Medicaid, the vital public health insurance program in the United States, provides crucial medical assistance to low-income individuals and families. While many associate Medicaid with direct eligibility based on income and asset thresholds, a less understood but equally critical pathway to qualification for long-term care services is the “Medicaid spend down.” This mechanism allows individuals who exceed the standard income limits to become eligible for Medicaid by incurring medical expenses equal to their excess income. Far from a simple financial transaction, the spend down is a sophisticated and often complex process, demanding strategic understanding and careful management to navigate effectively. It represents an intricate system designed to balance access to essential care with fiscal responsibility, touching upon principles of resource allocation and eligibility determination that, in a broader sense, echo the precision required in any complex system optimization.

Unpacking the Fundamentals of Medicaid Eligibility

Before delving into the mechanics of a spend down, it’s essential to grasp the foundational principles of Medicaid eligibility, particularly concerning long-term care. Medicaid is administered at the state level, within federal guidelines, leading to variations in rules and limits across jurisdictions. However, core concepts remain consistent, underpinning the need for the spend down provision.

Income and Asset Thresholds

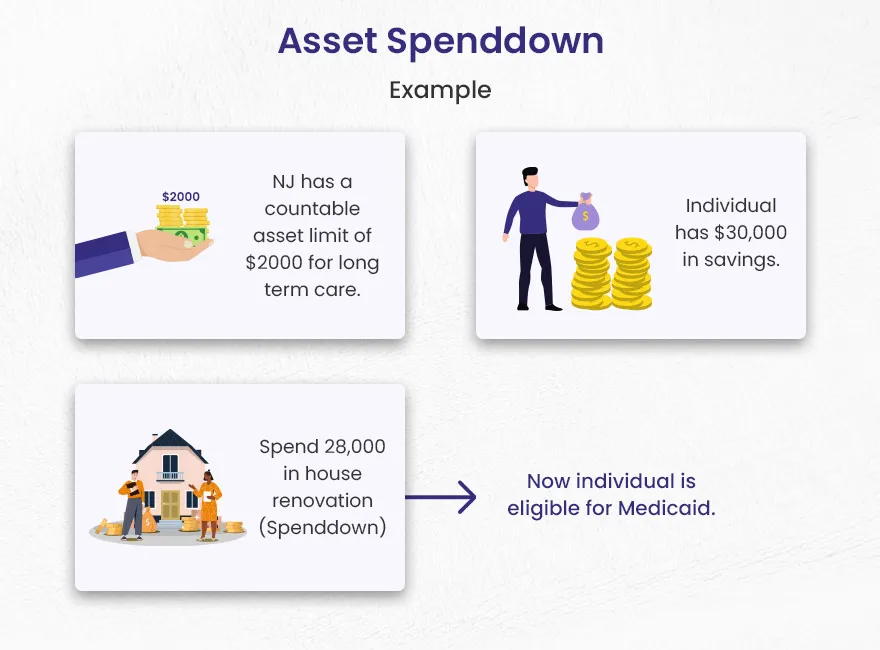

For most Medicaid programs, individuals must meet specific income and asset limits. These limits are typically quite stringent, especially for long-term care Medicaid (often referred to as institutional Medicaid or Home and Community-Based Services waivers). Assets include resources like bank accounts, investments, real estate (excluding a primary residence under certain conditions), and other liquid or convertible holdings. Income includes wages, pensions, Social Security benefits, and other regular payments. For individuals needing nursing home care or extensive in-home services, the costs can quickly deplete even substantial savings. The spend down is specifically designed for those whose income exceeds the Medicaid limit but whose medical expenses are so high that, once paid, their effective income falls below the threshold. This process is akin to a complex filtering system, where certain input criteria (income, expenses) are processed to determine an output (eligibility).

