Understanding Delta in Options Trading

Delta is a fundamental concept in options trading, representing one of the five “Greeks,” which are metrics used to measure an option’s sensitivity to various factors. Specifically, delta measures how much an option’s price is expected to change for a $1 change in the underlying asset’s price. For example, if a call option has a delta of 0.50, its price is expected to increase by $0.50 for every $1 increase in the underlying stock price. Conversely, if a put option has a delta of -0.40, its price is expected to decrease by $0.40 for every $1 increase in the underlying stock price, or increase by $0.40 for every $1 decrease.

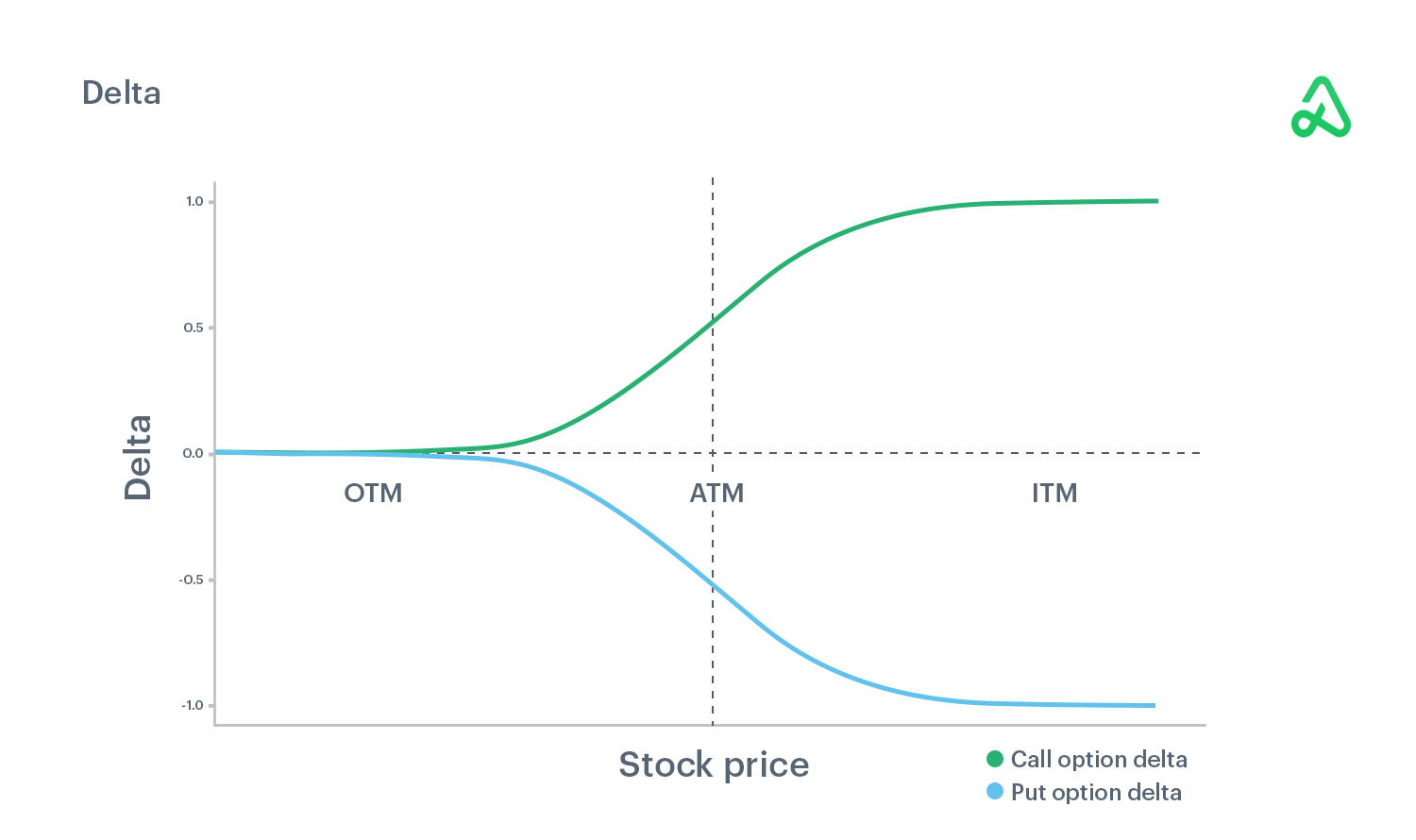

The Range and Interpretation of Delta

Delta for call options ranges from 0 to 1, while delta for put options ranges from -1 to 0.

