property, a levy is the taking of that property. Common forms of levies include:

- Wage Garnishment: The IRS can order your employer to withhold a portion of your wages and send it directly to the IRS.

- Bank Levy: The IRS can seize funds from your bank accounts.

- Property Seizure: In more severe cases, the IRS can seize and sell your assets, such as your home, car, or other valuable property.

The IRS typically provides several notices before a levy is placed on your property, giving you an opportunity to resolve the debt.

Passport Denial or Revocation

If you have a “seriously delinquent tax debt” (currently over $59,000, indexed for inflation, owed by you or jointly with your spouse), the IRS can certify this debt to the State Department, which can result in the denial of your passport application or the revocation of your existing passport. This can have significant implications for international travel and business.

Criminal Prosecution

While most tax non-compliance issues are handled through civil penalties, intentional tax evasion can lead to criminal prosecution. This is reserved for cases where there is evidence of willful intent to defraud the government, such as deliberately hiding income, claiming fraudulent deductions, or deliberately not filing taxes with the intent to avoid paying. Criminal tax evasion can result in substantial fines, imprisonment, and a criminal record, which has lifelong consequences.

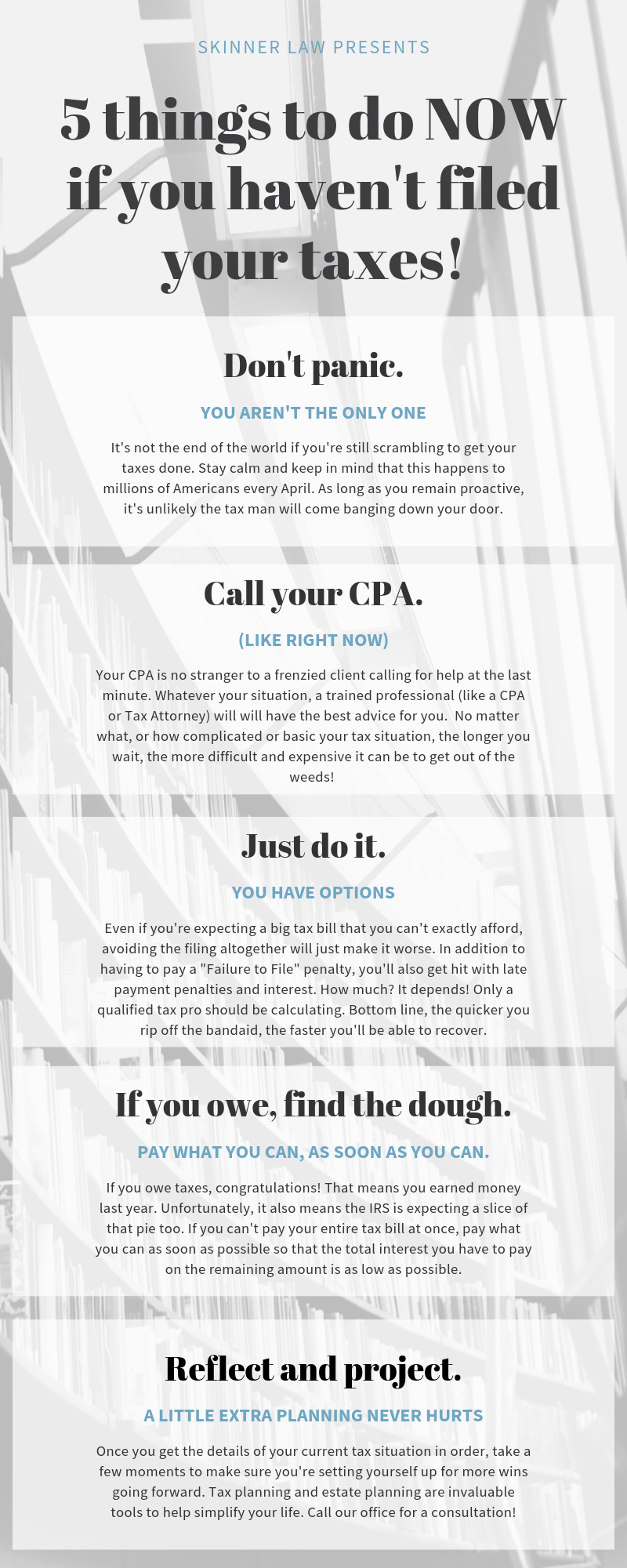

Steps to Take If You Forgot to File

Discovering that you’ve forgotten to file your taxes can be a daunting experience. However, taking prompt and decisive action can mitigate the potential negative consequences.

File Immediately

The most crucial step is to file your tax return as soon as possible, even if you cannot pay the full amount owed. Filing your return stops the failure-to-file penalty from accruing further and demonstrates your willingness to comply.

Pay What You Can

If you owe taxes, try to pay as much of the balance as you can by the due date, or as soon as you file your return. Even a partial payment can reduce the amount of interest and penalties you will owe.

Explore Payment Options

If you cannot afford to pay the full amount of your tax liability, the IRS offers several payment options:

- Offer in Compromise (OIC): An OIC allows certain taxpayers to resolve their tax debt for a lower amount than they owe. This option is typically available to those who are experiencing significant financial hardship and cannot pay their full tax liability.

- Installment Agreement: You can request to pay your tax debt in monthly installments over a period of up to 72 months. Setting up an installment agreement can help reduce the failure-to-pay penalty (though interest will still accrue).

- Currently Not Collectible Status: If you can demonstrate that you are unable to pay your tax debt due to financial hardship, the IRS may temporarily classify your account as “currently not collectible.” This does not eliminate your tax debt, but it will stop collection actions for a period.

Seek Professional Assistance

Navigating IRS procedures can be complex. If you are facing significant tax liabilities or are unsure about your options, it is highly recommended to consult with a qualified tax professional, such as a Certified Public Accountant (CPA) or an Enrolled Agent (EA). They can help you understand your rights and responsibilities, prepare your delinquent tax returns, and negotiate with the IRS on your behalf.

Forgetting to file your taxes is a serious matter with potentially severe financial and legal ramifications. However, by understanding the consequences and taking proactive steps to address the situation, taxpayers can minimize the damage and work towards resolving their tax obligations. The key is to act swiftly, communicate with the IRS, and seek professional guidance when necessary.