The Critical Role of Long-Term Care

Long-term care, such as nursing home services, assisted living, or extensive home health care, is incredibly expensive. Medicare, the primary health insurance for seniors, generally does not cover custodial long-term care, leaving individuals and families vulnerable to catastrophic costs. Medicaid often serves as the payer of last resort for these services. However, due to its means-tested nature, many middle-income seniors find themselves in a challenging “gap” – too “rich” for immediate Medicaid eligibility, yet not wealthy enough to self-fund years of expensive care without impoverishing themselves. The spend down offers a structured pathway through this gap, providing a bridge to necessary financial support. It’s a critical component in the overall architecture of healthcare financing for an aging population, demanding efficient processing and clear guidelines for those navigating its complexities.

The Mechanics of the Spend Down Process

The core of a Medicaid spend down involves demonstrating that an individual’s “excess income” has been used to pay for medical expenses, thereby reducing their countable income to the Medicaid-allowable level. This isn’t about spending down assets, which is a separate but related concept often involving asset protection strategies. The spend down primarily addresses income.

Calculating the Medically Needy Income Limit (MNIL)

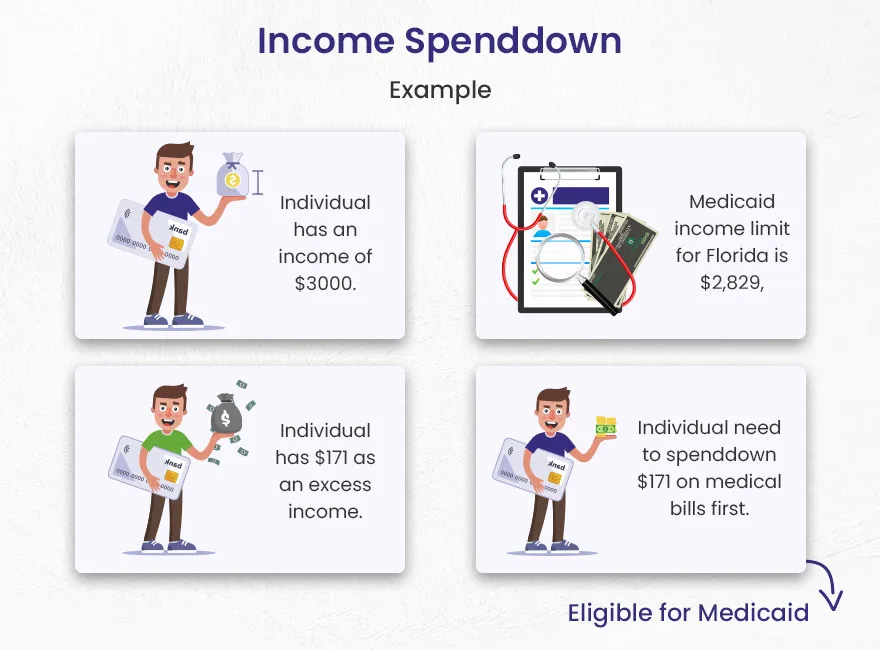

Each state establishes a Medically Needy Income Limit (MNIL), which is the maximum income an individual can have to qualify for Medicaid after factoring in medical expenses. If an applicant’s monthly income exceeds the MNIL, the difference is considered their “excess” or “share of cost” income. This excess amount must be “spent down” on qualified medical expenses before Medicaid benefits will kick in for the remainder of the month. It’s a calculated threshold system, where an algorithm determines the pivot point for eligibility. The system essentially looks at an individual’s financial inputs, calculates the deviation from a set standard, and requires specific actions to normalize the deviation for system entry.

Permitted Deductions and Qualified Expenses

The key to a successful spend down lies in understanding what expenses can be counted. Generally, these include:

- Medical Insurance Premiums: Medicare Part B and D premiums, supplemental insurance premiums, and long-term care insurance premiums.

- Medical Bills: Unpaid bills from doctors, hospitals, pharmacies, therapists, and other healthcare providers.

- Prescription Drugs: Costs for necessary medications.

- Deductibles and Co-payments: Out-of-pocket costs not covered by other insurance.

- Nursing Home or Home Care Costs: A significant portion of the monthly cost for these services can be applied towards the spend down.

