Reconciling accounts is a fundamental financial process that ensures the accuracy and integrity of your financial records. It involves comparing two sets of records to ensure they are in agreement and that all transactions have been properly recorded. While the term “reconcile accounts” might sound technical or intimidating, its core concept is simple: making sure your books balance and that your reported financial position is a true reflection of reality. This process is critical for individuals, small businesses, and large corporations alike, serving as a vital control mechanism against errors, fraud, and omissions.

The Importance of Account Reconciliation

The significance of account reconciliation extends far beyond merely ticking boxes on a checklist. It’s a proactive measure that underpins sound financial management and strategic decision-making. Without regular and accurate reconciliation, a business operates blind, susceptible to a cascade of potential problems.

Ensuring Financial Accuracy and Integrity

At its heart, reconciliation is about truth. It’s the process of verifying that the money that entered your bank account is precisely what your accounting records indicate, and that every penny spent has been accounted for. This involves comparing your internal accounting records (like your general ledger) with external financial statements, most commonly bank statements. Any discrepancies, whether they are small errors, unrecorded transactions, or potentially fraudulent activities, are brought to light through this meticulous comparison. This ensures that your financial statements, which are used by stakeholders – including investors, lenders, and management – to make critical decisions, are reliable and trustworthy.

Detecting Errors and Omissions

Human error is an unavoidable aspect of any manual process, and accounting is no exception. During the course of daily transactions, entries can be duplicated, omitted, or incorrectly recorded. Bank reconciliation, for example, often uncovers outstanding checks that haven’t yet cleared, deposits in transit that haven’t yet been credited, or bank service charges that haven’t been entered into the company’s books. Similarly, reconciling accounts receivable with customer payments can reveal if a customer paid an incorrect amount or if an invoice was mistakenly marked as paid. Prompt detection of these errors prevents them from snowballing into larger issues that could distort financial performance and lead to misinformed strategic choices.

Preventing and Detecting Fraud

Fraudulent activities can range from outright theft to more subtle manipulations of financial data. Reconciling accounts acts as a powerful deterrent and detection tool against such malfeasance. When accounts are reconciled regularly, suspicious transactions or unusual patterns are more likely to be spotted. For instance, if a bank statement shows a withdrawal that doesn’t correspond to any authorized company expenditure, it flags a potential problem. Similarly, reconciling petty cash can reveal discrepancies between recorded expenses and actual cash on hand. By implementing a robust reconciliation process, organizations demonstrate a commitment to transparency and accountability, making it harder for fraudulent activities to go unnoticed.

Improving Cash Flow Management

Understanding your actual cash position is paramount for effective cash flow management. Reconciliation provides a clear picture of your available funds. By comparing your internal records with bank statements, you can identify discrepancies in cash balances and anticipate upcoming cash inflows and outflows more accurately. This allows for better planning of expenses, investments, and debt repayments, ultimately contributing to a healthier and more stable financial position. Knowing exactly how much cash is readily available helps avoid overdraft fees, missed payment opportunities, and unnecessary borrowing.

Supporting Audits and Compliance

Whether for internal reviews or external audits, accurate and well-maintained financial records are essential. The process of account reconciliation is a cornerstone of a sound audit trail. Auditors will invariably examine reconciliation reports to verify the accuracy of financial statements and the effectiveness of internal controls. Demonstrating a consistent and thorough reconciliation process simplifies the audit process, reduces audit fees, and instills confidence in the integrity of your financial reporting, which is crucial for regulatory compliance.

Types of Accounts to Reconcile

While the principle of reconciliation is universal, its application varies across different types of financial accounts. Each type of reconciliation addresses specific aspects of financial health and operational efficiency.

