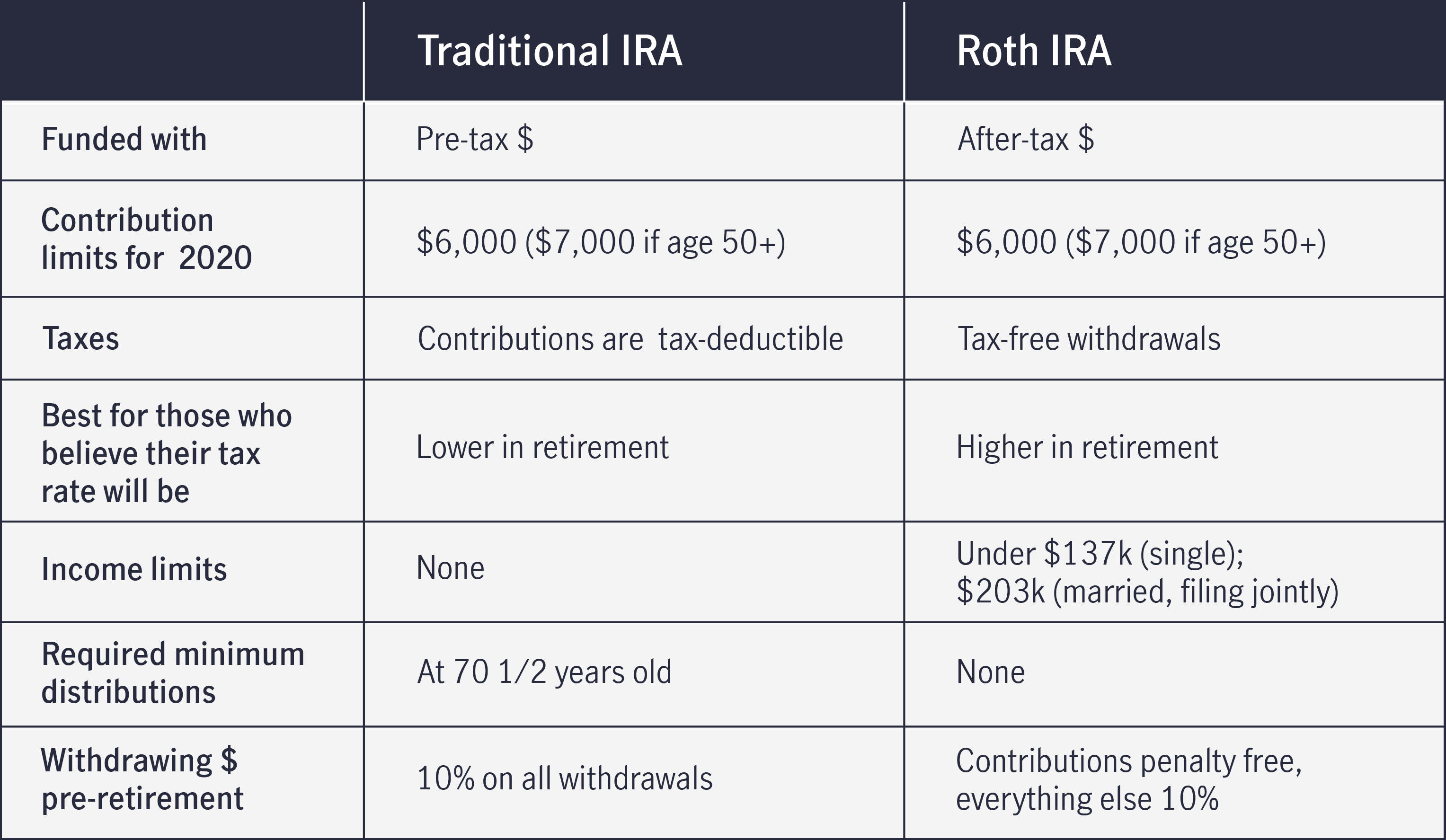

Understanding the nuances of retirement savings vehicles is crucial for effective financial planning. Among the most popular and accessible options are Individual Retirement Arrangements (IRAs), with the Traditional IRA and the Roth IRA being the two primary types. While both offer tax advantages to help individuals grow their savings for retirement, their core differences lie in when those tax benefits are realized. This distinction can significantly impact your overall tax liability during your working years and in retirement, making it essential to grasp their unique structures.

Traditional IRA: Tax-Deferred Growth

The Traditional IRA has been a cornerstone of retirement planning for decades. Its primary appeal lies in its tax-deferred growth, meaning your investments are not taxed annually. Contributions made to a Traditional IRA may be tax-deductible in the year they are made, reducing your current taxable income. This can be a significant advantage for individuals in higher tax brackets during their peak earning years.

Tax-Deductible Contributions

The deductibility of Traditional IRA contributions is subject to income limitations and whether you (or your spouse, if married) are covered by a retirement plan at work. For the 2023 tax year, if you are not covered by a retirement plan at work, your contributions are fully deductible regardless of your income. However, if you are covered by a retirement plan, the deductibility phases out as your Modified Adjusted Gross Income (MAGI) increases. For example, in 2023, the deduction begins to phase out for single filers with MAGI between $73,000 and $83,000, and for those married filing jointly, between $116,000 and $136,000. If your income exceeds these limits, your contributions may not be deductible, but the earnings will still grow tax-deferred.

