The Evolving Landscape of Drone Insurance for Tech & Innovation

The rapid advancements in drone technology, particularly within areas like AI follow mode, autonomous flight, sophisticated mapping, and remote sensing, have opened unprecedented opportunities across numerous industries. However, with innovation comes inherent risks and complexities. From accidental damage to high-value drone platforms equipped with cutting-edge sensors, to potential third-party liability arising from autonomous operations or data collection, the financial implications for operators and innovators can be substantial. As drone technology transitions from hobbyist pursuits to critical commercial and industrial tools, understanding the nuances of insurance becomes paramount. This is especially true for entities pushing the boundaries of what drones can achieve, where standard off-the-shelf policies may not adequately address the unique challenges posed by advanced operations. For those leveraging drones for mapping vast agricultural fields, conducting intricate infrastructure inspections with remote sensing, or deploying fully autonomous fleets for logistics, comprehensive risk management, underpinned by robust insurance, is not merely a safeguard—it’s a fundamental operational requirement.

Navigating the insurance landscape for these specialized applications requires a keen understanding of policy terms that go beyond basic coverage. It delves into the specifics of hull damage for sophisticated equipment, liability for data integrity in mapping, and the profound implications of autonomous system failures. Therefore, for professionals and businesses deeply embedded in the “Tech & Innovation” segment of the drone industry, grasping every facet of their insurance coverage is essential for sustainable growth and mitigating unforeseen financial exposures. It is within this intricate framework that terms like “deductible” and “coinsurance” take on a critical role, directly impacting an operator’s out-of-pocket costs following an insured event.