-

Call Options:

- A delta of 1 indicates that the option’s price will move in perfect lockstep with the underlying asset’s price. This is typical for deep-in-the-money call options, where the option is essentially behaving like owning 100 shares of the underlying stock.

- A delta of 0 suggests that the option’s price will not change at all with a $1 move in the underlying asset. This is characteristic of far-out-of-the-money call options, where there is very little chance of the option expiring in the money.

- Options that are at-the-money typically have a delta around 0.50. This means they are equally sensitive to both upside and downside moves in the underlying asset.

-

Put Options:

- A delta of -1 indicates that the option’s price will move in perfect opposition to the underlying asset’s price. This is characteristic of deep-in-the-money put options.

- A delta of 0 suggests that the option’s price will not change at all with a $1 move in the underlying asset. This is typical for far-out-of-the-money put options.

- At-the-money put options also typically have a delta around -0.50.

Understanding delta is crucial for traders as it helps in assessing the potential profit and loss of an options position and for hedging strategies.

Delta and Risk Management

Delta plays a significant role in managing the risk associated with options positions. By understanding the delta of an option, traders can:

- Estimate Potential Price Changes: As mentioned, delta provides a direct estimate of how much an option’s price will change for a given move in the underlying asset. This allows traders to forecast potential profits and losses.

- Hedge Positions: Delta is a key component in delta-hedging strategies. Traders can use the delta of their options positions to offset the risk of adverse price movements in the underlying asset. For instance, if a trader is long call options with a delta of 0.60, they are effectively exposed to 60% of the underlying asset’s movement. To hedge this exposure, they could sell 60 shares of the underlying stock for every 100 call options they hold. This creates a delta-neutral position, meaning the overall value of the portfolio (stock + options) will not change with small movements in the underlying asset’s price.

- Manage Portfolio Delta: For traders with multiple options positions, calculating the aggregate delta of their portfolio is essential. This sum provides a view of the overall sensitivity of their entire options book to market movements. A positive portfolio delta means the portfolio will gain value if the underlying assets rise, while a negative portfolio delta means it will gain value if the underlying assets fall.

Effective use of delta in risk management allows traders to maintain desired risk profiles and protect their capital.

Delta and Probability

While delta is not a direct measure of probability, it has a strong correlation with the probability of an option expiring in the money.

- Call Options: For call options, delta can be interpreted as the approximate probability that the option will expire in the money. A call option with a delta of 0.70 suggests that there is roughly a 70% chance it will expire in the money.

- Put Options: For put options, the absolute value of delta can be interpreted similarly. A put option with a delta of -0.60 suggests that there is roughly a 60% chance it will expire in the money.

This probabilistic interpretation is particularly useful for “at-the-money” options. As an option moves deeper into the money, its delta will approach 1 (for calls) or -1 (for puts), reflecting a higher certainty of expiring in the money. Conversely, as an option moves further out of the money, its delta approaches 0, indicating a lower probability of expiring in the money.

It’s important to note that this is an approximation. Factors like time decay (theta) and changes in implied volatility (vega) also influence option prices, and therefore the precise probability of expiring in the money can differ from delta. However, delta provides a quick and useful heuristic.

Factors Influencing Delta

Delta is not a static number; it changes dynamically with several factors related to the option and the underlying asset. Understanding these influences is key to accurately predicting option price movements.

The Underlying Asset’s Price

The most direct influence on delta is the price of the underlying asset relative to the option’s strike price.

- In-the-Money Options: As an underlying asset’s price moves further into the money for a call option (i.e., stock price significantly above strike price), the delta approaches 1. For a put option, as the underlying asset’s price moves significantly below the strike price, the delta approaches -1. This is because the option behaves more like owning or shorting the underlying asset itself.

- At-the-Money Options: Options that are at-the-money, where the underlying asset’s price is close to the strike price, tend to have deltas around 0.50 for calls and -0.50 for puts. These options are the most sensitive to changes in the underlying asset’s price, as a small move can push them in or out of the money.

- Out-of-the-Money Options: As an underlying asset’s price moves further out of the money for a call option (i.e., stock price significantly below strike price), the delta approaches 0. Similarly, for a put option, as the underlying asset’s price moves significantly above the strike price, the delta approaches 0. These options have a low probability of expiring in the money and thus a low sensitivity to the underlying’s price.

Time to Expiration

The amount of time remaining until an option expires also affects its delta. This relationship is primarily governed by gamma, which measures the rate of change of delta.

- Longer Time to Expiration: Options with longer times to expiration generally have deltas that are less extreme. For example, an at-the-money call option with a year until expiration might have a delta closer to 0.40 or 0.45, while one with a week until expiration might be closer to 0.55 or 0.60. This is because there is more time for the underlying asset’s price to move and for the option to become in-the-money.