Bank Reconciliations

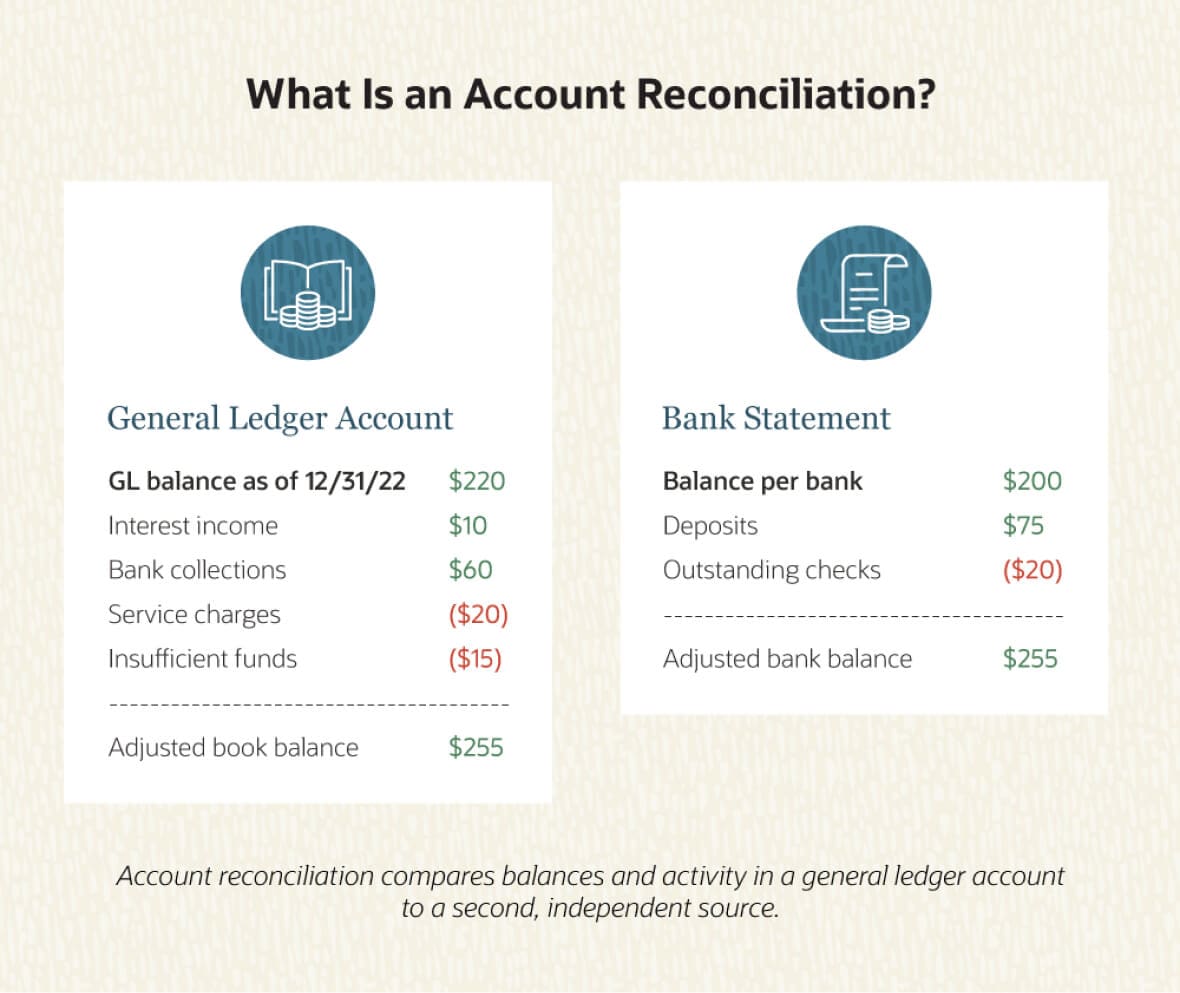

This is perhaps the most common and frequently performed type of reconciliation. It involves comparing the cash balance in a company’s accounting records with the corresponding balance on its bank statement. The goal is to identify and explain any differences. Common reconciling items include:

- Deposits in Transit: Deposits made by the company but not yet recorded by the bank.

- Outstanding Checks: Checks issued by the company that have not yet been cashed or cleared by the bank.

- Bank Service Charges: Fees charged by the bank that may not have been recorded in the company’s books.

- Interest Earned: Interest credited to the account by the bank that may not have been recorded internally.

- NSF (Non-Sufficient Funds) Checks: Checks received by the company that were returned by the bank due to insufficient funds in the payer’s account.

- Errors: Mistakes made by either the company in recording transactions or by the bank in processing them.

Performing bank reconciliations regularly (often monthly) is crucial for accurate cash management and for detecting any unauthorized transactions or errors.

Accounts Receivable Reconciliations

This process involves comparing the subsidiary ledger for accounts receivable (which details individual customer balances) with the general ledger control account for accounts receivable. It ensures that the total amount owed by customers, as recorded in the detailed customer accounts, matches the total amount recorded as accounts receivable in the main accounting system. This reconciliation helps:

- Identify Unpaid Invoices: Pinpointing which customers owe money and how much.

- Detect Payment Errors: Ensuring that customer payments have been correctly applied to their respective accounts.

- Flag Delinquent Accounts: Highlighting overdue balances that may require collection efforts.

- Verify Creditworthiness: Ensuring that the overall accounts receivable balance is realistic and reflects actual outstanding obligations.

A thorough accounts receivable reconciliation supports effective credit management and optimizes cash inflows from sales.