Demystifying “20 After Deductible” in Drone Coverage

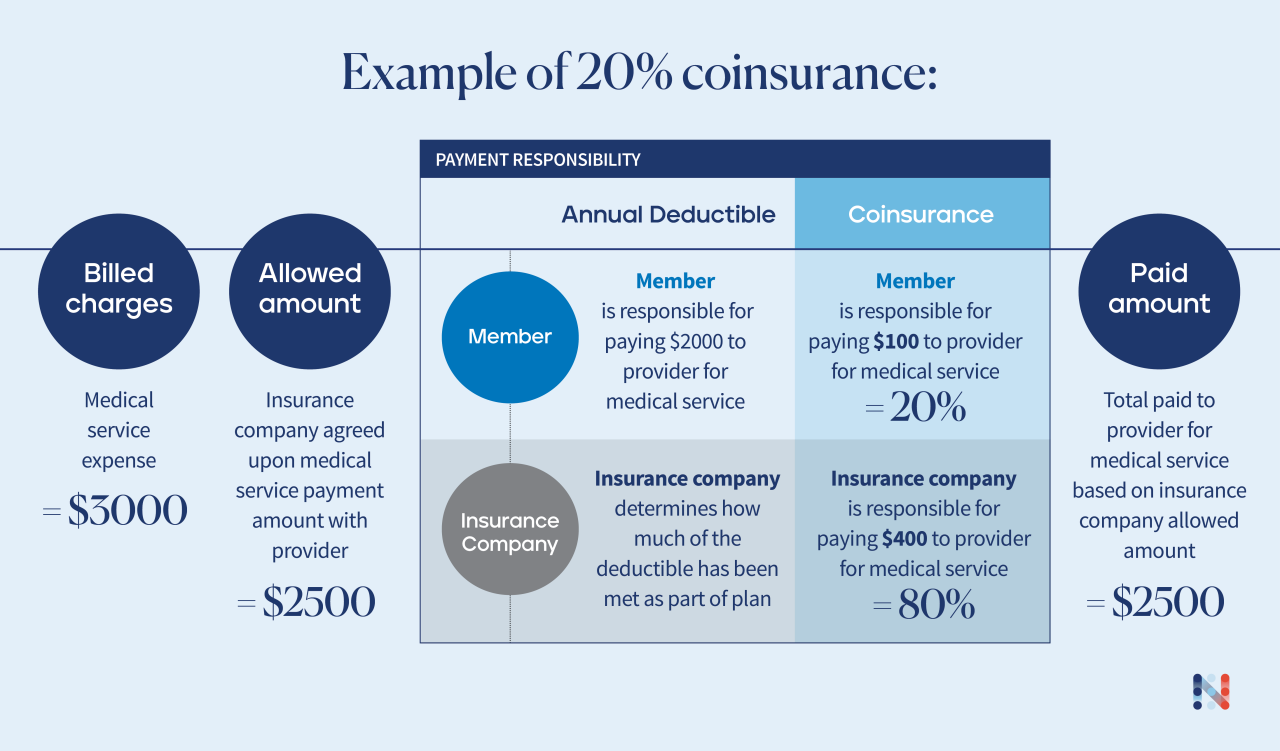

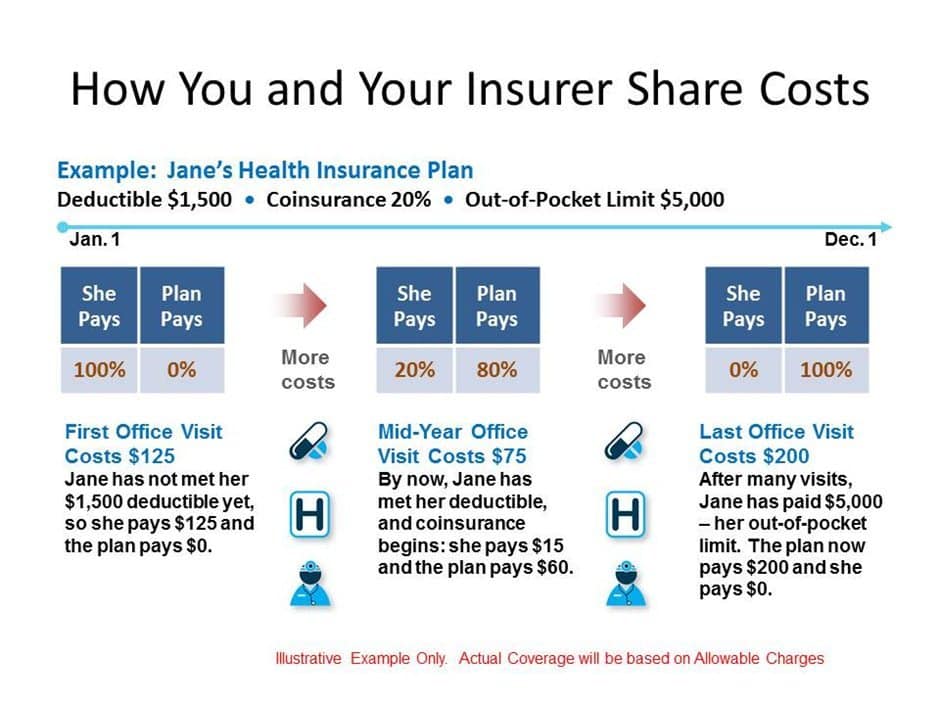

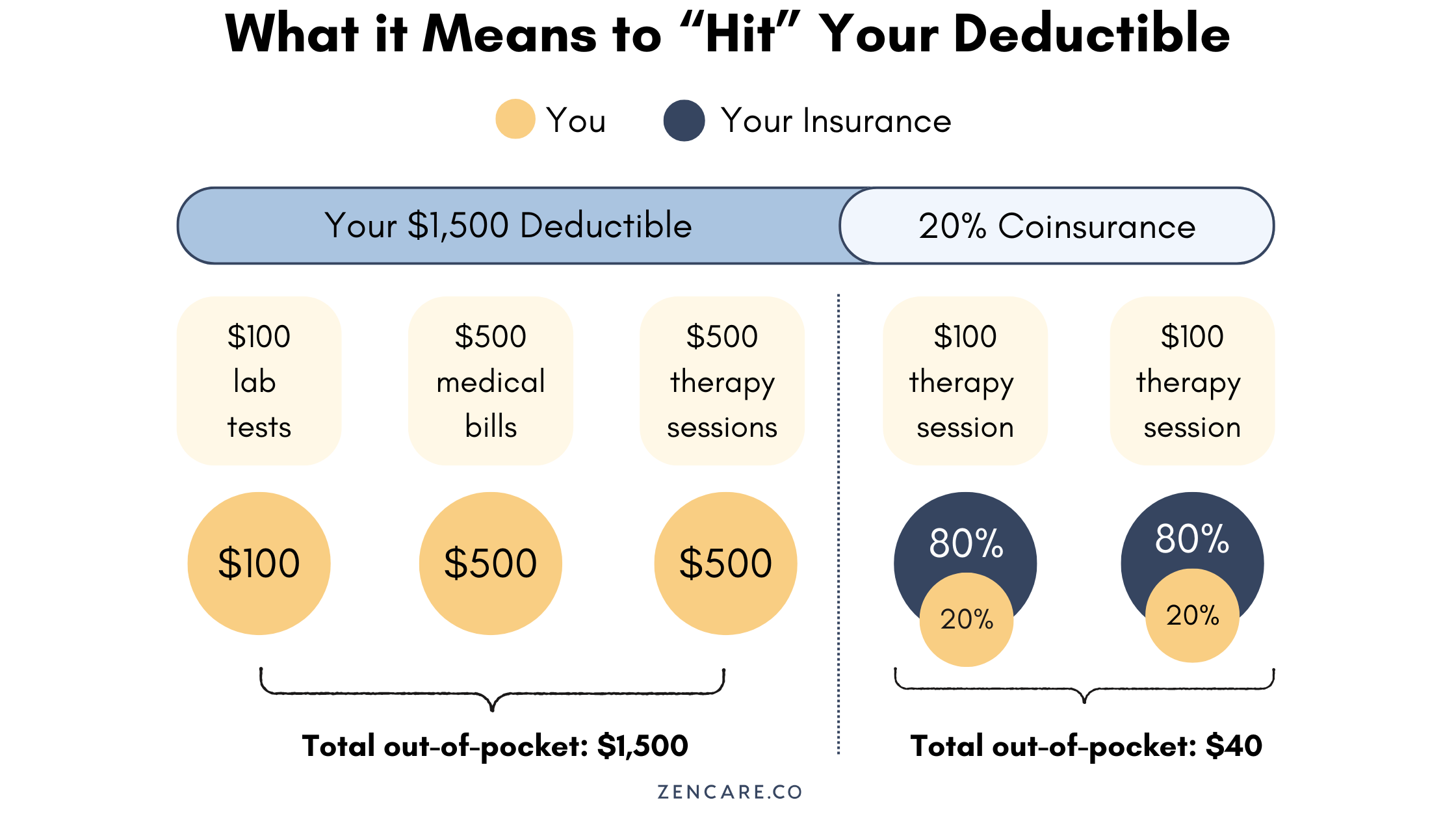

When an insurance policy for a drone or its advanced operations mentions “20 after deductible,” it refers to a common insurance principle known as coinsurance. This term delineates the percentage of an insured loss that an policyholder is responsible for paying after their deductible has been met. In essence, the deductible is the initial amount you must pay out-of-pocket for a covered claim before your insurance company starts contributing. Once that deductible threshold is reached, coinsurance kicks in, dictating the shared responsibility for the remaining costs.

For example, if a high-value drone used for advanced remote sensing suffers $10,000 in covered damage, and your policy has a $1,000 deductible with “20 after deductible” coinsurance:

- You would first pay the $1,000 deductible.

- The remaining cost is $10,000 – $1,000 = $9,000.

- Your coinsurance of 20% would apply to this remaining $9,000, meaning you pay 20% of $9,000, which is $1,800.

- The insurance company would then cover the remaining 80% of $9,000, which is $7,200.

- Your total out-of-pocket cost for this claim would be the $1,000 deductible plus the $1,800 coinsurance, totaling $2,800.

This structure is designed to share the risk between the insurer and the insured, incentivizing careful operation and maintenance while making insurance premiums more manageable. For drone businesses relying on expensive, cutting-edge technology—such as thermal imaging payloads for industrial inspection or LiDAR systems for precision mapping—understanding these financial responsibilities before an incident occurs is crucial for budgeting and operational resilience. A minor incident could still result in significant out-of-pocket expenses if the operator is unaware of their coinsurance obligations, potentially impacting their ability to quickly replace or repair critical equipment and resume operations.

Understanding Deductibles in High-Tech Drone Policies