Taxable Withdrawals in Retirement

The flip side of tax-deferred growth is that withdrawals made from a Traditional IRA during retirement are taxed as ordinary income. This means that while you receive a tax break now, you will pay taxes on both your contributions (if they were deductible) and all the earnings when you begin taking distributions. The tax rate applied will be your ordinary income tax rate at the time of withdrawal, which could be higher or lower than your current rate depending on your income in retirement. This unpredictability in future tax rates is a key consideration when deciding if a Traditional IRA is the right choice for you.

Required Minimum Distributions (RMDs)

Another important feature of Traditional IRAs is the requirement to take Required Minimum Distributions (RMDs) once you reach a certain age. For 2023, the age at which RMDs begin is 73. The amount of the RMD is calculated based on your account balance and your life expectancy, as determined by IRS tables. Failure to take your RMD can result in a significant penalty, typically 50% of the amount that should have been withdrawn. RMDs ensure that the government eventually collects taxes on the deferred income.

Roth IRA: Tax-Free Growth and Withdrawals

The Roth IRA offers a fundamentally different approach to retirement savings, prioritizing tax-free growth and tax-free withdrawals in retirement. Unlike the Traditional IRA, contributions to a Roth IRA are made with after-tax dollars, meaning they are not tax-deductible in the year they are made. However, this upfront tax payment is compensated by the significant advantage of tax-free growth and the ability to withdraw both contributions and earnings tax-free in retirement, provided certain conditions are met.

After-Tax Contributions

The direct consequence of not receiving a tax deduction for Roth IRA contributions is that your current taxable income is not reduced. However, this also means that you have already paid taxes on the money you are investing. This can be an attractive option for individuals who anticipate being in a higher tax bracket in retirement than they are currently, or for those who prefer the certainty of knowing their retirement income will be tax-free.

Tax-Free Qualified Withdrawals

The most significant benefit of a Roth IRA is the potential for tax-free qualified withdrawals in retirement. To qualify for tax-free withdrawals of both contributions and earnings, you must meet two conditions:

- Age Requirement: You must be at least 59 ½ years old.

- Five-Year Rule: You must have had your first Roth IRA contribution made at least five tax years prior to the withdrawal.

If these conditions are met, any amount you withdraw from your Roth IRA, including all the earnings that have accumulated over the years, will be completely free of federal income tax. This predictability can be invaluable for retirement planning, allowing you to budget more accurately without the uncertainty of future tax rates.

Contributions Can Be Withdrawn Anytime

A unique and often overlooked benefit of Roth IRAs is that your original contributions can be withdrawn at any time, for any reason, without incurring taxes or penalties. This is because you have already paid taxes on this money. While it is generally advisable to leave retirement savings untouched until retirement, this feature can provide a valuable safety net for unexpected financial emergencies, offering more flexibility than a Traditional IRA. Earnings, however, are subject to the same age and five-year rule requirements for tax-free withdrawal.

No RMDs for the Original Owner

Unlike Traditional IRAs, Roth IRAs do not have Required Minimum Distributions (RMDs) for the original owner during their lifetime. This means you are not forced to withdraw funds at a certain age, allowing your money to continue growing tax-free for as long as you wish. This can be particularly beneficial for individuals who do not need their retirement funds immediately or who want to pass on their assets to heirs. Beneficiaries of a Roth IRA are subject to RMD rules, though.

