For individuals and businesses operating unmanned aerial vehicles (UAVs), commonly known as drones, understanding the intricacies of insurance is paramount. Whether you’re a hobbyist with an advanced quadcopter or a commercial enterprise utilizing a fleet of specialized drones for mapping, inspections, or aerial filmmaking, the need for robust insurance coverage is undeniable. Central to verifying the legitimacy and reliability of any insurance provider is the National Association of Insurance Commissioners (NAIC) number. This seemingly innocuous numerical identifier serves as a cornerstone of regulatory oversight within the U.S. insurance industry, offering a critical layer of transparency and protection for consumers – including drone operators seeking specialized policies.

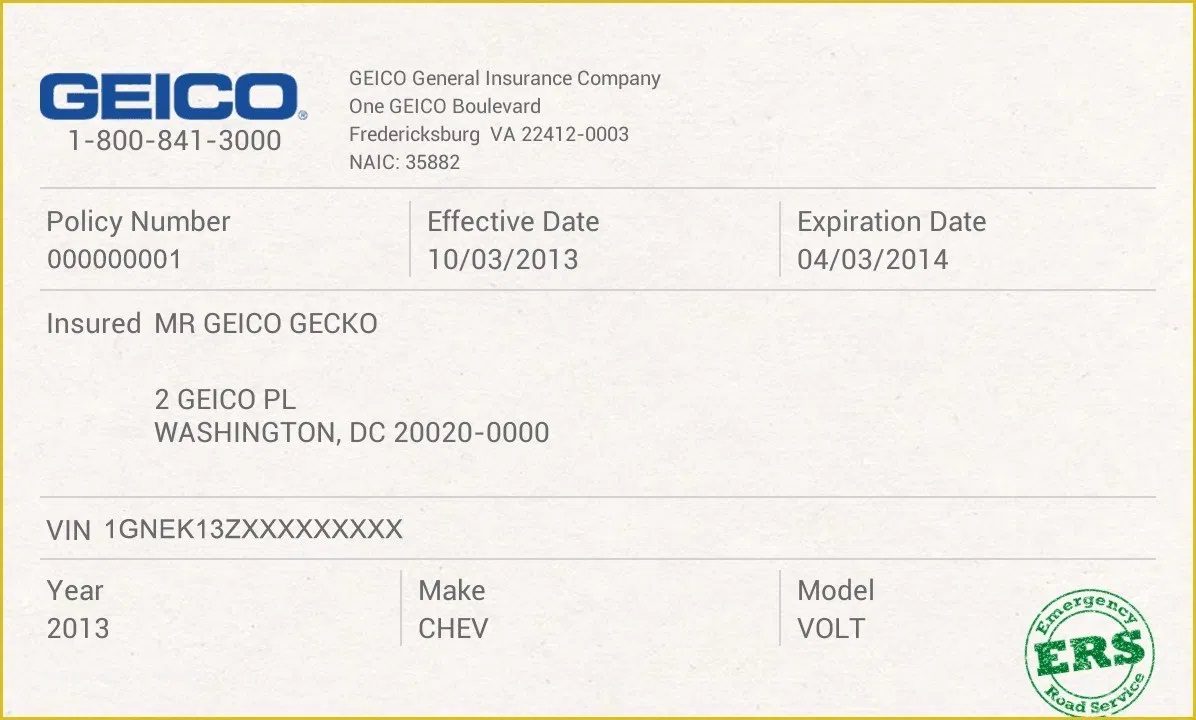

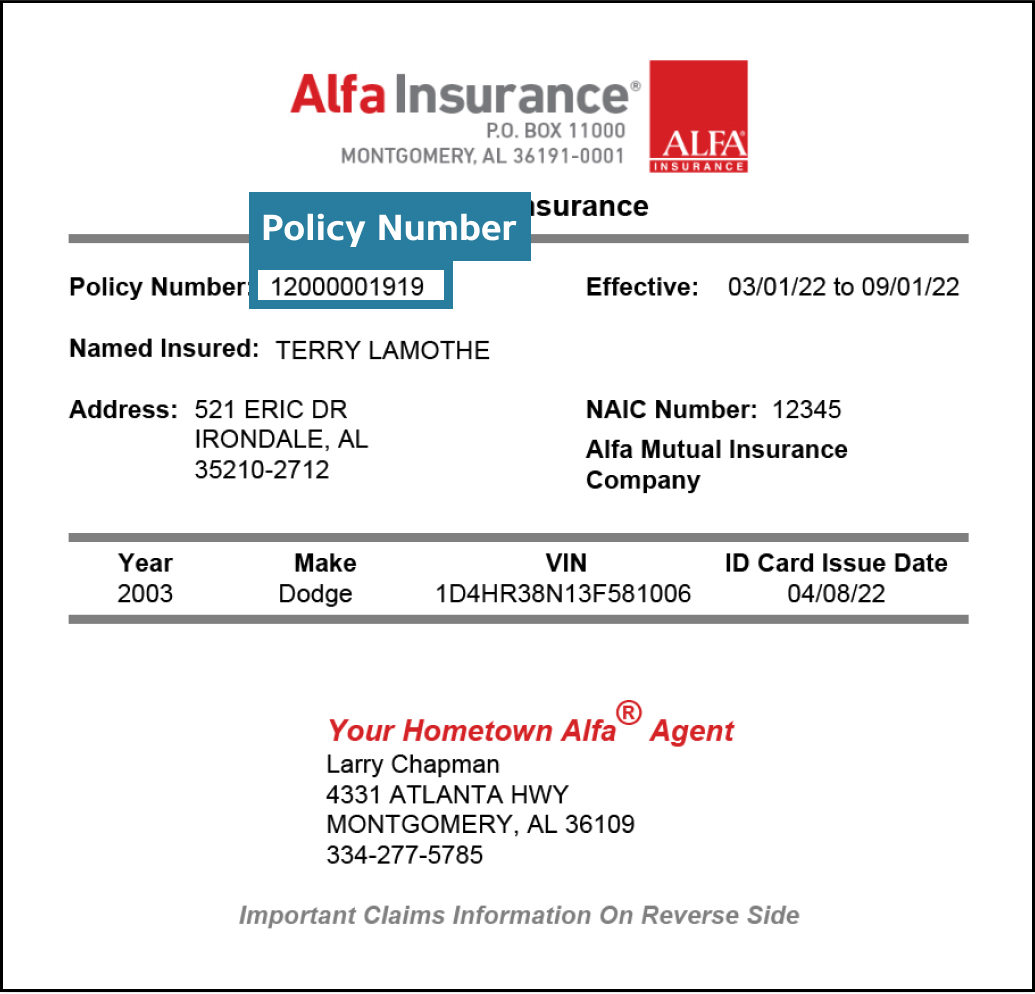

An NAIC number is a unique five-digit code assigned by the NAIC to every insurance company operating in the United States. Its primary purpose is to identify and track insurance companies, facilitating regulatory oversight, data collection, and consumer protection across state lines. While the NAIC itself is not a regulatory body that issues licenses or enforces laws (that responsibility falls to individual state departments of insurance), it plays a crucial role in harmonizing insurance regulations, developing model laws, and providing resources that enable effective state-based regulation. For drone pilots and businesses, understanding what an NAIC number signifies can be the first step in making informed decisions about their drone insurance providers, ensuring they are dealing with reputable and financially stable entities.

The Role of NAIC in the Broader Insurance Landscape

The National Association of Insurance Commissioners (NAIC) is an organization of the chief insurance regulators from the 50 states, the District of Columbia, and five U.S. territories. Its mission is to protect public interest, promote competitive markets, facilitate the fair and equitable treatment of consumers, and promote the reliability of the insurance industry. The NAIC achieves these goals through various initiatives, including the development of uniform financial standards, statutory accounting principles, and best practices for market conduct. This collaborative effort helps to create a consistent regulatory environment across the nation, which is particularly beneficial for emerging industries like commercial drone operations that often span multiple jurisdictions.

