The world of real estate and finance can often feel like navigating a complex maze, with terminology and concepts that are new to many borrowers. Among these, “lender points,” often referred to as “discount points,” are a frequent topic of discussion when securing a mortgage. Understanding what lender points are, how they function, and their implications is crucial for making informed financial decisions. This article delves into the intricacies of lender points, exploring their purpose, calculation, and strategic use in the context of real estate financing.

The Core Concept of Lender Points

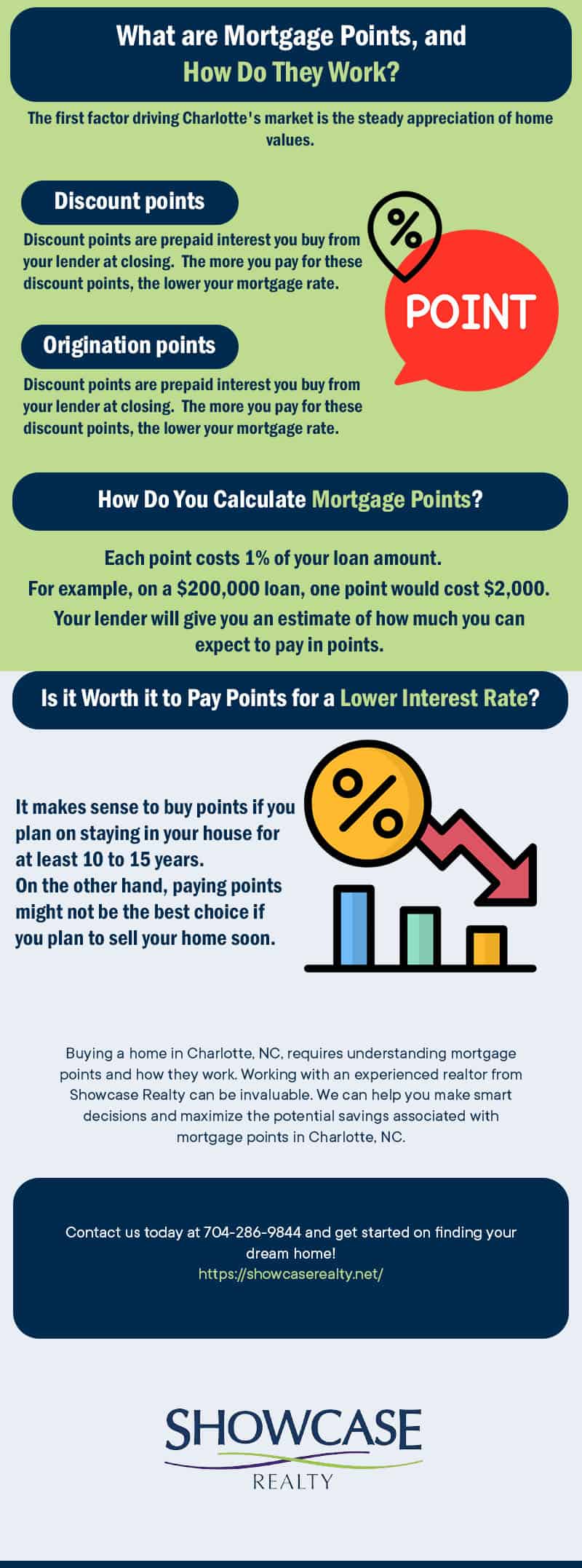

At its heart, a lender point is a fee paid directly to the lender at closing in exchange for a reduction in the interest rate on a mortgage loan. One point is equivalent to 1% of the loan amount. For instance, if a borrower is taking out a $200,000 mortgage and pays one point, they will pay $2,000 upfront at closing. In return for this upfront payment, the lender will typically lower the interest rate on the loan, often by a fraction of a percentage point.

How Points Influence Interest Rates

The relationship between paying points and reducing the interest rate is not a fixed, universally mandated formula. Instead, it’s a negotiation between the borrower and the lender, influenced by market conditions and the lender’s specific pricing strategies. Generally, for every point paid, a borrower might see a reduction of 0.25% to 1% in their annual interest rate. This reduction, while seemingly small, can have a significant impact on the total amount of interest paid over the life of a loan, especially for long-term mortgages like 15 or 30 years.