- Shorter Time to Expiration: As an option approaches its expiration date, its delta tends to move towards its extreme values (1 or -1 for in-the-money options, and 0 for out-of-the-money options). This is because the probability of the underlying asset making a significant move that would result in the option expiring in-the-money diminishes rapidly for out-of-the-money options, while in-the-money options become more certain to retain their intrinsic value.

Implied Volatility

Implied volatility, which represents the market’s expectation of future price fluctuations in the underlying asset, also influences delta.

- Higher Implied Volatility: When implied volatility is high, options become more expensive. This increased premium is due to a greater chance of substantial price swings that could move the option into profitable territory. For both call and put options, higher implied volatility tends to push the delta of at-the-money options closer to 0.50 and -0.50, respectively. It also increases the delta of out-of-the-money options (making them more sensitive to price changes) and decreases the delta of in-the-money options (making them less sensitive).

- Lower Implied Volatility: Conversely, when implied volatility is low, options are cheaper, and the market anticipates less price movement. This causes the deltas of at-the-money options to move away from 0.50 and -0.50. Out-of-the-money options will have lower deltas, and in-the-money options will have higher deltas, reflecting a more certain outcome.

Calculating and Using Delta

Delta can be calculated using theoretical option pricing models, such as the Black-Scholes-Merton model. While complex for manual calculation, readily available tools and platforms provide delta values for options.

The Black-Scholes Model and Delta

The Black-Scholes-Merton model is a mathematical framework used to determine the theoretical price of European-style options. One of the key outputs of this model is delta. For a call option, the Black-Scholes delta formula is:

$Delta{call} = N(d1)$

Where:

- $N(d1)$ is the cumulative standard normal distribution function applied to the value $d1$.

- $d1$ is calculated as:

$d1 = frac{ln(frac{S}{K}) + (r + frac{sigma^2}{2})t}{sigmasqrt{t}}$

For a put option, the delta is:

$Delta{put} = N(d1) – 1$

Where:

- $S$ is the current price of the underlying asset.

- $K$ is the strike price of the option.

- $r$ is the risk-free interest rate.

- $sigma$ is the implied volatility of the underlying asset.

- $t$ is the time to expiration in years.

While understanding the formula provides insight, most traders rely on their brokerage platform or financial data providers to obtain real-time delta values.

Practical Applications of Delta

Delta is a cornerstone for several practical trading strategies:

- Directional Bets: Traders use delta to gauge the leverage and directional exposure of their options trades. A high delta call option is a strong bet on the underlying asset moving higher, offering more immediate profit potential for each point the underlying gains.

- Hedging Strategies:

- Delta Hedging: As discussed, this involves creating a portfolio that is neutral to small price movements in the underlying asset. This is often used by market makers to hedge their inventory of options.

- Portfolio Delta Management: Understanding the net delta of all positions allows traders to manage their overall exposure to market direction. A trader who is bullish might aim for a positive portfolio delta, while a bearish trader would seek a negative delta.

- Volatility Trading: While delta is primarily about price movement, understanding how delta changes (gamma) is crucial for strategies that are sensitive to volatility. For example, buying options can benefit from increasing volatility, and understanding the delta helps in constructing positions that profit from these moves while managing the directional risk.

- Income Generation (e.g., Covered Calls, Cash-Secured Puts): When selling options for income, delta helps in assessing the risk being taken. For a covered call, the delta of the sold call indicates how much of the stock’s upside potential is being sold off. For a cash-secured put, the delta shows the probability of the stock price falling and the obligation to buy the stock.

Delta as a Dynamic Indicator

It is crucial to remember that delta is not fixed. It changes as the underlying asset’s price, time to expiration, and implied volatility change.

- Gamma: The rate at which delta changes is measured by gamma. High gamma means delta will change rapidly with small price movements of the underlying, making delta hedging more challenging and requiring more frequent adjustments. Options that are at-the-money and have short times to expiration typically have the highest gamma.

- Theta: Time decay, measured by theta, also impacts delta. As an option approaches expiration, its delta moves towards 0 or 1/-1, reflecting the decreasing probability of significant price movements.

Traders must continuously monitor and recalculate their delta exposure, especially when employing delta-hedging strategies, to ensure their positions remain aligned with their intended risk profile. Sophisticated trading platforms automate these calculations, allowing traders to make informed decisions in real-time. Understanding delta, therefore, is not just about knowing a single number but about grasping its dynamic nature and its interplay with other options Greeks.