Deductibles for drone insurance can vary significantly based on the value of the drone, its payload, the nature of operations (e.g., autonomous flights versus manual), and the perceived risk. For highly specialized drones engaged in advanced mapping or remote sensing, which may cost tens or hundreds of thousands of dollars, deductibles could range from several hundred to several thousand dollars. Policies often feature separate deductibles for hull damage (damage to the drone itself) and liability claims (damage or injury to third parties). Innovators and operators must carefully evaluate deductible amounts in relation to their financial capacity and risk tolerance, especially when dealing with experimental technologies or high-stakes projects. A higher deductible typically results in lower premiums, but also means greater out-of-pocket expense in the event of a claim.

The Role of Coinsurance in Advanced Operations

Coinsurance rates like “20 after deductible” are not arbitrary; they reflect the insurer’s assessment of risk associated with particular drone technologies and their applications. For instance, an insurer might apply a higher coinsurance rate to experimental autonomous flight programs due to the elevated, often unquantified, risks involved, or for operations in challenging environments with complex remote sensing equipment. Conversely, a well-established mapping operation with a proven safety record might qualify for more favorable coinsurance terms. Operators in the Tech & Innovation space must engage with their insurance providers to understand how their specific technological applications and operational procedures influence these critical policy components. This dialogue ensures that coverage accurately reflects the unique risk profile of their advanced drone endeavors.

Navigating Insurance for Autonomous Flight and AI Integration

The frontier of autonomous flight and AI integration in drones presents a unique set of challenges for insurance providers and policyholders. As drones become more independent, making real-time decisions using AI for navigation, obstacle avoidance, and mission execution (e.g., AI follow mode for cinematic shots or autonomous inspection routes), the traditional understanding of fault and liability can become blurred. If an AI-driven drone causes property damage or injury, determining whether the fault lies with the software developer, the operator, the hardware manufacturer, or a combination, requires sophisticated legal and technical analysis.