For example, consider a $300,000 loan at a 7% interest rate for 30 years.

- Without paying any points, the monthly principal and interest payment would be approximately $1,995.90. Over 30 years, the total interest paid would be $418,524.

- If the borrower pays one point ($3,000) to reduce the interest rate to 6.75%, the monthly payment would decrease to approximately $1,946.46. Over 30 years, the total interest paid would be $398,724. In this scenario, the borrower paid an extra $3,000 upfront but saved approximately $19,800 in interest over the loan’s term.

This illustrates the fundamental trade-off: an upfront cost in exchange for long-term savings. The decision to pay points hinges on how long the borrower anticipates holding the mortgage and whether the interest savings outweigh the initial expense.

The Purpose of Lender Points

Lender points serve a dual purpose. For the lender, they represent an immediate injection of capital and a way to generate revenue beyond the standard interest payments. This can be particularly attractive to lenders in a market with lower interest rates, where profit margins might be squeezed. By offering the option to buy down the interest rate, lenders can attract borrowers who are seeking the lowest possible monthly payments and are willing to pay for that benefit upfront.

For the borrower, the primary motivation for paying points is to reduce their monthly mortgage payment and, consequently, the total interest paid over the life of the loan. This strategy is often employed by individuals who plan to stay in their home for a significant period, making the long-term savings a worthwhile investment. It can also be a way to improve cash flow by lowering the ongoing debt burden, freeing up funds for other financial goals.

Types of Lender Points

While the general concept of “lender points” remains the same, there are two main types: discount points and origination points. Understanding the distinction is important for borrowers.

Discount Points

Discount points, as discussed, are paid directly to the lender to reduce the interest rate on the loan. The primary goal of purchasing discount points is to achieve a lower monthly payment and reduce the overall interest paid over the loan’s duration. Borrowers typically consider discount points when they have sufficient cash reserves at closing and intend to keep the mortgage for an extended period, allowing them to recoup the upfront cost through interest savings.

Origination Points

Origination points, on the other hand, are essentially a fee charged by the lender for processing the mortgage application. They are not typically tied to a reduction in the interest rate and represent the lender’s compensation for the work involved in originating the loan. Sometimes, the term “origination fee” is used, and it can be expressed as a flat fee or a percentage of the loan amount. While origination points are a cost of getting the loan, they don’t offer the same direct benefit of interest rate reduction as discount points. However, it’s important to note that the line between origination fees and discount points can sometimes be blurred, and borrowers should carefully review their loan estimates to understand all associated charges.

Calculating the Break-Even Point

A critical consideration when deciding whether to pay lender points is the break-even point. This is the time at which the total savings from the reduced interest rate equal the upfront cost of the points paid. Calculating the break-even point helps borrowers determine if purchasing points is financially prudent based on their expected duration of homeownership and mortgage.

The Break-Even Formula and Calculation

To calculate the break-even point, one needs to consider the monthly savings and the upfront cost.

- Calculate Monthly Savings: Subtract the new monthly payment (with points) from the original monthly payment (without points).

- Calculate Total Cost of Points: Multiply the number of points by 1% of the loan amount.

- Calculate Break-Even Period: Divide the total cost of points by the monthly savings.

Let’s revisit our previous example: a $300,000 loan.

- Original loan: $300,000 at 7% interest. Monthly P&I: $1,995.90.

- Loan with one point: $300,000 at 6.75% interest. Monthly P&I: $1,946.46.

- Monthly Savings: $1,995.90 – $1,946.46 = $49.44.

- Cost of one point: 1% of $300,000 = $3,000.

- Break-Even Period: $3,000 / $49.44 ≈ 60.68 months, or approximately 5 years and 1 month.

In this scenario, if the borrower plans to keep the mortgage for longer than about 5 years, paying the point would be financially beneficial. If they anticipate selling or refinancing before then, the upfront cost might not be recouped.

Factors Influencing Break-Even

Several factors can influence the break-even point:

- Loan Term: Longer loan terms generally make paying points more attractive, as the cumulative interest savings over 30 years are more substantial.