Accounts Payable Reconciliations

Similar to accounts receivable, accounts payable reconciliation involves comparing the subsidiary ledger for accounts payable (listing all outstanding invoices from suppliers) with the general ledger control account for accounts payable. This ensures that the total amount the company owes to its vendors is accurately reflected. Key benefits include:

- Preventing Duplicate Payments: Ensuring that the same invoice is not paid more than once.

- Identifying Missed Invoices: Discovering any supplier invoices that have not been entered into the accounting system, which could lead to missed payment deadlines and late fees.

- Verifying Vendor Balances: Confirming that the amounts due to each vendor are correct.

- Securing Early Payment Discounts: By having a clear view of upcoming payments, businesses can take advantage of early payment discounts offered by suppliers.

Accurate accounts payable reconciliation contributes to strong vendor relationships and sound financial planning.

Credit Card Reconciliations

For businesses that use credit cards, reconciling these statements with internal records is essential. This involves comparing the credit card statement with the expense records and any internal logs of credit card purchases. It helps to:

- Identify Unauthorized Charges: Spotting any transactions that were not made by authorized personnel.

- Track Expenses: Ensuring all credit card expenses are properly categorized and recorded in the accounting system.

- Verify Payment Amounts: Confirming that the correct amount is being paid to the credit card company.

- Manage Credit Limits: Keeping track of outstanding balances to stay within credit limits.

Petty Cash Reconciliations

Petty cash is a small amount of cash kept on hand by an organization for minor, immediate expenses. Reconciling petty cash involves counting the physical cash on hand and comparing it to the recorded balance of the petty cash fund, accounting for all disbursed receipts. This process ensures:

- Fund Integrity: Verifying that the cash balance is accurate.

- Proper Use of Funds: Confirming that all disbursements are legitimate and supported by receipts.

- Reimbursement Accuracy: Ensuring that the fund is replenished with the correct amount based on documented expenses.

The Process of Account Reconciliation

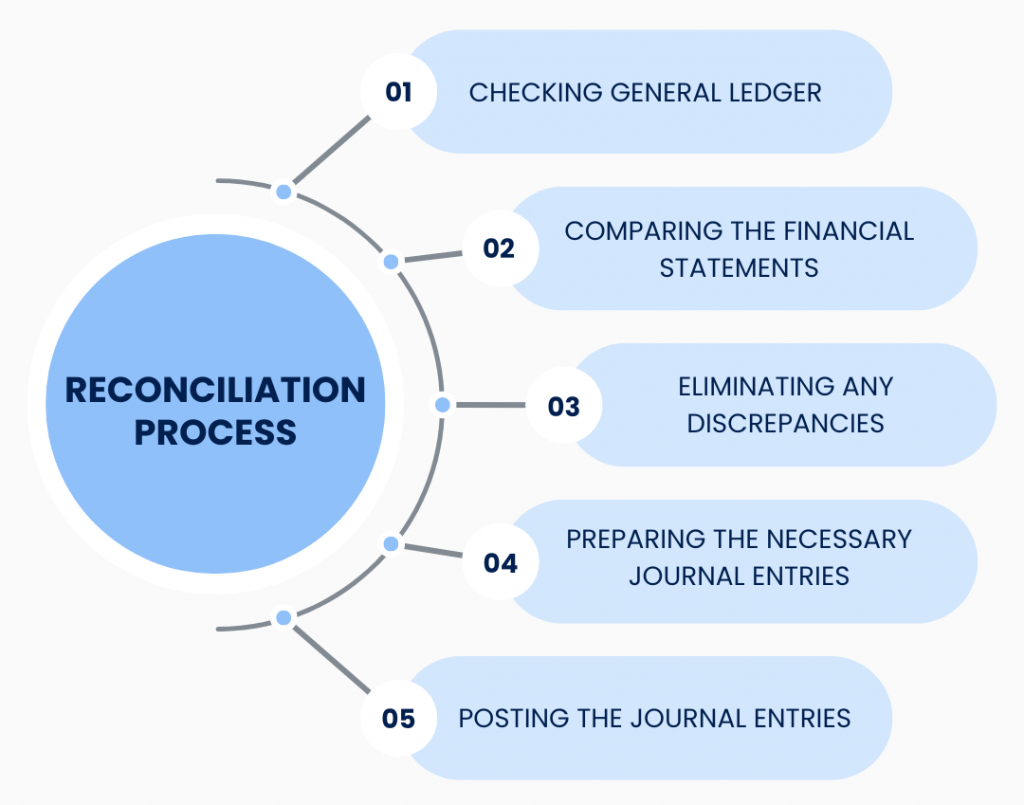

While the specific steps might vary slightly depending on the account type and the accounting software used, the fundamental process of account reconciliation involves a systematic approach to comparing and adjusting financial records.