Ensuring Regulatory Compliance and Consumer Protection

The NAIC provides a vast array of data and tools that state regulators use to monitor the financial solvency of insurance companies and ensure they comply with state laws. By assigning a unique NAIC number to each insurer, the organization creates a standardized system for identifying and tracking companies. This numbering system is fundamental to the NAIC’s comprehensive databases, which house critical information such as financial statements, regulatory actions, and consumer complaints. For drone operators, this translates into an added layer of security. When seeking hull coverage for an expensive UAV or liability insurance for high-risk aerial operations, knowing that their chosen insurer is transparently identifiable through an NAIC number allows for due diligence that extends beyond simply comparing premiums. It allows access to public information that can reveal an insurer’s financial health and regulatory standing.

Identifying Licensed Insurers and Their Offerings

One of the most practical applications of the NAIC number for drone enthusiasts and professionals is its use in identifying licensed insurers. The NAIC website offers a company search tool that allows anyone to look up an insurance company by its name or NAIC number. This search can reveal crucial details, including the states where the company is licensed to operate, its financial ratings, and its history of consumer complaints. For a drone business, perhaps headquartered in one state but operating projects in several others, verifying that an insurer is licensed in all relevant states is non-negotiable. An NAIC number provides a direct pathway to confirm this legitimacy, mitigating the risk of purchasing coverage from an unauthorized or unreliable provider. This is especially vital in the specialized field of drone insurance, where policies often need to be tailored to specific operational risks, such as flights over populated areas, night operations, or the use of heavy-lift UAVs.

NAIC Numbers and Drone Insurance: A Critical Connection

The specialized nature of drone operations introduces unique risks that traditional insurance policies may not adequately cover. From the potential for property damage or bodily injury in the event of an accident to data privacy concerns associated with aerial surveillance, drone pilots require comprehensive coverage. This demand has led to the proliferation of specialized drone insurance providers, some of which are established insurers expanding their offerings, while others are newer, niche players. Regardless of the provider, their NAIC number is a crucial piece of information for any discerning drone operator.

Navigating Liability and Hull Coverage for UAVs

Drone insurance typically falls into two main categories: liability coverage and hull coverage. Liability insurance protects the drone operator from financial responsibility for damages or injuries to third parties caused by their drone. This is often mandated by regulatory bodies like the FAA for commercial operations. Hull coverage, on the other hand, protects the drone itself from physical damage, theft, or loss. Given the significant investment in advanced drones, from intricate FPV racing drones to high-tech professional surveying UAVs, both types of coverage are essential. When researching potential insurers for these critical coverages, the NAIC number provides a benchmark for evaluating the company’s overall standing and trustworthiness within the broader insurance industry.

Why Your Drone Insurance Provider’s NAIC Number Matters

The NAIC number isn’t just a regulatory formality; it’s a direct indicator of an insurer’s legitimacy and accountability. For drone operators, this means:

- Verification of Licensing: An NAIC number allows you to confirm that the insurance company is properly licensed to sell insurance in your state (and any other states where you operate your drone business). Operating with an unlicensed insurer could render your policy invalid, leaving you exposed to significant financial risk in the event of an incident.

- Access to Financial Health Data: The NAIC collects extensive financial data from all companies with an NAIC number. This data, often aggregated and rated by independent agencies, provides insights into an insurer’s financial stability and ability to pay claims. For a drone business with a high-value fleet and potentially high-stakes operations, partnering with a financially sound insurer is non-negotiable.

- Consumer Complaint History: The NAIC maintains a database of consumer complaints against insurance companies. Checking this record using an NAIC number can reveal a pattern of poor customer service, slow claims processing, or unfair practices. For a drone operator, swift and fair claims handling is critical, especially when a damaged drone means lost revenue.

- Regulatory Scrutiny: Companies with NAIC numbers are subject to the regulatory oversight of state insurance departments. This means they operate under a framework designed to protect consumers and maintain fair market practices. Choosing an insurer without an NAIC number, or one with a problematic regulatory history, is an unnecessary risk in a field that already carries inherent operational risks.

Verifying Your Drone Insurer’s Legitimacy

Before committing to any drone insurance policy, due diligence is paramount. The NAIC’s Company Search tool is a freely available resource that empowers drone operators to verify their prospective insurer. Simply enter the company’s name or its NAIC number (which should be readily provided by any legitimate insurer). The results will confirm the company’s existence, its licensing status in various states, and provide access to its financial data and complaint history. This step should be as routine as checking a drone’s pre-flight checklist, ensuring that the ground support (your insurance) is as reliable as your aerial technology.