Insurance policies for autonomous and AI-integrated drones must specifically address these complex liability scenarios. While a “20 after deductible” clause still applies to the physical damage to the drone (hull coverage), the more significant concern often revolves around third-party liability coverage for incidents caused by autonomous operation. Innovators developing or deploying such systems need policies that include robust coverage for:

- Product Liability: If a fault in the AI software or autonomous system leads to an incident.

- Operational Liability: If the autonomous system, while functioning as intended, causes an incident due to unforeseen environmental factors or misinterpretation.

- Data Breach/Privacy Liability: As autonomous drones often collect vast amounts of data, a breach could lead to significant legal exposure.

Understanding the “20 after deductible” for hull coverage is straightforward, but the intricate web of liability insurance for autonomous systems requires detailed scrutiny. Operators must ensure their policies explicitly cover autonomous flight and AI decision-making risks, rather than relying on generic drone liability which might have exclusions for unpiloted operations beyond visual line of sight or AI-driven decision failures.

Protecting Your Investment in Mapping and Remote Sensing Operations

Drones equipped for mapping and remote sensing are often multi-faceted investments, comprising the drone platform itself, high-resolution cameras, LiDAR scanners, hyperspectral sensors, and sophisticated data processing units. A single incident involving such a system can lead to substantial financial losses, not only from the damage to the equipment but also from the disruption of critical data collection schedules and potential contractual penalties. For these operations, the “20 after deductible” clause directly impacts the cost of repair or replacement for these valuable assets.

Consider a professional mapping firm that uses a drone with a specialized LiDAR payload for surveying. If this drone experiences a hard landing due to a GPS glitch, resulting in $25,000 worth of damage to both the airframe and the payload, and their policy has a $2,000 deductible with 20% coinsurance:

- They pay the $2,000 deductible.

- Remaining cost: $23,000.

- Their 20% coinsurance on $23,000 is $4,600.

- The insurer pays $18,400.

- Total out-of-pocket: $2,000 + $4,600 = $6,600.

This example underscores the importance of not just having insurance, but understanding its financial mechanics. For businesses whose core service relies on mapping and remote sensing data, ensuring that both the drone platform and its expensive payloads are adequately covered is non-negotiable. Policies should clarify how components are valued (replacement cost vs. actual cash value) and whether specific high-value sensors are itemized and insured separately. Additionally, firms engaged in remote sensing may also need professional liability or errors and omissions insurance to cover potential claims arising from inaccurate data or mapping errors that lead to financial loss for their clients. While “20 after deductible” might not apply to these specific liability policies, understanding its impact on hull coverage is vital for maintaining operational continuity.

Strategic Risk Management for Drone Innovators

For businesses at the forefront of drone technology and innovation, risk management extends beyond simply purchasing an insurance policy. It involves a holistic approach that integrates safety protocols, operational best practices, and a deep understanding of potential liabilities inherent in new technologies. Knowing what “20 after deductible” means is just one piece of this puzzle, albeit a critical financial one. Strategic risk management for drone innovators includes:

Proactive Safety Protocols and Training

Implementing rigorous training programs for operators, especially those managing autonomous flights or complex remote sensing missions, can significantly reduce the likelihood of incidents. Comprehensive pre-flight checks, adherence to regulatory guidelines, and ongoing education about new technologies and their operational nuances are paramount. Insurers often look favorably upon businesses with demonstrably strong safety cultures, which can sometimes translate into better policy terms, including more favorable coinsurance rates or lower deductibles.

Detailed Policy Review and Customization

Standard drone insurance policies may not adequately cover the unique risks associated with experimental AI, specialized payloads, or novel applications. Innovators must work closely with experienced insurance brokers to customize policies that accurately reflect their operations. This includes specifying coverage for R&D phases, testing of autonomous systems, and the specific liabilities associated with data collection and processing in mapping and remote sensing. Explicitly confirming how “20 after deductible” applies to various components and scenarios within a customized policy prevents future surprises.

Financial Preparedness for Out-of-Pocket Expenses

Even with comprehensive insurance, businesses must be prepared for the out-of-pocket costs associated with deductibles and coinsurance. Budgeting for these potential expenses as part of an operational contingency plan is crucial. For companies running lean operations or those heavily invested in R&D, an unexpected several thousand dollar expense from an incident could significantly impact cash flow or project timelines.

By meticulously understanding terms like “20 after deductible” and integrating this knowledge into a broader risk management strategy, drone innovators can not only protect their significant investments in advanced technology but also foster a more resilient and sustainable operational framework. This ensures that the promise of AI, autonomous flight, precision mapping, and remote sensing can be realized without being derailed by unforeseen financial burdens.