Step 1: Gather Necessary Documents

The first step is to collect all relevant financial documents. This typically includes:

- The most recent bank statement for the account being reconciled.

- The corresponding period’s accounting records (e.g., general ledger, subsidiary ledgers, journal entries).

- Any supporting documentation for transactions, such as check registers, deposit slips, invoices, and receipts.

- Previous reconciliation reports, if available.

Step 2: Compare Account Balances

Begin by comparing the ending balance reported on the bank statement with the ending balance shown in the company’s accounting records for the same period. These balances are unlikely to match initially due to timing differences and unrecorded transactions.

Step 3: Identify and List Discrepancies

Systematically go through both sets of records to identify and list all items that appear on one statement but not the other, or items that have different amounts. This involves:

- For Bank Reconciliations:

- Check off all deposits listed on the bank statement against the company’s records. Any deposits in the company’s books not on the statement are “deposits in transit.”

- Check off all checks cleared by the bank against the company’s check register. Any checks issued by the company but not yet cleared by the bank are “outstanding checks.”

- Identify any bank charges, interest earned, or NSF checks on the bank statement that are not in the company’s records.

- For Other Account Reconciliations: Follow a similar process of comparing detailed records with summary accounts or external statements, noting any differences.

Step 4: Adjust for Timing Differences and Unrecorded Transactions

Once discrepancies are identified, adjust the balances to account for them.

- Adjusting the Bank Statement Balance: Add deposits in transit and subtract outstanding checks. Include any bank errors that need correction.

- Adjusting the Book Balance: Add interest earned and subtract bank service charges, NSF checks, or any other expenses that need to be recorded. Also, add any recorded transactions that the bank has not yet processed.

Step 5: Calculate the Reconciled Balance

After making all the necessary adjustments, the goal is to arrive at a single, reconciled balance that is the same for both the bank statement and the company’s books. If the adjusted balances match, the reconciliation is successful.

Step 6: Record Adjusting Entries

Any items identified during the reconciliation process that affect the company’s accounting records (e.g., bank fees, interest income, NSF checks) must be formally recorded through journal entries. These entries bring the company’s books into agreement with the corrected financial position. For example, a journal entry would be made to record bank service charges as an expense.

Step 7: Review and Finalize

Review the completed reconciliation report for accuracy and completeness. Ensure all discrepancies have been properly investigated and accounted for. The reconciled report should be signed and dated by the person performing the reconciliation, and ideally reviewed by a supervisor or manager to ensure proper oversight.

Best Practices for Effective Reconciliation

To maximize the benefits of account reconciliation and ensure it is a smooth and effective process, several best practices should be adopted.

Reconcile Promptly and Regularly

The most effective approach is to reconcile accounts as soon as financial statements become available, typically on a monthly basis. Delaying reconciliation allows discrepancies to accumulate, making them harder to track down and resolve. Regularity transforms reconciliation from a reactive chore into a proactive financial management tool.

Utilize Accounting Software

Modern accounting software significantly streamlines the reconciliation process. Many platforms offer automated bank feeds and built-in reconciliation tools that can match transactions, flag exceptions, and generate reports, saving considerable time and reducing the risk of manual errors.

Establish Clear Procedures and Responsibilities

Document a clear reconciliation policy that outlines the steps involved, the frequency of reconciliation, and who is responsible for performing and reviewing the process. This ensures consistency and accountability, regardless of personnel changes. Segregating duties, where possible, by having one person perform the reconciliation and another review it, adds an extra layer of control.

Maintain Supporting Documentation

Keep all supporting documents for transactions readily accessible. This documentation is crucial for investigating discrepancies and provides the necessary evidence for audit purposes. A well-organized filing system for invoices, receipts, and statements is indispensable.

Investigate All Discrepancies Thoroughly

Do not overlook small discrepancies. Even minor differences can indicate underlying issues, such as errors in data entry or potential fraudulent activity. A thorough investigation ensures that no problem goes unnoticed.

Review Reconciliation Reports

Beyond just performing the reconciliation, it’s vital to regularly review the reconciliation reports themselves. This review should be conducted by someone with oversight responsibility to ensure the process is being followed correctly and that the financial information is accurate.

Train Personnel Properly

Ensure that the individuals responsible for reconciliation are adequately trained on the accounting software, the company’s specific reconciliation procedures, and the principles of financial accounting. This investment in training will lead to more accurate and efficient reconciliation.

In conclusion, account reconciliation is a vital, non-negotiable component of sound financial management. It is the process of ensuring that your financial records accurately reflect your actual financial position. By diligently comparing and verifying different financial data sources, businesses and individuals can maintain financial integrity, detect errors, prevent fraud, and make better-informed decisions, ultimately contributing to greater financial stability and success.