Types of Drone Insurance Policies

Beyond the foundational understanding of NAIC numbers, drone operators must also grasp the specifics of available insurance policies to secure appropriate protection for their aerial assets and operations. The burgeoning drone industry has spurred innovation in insurance products, offering tailored solutions for diverse needs.

Public Liability Insurance for Commercial Drone Operations

For commercial drone pilots, public liability insurance is often the most critical coverage and, in many jurisdictions, a legal requirement. This policy covers the legal costs and compensation payments that may arise if your drone causes injury to a third party or damages their property. Given the potential for drones to malfunction, lose control, or simply be misoperated, the financial implications of an incident can be devastating without adequate liability protection. Policies are typically structured to provide coverage limits appropriate for the scale and risk level of the operation, from a small-scale aerial photographer to a large industrial inspection firm.

Hull Coverage: Protecting Your Drone Investment

High-end drones, especially those equipped with advanced cameras, LiDAR sensors, or specialized payloads, represent significant capital investments. Hull coverage is designed to protect this investment, covering the cost of repair or replacement if the drone is damaged, lost, or stolen. This can include damage sustained during flight, transport, or even while stored. Some policies offer “all-risk” coverage, while others may have specific exclusions. Understanding the scope of hull coverage is vital, particularly for businesses that rely on their drones for daily operations, where downtime due to damage can lead to substantial financial losses.

Personal vs. Commercial Drone Insurance Considerations

The distinction between personal (recreational) and commercial drone use is paramount for insurance purposes. While hobbyists may be covered by existing homeowner’s policies for very limited liability, specialized drone insurance is almost always recommended, and often legally required, for commercial operations. Commercial policies typically have higher liability limits, cover a wider range of risks associated with professional use, and may include endorsements for specific activities like night flying, international travel, or operations near airports. Recreational drone flyers, even if not legally mandated, should consider personal drone insurance to protect against unforeseen accidents and property damage, as even a small consumer drone can cause significant harm.

Selecting the Right Drone Insurance Partner

Choosing the right drone insurance provider is not merely about finding the lowest premium; it’s about securing a partnership that offers comprehensive coverage, reliable claims service, and financial stability. Leveraging the NAIC framework provides a robust method for evaluating potential insurers.

Beyond the Premium: What to Look for in a Drone Insurer

While cost is always a factor, drone operators should prioritize several key aspects when selecting an insurer:

- Coverage Scope: Does the policy genuinely cover all your operational risks, including specific payloads, flight environments, and regulatory compliance?

- Claims Process: Is the claims process clear, efficient, and fair? Researching an insurer’s NAIC complaint history can provide valuable insights here.

- Customer Service: Do they offer knowledgeable support for drone-specific insurance questions?

- Flexibility: Can the policy be easily adjusted as your drone operations evolve or expand?

- Financial Strength: An insurer’s ability to pay out large claims is critical. Financial ratings from agencies like A.M. Best, Moody’s, or S&P, often accessible through NAIC company searches, are key indicators.

The Importance of a Strong Underwriter

Behind every insurance policy is an underwriter who assesses risk and determines premiums. In the specialized field of drone insurance, having an underwriter with deep understanding of UAV technology, aviation regulations, and specific operational hazards is invaluable. A strong underwriter can structure policies that accurately reflect risk, avoiding unnecessary exclusions or inadequate coverage. Their expertise, often backed by comprehensive data analysis and actuarial science, is a hallmark of a reputable insurance company – one whose NAIC record will demonstrate a history of stable operation and fair dealings.

Due Diligence: Using the NAIC Database for Informed Decisions

Ultimately, the NAIC number and the resources it unlocks empower drone operators to make informed, data-driven decisions about their insurance. By using the NAIC’s company search tool, checking financial data, reviewing complaint histories, and verifying licensing, you can move beyond relying solely on sales pitches. This due diligence ensures that your drone insurance partner is not only offering a competitive policy but is also a financially sound, ethically operating, and properly regulated entity that will be there to support your operations when it matters most. In an industry as dynamic and innovative as drone technology, ensuring your insurance foundation is solid is just as critical as the flight readiness of your UAVs.