- Interest Rate Differential: A larger reduction in the interest rate for each point paid will shorten the break-even period.

- Loan Amount: Larger loan amounts mean a higher upfront cost for points but also larger monthly interest payments, leading to greater savings with a rate reduction, which can shorten the break-even period.

- Borrower’s Time Horizon: The most crucial factor is how long the borrower intends to keep the mortgage.

When to Consider Paying Lender Points

The decision to pay lender points is not one-size-fits-all. It requires a careful analysis of personal financial circumstances, future plans, and market conditions.

Long-Term Homeowners

Individuals who are confident they will remain in their home for many years are often prime candidates for purchasing discount points. The extended period allows them to fully benefit from the reduced interest rate, maximizing their long-term savings. For a 30-year mortgage, staying in the home for 7-10 years or more often makes paying points a wise financial strategy.

Borrowers Seeking Lower Monthly Payments

Even if a borrower plans to move in a shorter timeframe, sometimes the reduction in monthly payments is a significant priority. If a lower monthly obligation is crucial for managing household budgets, improving cash flow, or freeing up funds for other investments, paying points can be a viable option, provided the break-even point is acceptable.

Refinancing Considerations

When refinancing an existing mortgage, borrowers may again encounter the option of paying points to secure a lower interest rate on the new loan. The same break-even analysis applies. If the new loan term is long and the savings are substantial, purchasing points during a refinance can be advantageous. It’s also worth noting that points paid on a refinanced mortgage are tax-deductible over the life of the new loan, similar to points on an original mortgage.

Tax Implications of Lender Points

The tax deductibility of lender points is a significant consideration for borrowers. Under current tax laws, points paid on the acquisition of a primary residence are generally tax-deductible in the year they are paid. This can offer a substantial tax benefit, effectively reducing the upfront cost of the points.

Deducting Points on Your Tax Return

To qualify for the deduction, the loan must be secured by your main home, and the points must be paid directly by you at or before closing. The lender must also report the points paid on IRS Form 1098, Mortgage Interest Statement. If these conditions are met, the points can be itemized as a deduction on Schedule A (Form 1040).

Limitations and Considerations

It’s important to consult with a tax professional for personalized advice, as tax laws can change and individual circumstances vary. There are limitations on how points can be deducted. For example, if the points paid represent a disguised fee or a commission for services beyond just lowering the interest rate, they may not be deductible. Additionally, if points are paid on a loan that is not for your primary residence, or if they are not paid directly by you (e.g., rolled into the loan amount without direct payment at closing), their deductibility may be affected. The IRS also has rules regarding the deductibility of points paid when refinancing a mortgage; these are typically deducted over the life of the new loan.

When to Avoid Paying Lender Points

While paying lender points can be a strategic move, there are scenarios where it’s not advisable.

Short-Term Homeowners

If you anticipate selling your home or refinancing your mortgage within a few years, paying points is often not a wise financial decision. The upfront cost might not be recouped through interest savings before you no longer have the mortgage. For example, if the break-even point is five years and you plan to move in three, you’ll likely lose money on the points paid.

Limited Cash Reserves

Mortgages involve numerous closing costs, and paying additional points can strain an already tight budget. If paying points means depleting your emergency fund or other essential savings, it’s generally better to avoid them and opt for a slightly higher interest rate. Maintaining adequate liquidity is crucial for financial security.

Interest Rates at Historic Lows

When interest rates are already very low, the potential for reduction through points might be minimal. In such scenarios, even a quarter-point reduction might not be enough to justify the upfront cost, especially if the lender’s offering for points-to-rate reduction is not aggressive.

Conclusion

Lender points represent a powerful tool in the mortgage financing landscape, offering borrowers the opportunity to customize their loan terms. By understanding how points work, their associated costs and benefits, and the crucial concept of the break-even point, individuals can make informed decisions that align with their financial goals and timelines. Whether to pay points is a strategic choice that balances upfront investment against long-term savings, and a careful evaluation of personal circumstances is paramount. Consulting with mortgage lenders and financial advisors can provide clarity and ensure that the path chosen leads to the most advantageous outcome for the borrower.