Crucially, these expenses must be incurred by the applicant or their spouse. Bills paid by a third party, unless that third party is being reimbursed by the applicant, generally do not count. The system processes these deductions sequentially against the excess income, calculating a running total until the spend down amount is met. This iterative process mirrors data processing in technical systems, where inputs are continuously evaluated against predefined criteria.

Illustrative Scenarios and Practical Application

Consider an individual with a monthly income of $2,500 in a state where the MNIL is $1,000. Their excess income is $1,500. To qualify for Medicaid, they must incur $1,500 in qualified medical expenses each month. This might involve paying their Medicare premium, covering prescription costs, and allocating a portion of their nursing home bill. Once they’ve documented $1,500 in expenses, Medicaid will cover the remaining approved medical costs for that month. This cycle repeats monthly, requiring consistent tracking and submission of documentation. It’s a recurring compliance loop, demanding precision and diligent record-keeping, much like monitoring and adjusting parameters within an automated system.

Strategic Considerations and Navigating the System

Successfully managing a Medicaid spend down requires more than just understanding the rules; it demands strategic planning and, often, expert guidance. The intricacies of state-specific regulations and the dynamic nature of an individual’s health needs can make this process a formidable challenge.

Asset Protection and Planning Tools

While the spend down primarily concerns income, comprehensive Medicaid planning often involves asset protection strategies. This includes techniques like establishing certain types of trusts (e.g., irrevocable trusts), gifting assets within look-back periods, and utilizing Medicaid-compliant annuities. These tools are designed to reduce countable assets below Medicaid thresholds, complementing the income spend down process. Integrating these strategies with the income spend down creates a holistic approach to eligibility, akin to designing an interconnected system where multiple modules work in concert to achieve a complex objective.

The Importance of Professional Guidance

Due to the complexity of Medicaid rules and the significant financial implications, seeking advice from an elder law attorney or a qualified Medicaid planner is highly recommended. These professionals can provide invaluable guidance on state-specific regulations, assist with asset protection, help identify qualifying expenses, and ensure proper documentation. Their expertise is crucial in optimizing the spend down process, minimizing errors, and ensuring continuous eligibility. They act as system architects and navigators, interpreting complex rules and designing pathways for optimal outcomes.

Continuous Optimization and Compliance

The spend down process is not a one-time event; it’s an ongoing monthly requirement. This necessitates meticulous record-keeping, consistent monitoring of medical expenses, and proactive communication with Medicaid agencies. Any changes in income, assets, or medical needs can impact eligibility and the required spend down amount. Continuous compliance and periodic review of the financial situation are vital for uninterrupted Medicaid coverage. This aspect highlights the need for robust data management and an adaptive strategy, similar to how advanced systems require continuous calibration and performance monitoring to maintain efficiency and effectiveness.

Societal Impact and Future of Spend Down Policies

The Medicaid spend down mechanism plays a critical role in the broader landscape of healthcare finance, enabling access to long-term care for countless Americans who would otherwise face financial ruin. Its design reflects an attempt to create an equitable, albeit complex, system for resource allocation within a public assistance framework.

Balancing Access and Fiscal Responsibility

The spend down provision seeks to strike a delicate balance: ensuring that individuals with significant medical needs can access care, while also preventing those with substantial means from inappropriately relying on public funds. It’s a policy instrument designed to manage a finite pool of resources, a challenge often faced in any large-scale system where demand must meet supply under specific constraints. The ongoing debate around healthcare costs and public spending continually influences these policies, necessitating thoughtful adjustments to maintain the system’s integrity and responsiveness.

Potential for Systemic Enhancements

As healthcare systems evolve and technological capabilities advance, there is potential for enhancing the efficiency and user-friendliness of the Medicaid spend down process. Digital platforms for expense tracking, automated eligibility verification (while maintaining necessary oversight), and more streamlined documentation submission could reduce administrative burdens for both applicants and state agencies. Innovations in data analytics could also help identify trends and areas for policy refinement, ensuring the spend down mechanism remains a relevant and effective component of Medicaid in the face of changing demographics and healthcare demands. Exploring intelligent processing and transparent financial tracking could transform how individuals interact with and benefit from this essential social safety net.