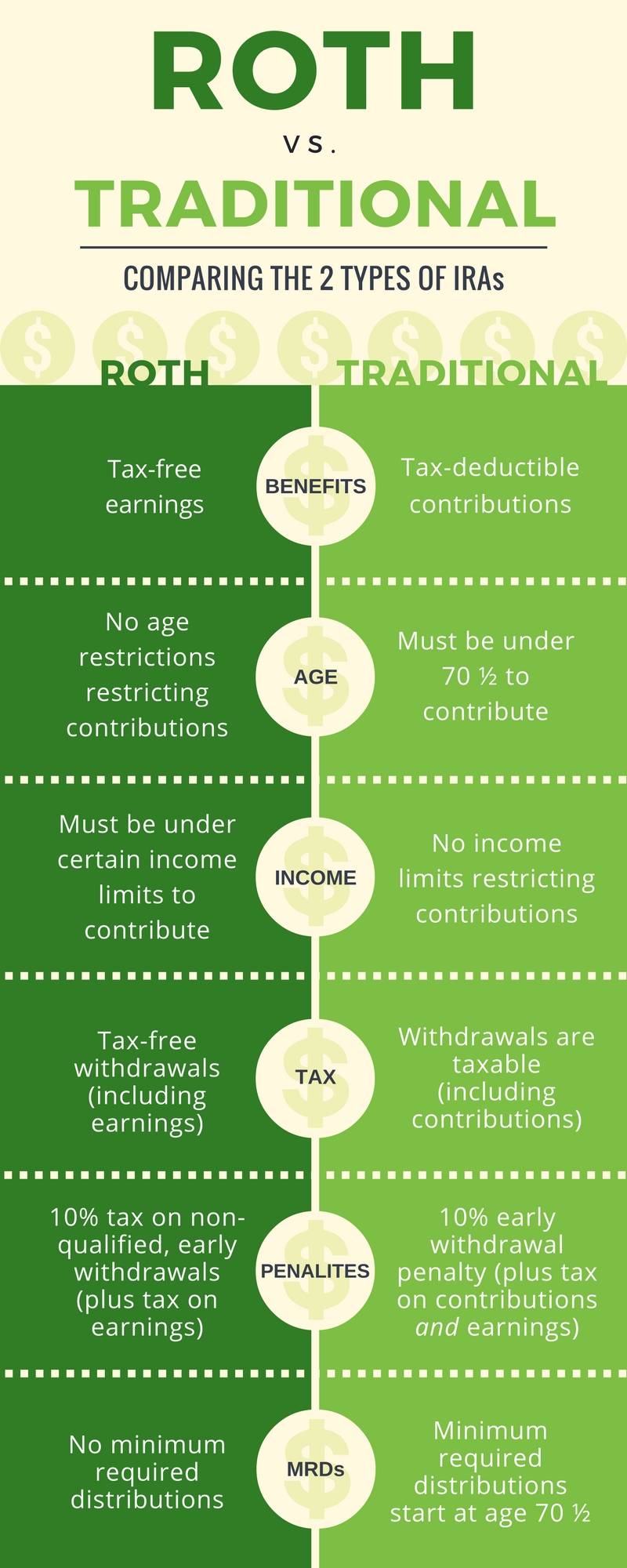

Key Differences Summarized

The core distinction between a Traditional IRA and a Roth IRA boils down to the timing of tax benefits:

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| Contributions | May be tax-deductible in the current year. | Made with after-tax dollars; not tax-deductible. |

| Tax on Growth | Tax-deferred; earnings are not taxed annually. | Tax-free; earnings grow without annual taxation. |

| Withdrawals (Qualified) | Taxed as ordinary income in retirement. | Tax-free in retirement (if age and five-year rules are met). |

| RMDs | Required starting at age 73 (as of 2023). | Not required for the original owner during their lifetime. |

| Income Limitations | Deductibility is subject to income limits if covered by a workplace retirement plan. | Contributions are subject to income limits; higher earners may not be eligible. |

| Withdrawal of Contributions | Subject to taxes and penalties if withdrawn before age 59 ½ (with exceptions). | Contributions can be withdrawn tax- and penalty-free at any time. |

Which IRA is Right for You?

The decision between a Traditional IRA and a Roth IRA is highly personal and depends on several factors, primarily your current income, your expected income in retirement, and your tax situation.

Consider a Traditional IRA if:

- You expect your tax rate to be lower in retirement than it is now. The upfront tax deduction provides immediate tax relief, which is more valuable when your current tax rate is high. If you anticipate being in a lower tax bracket in retirement, paying taxes then will be less of a burden.

- You want to reduce your current taxable income. The immediate tax deduction can lower your current tax bill, freeing up cash flow for other investments or expenses.

- Your income is too high to contribute directly to a Roth IRA. While higher earners may not be eligible for direct Roth IRA contributions, they might still be able to contribute to a Traditional IRA, though deductibility may be limited.

Consider a Roth IRA if:

- You expect your tax rate to be higher in retirement than it is now. Paying taxes on your contributions now means all your future withdrawals will be tax-free, a significant advantage if you anticipate being in a higher tax bracket when you stop working.

- You value tax diversification in retirement. Having a mix of taxable and tax-free retirement accounts can provide flexibility in managing your tax liability during your retirement years.

- You want the flexibility to withdraw contributions if needed. The ability to access your contributions penalty- and tax-free offers a valuable layer of financial security.

- You want to avoid RMDs during your lifetime. This allows for continued tax-free growth and more control over your assets.

- You are a younger individual early in your career with lower current income. The benefits of tax-free growth over a longer period can be substantial.

Contributing to Both or Converting

It’s important to note that you are not limited to choosing just one type of IRA. You can contribute to both a Traditional IRA and a Roth IRA, as long as your total contributions across all your IRAs do not exceed the annual contribution limit. For 2023, the maximum contribution limit is $6,500, with an additional catch-up contribution of $1,000 for individuals age 50 and older.

Furthermore, individuals whose income exceeds the Roth IRA contribution limits may be able to utilize a “backdoor Roth IRA” strategy. This involves contributing to a non-deductible Traditional IRA and then immediately converting it to a Roth IRA. This strategy allows higher earners to benefit from Roth IRA advantages, but it’s crucial to understand the tax implications and consult with a tax professional.

The decision of whether to contribute to a Traditional IRA, a Roth IRA, or a combination of both, requires careful consideration of your personal financial circumstances and future expectations. By understanding the fundamental differences in their tax treatments, you can make an informed choice that best aligns with your long-term retirement savings goals.