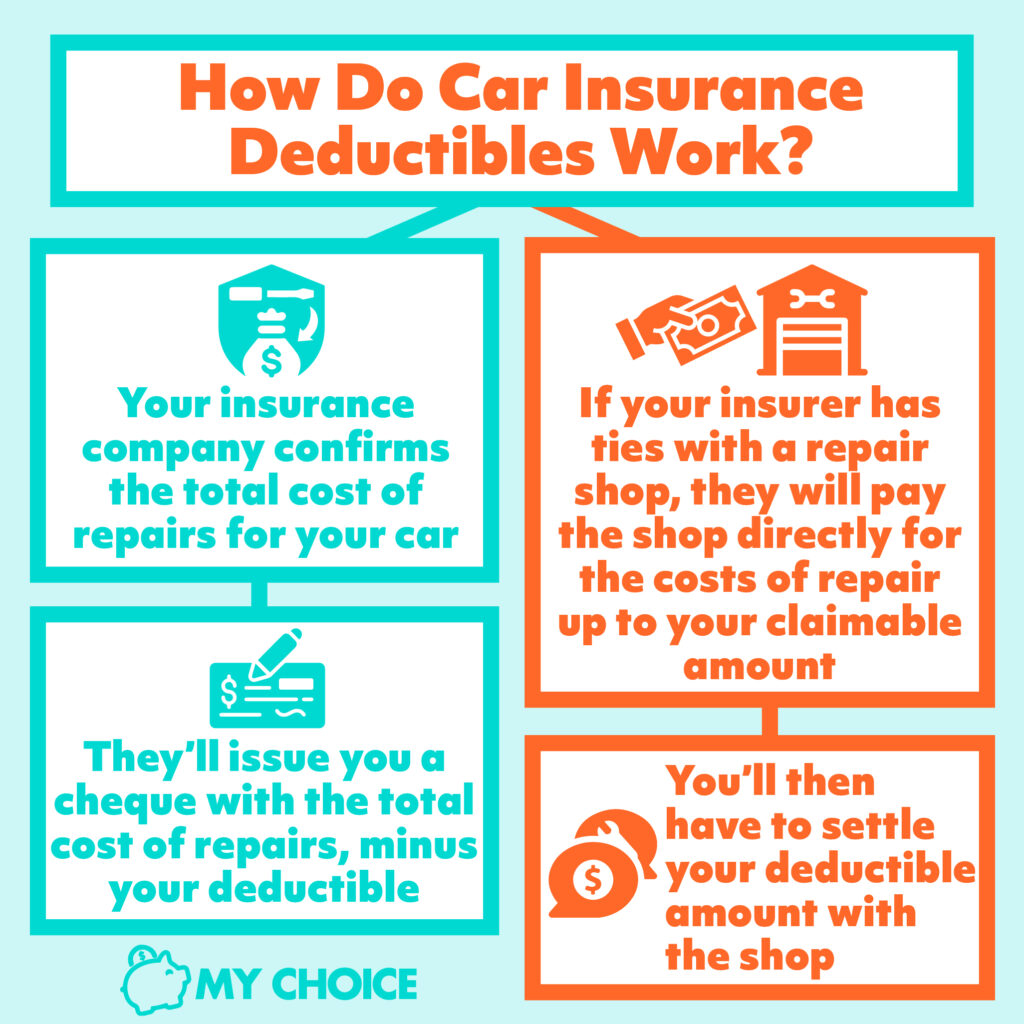

A deductible is a fundamental component of nearly every auto insurance policy, representing the amount of money a policyholder must pay out-of-pocket towards a covered claim before their insurance company begins to pay. It acts as a shared responsibility between the insured and the insurer, influencing both the cost of premiums and the financial implications of filing a claim. Understanding the deductible is crucial for managing personal finances and making informed decisions about insurance coverage in an increasingly complex and technologically driven automotive landscape.

The core purpose of a deductible is twofold: to reduce the number of small claims an insurance company has to process and to encourage policyholders to drive carefully, knowing they will bear some financial responsibility in the event of an accident or damage. By sharing the risk, insurers can offer lower premiums to policyholders, as their financial exposure per claim is reduced. Conversely, policyholders can often choose a higher deductible to lower their monthly or annual premium, trading a lower immediate cost for a potentially higher out-of-pocket expense if they need to file a claim.

The Foundational Role of Deductibles in Risk Management

Deductibles are not merely a number on a policy; they are a strategic tool in the actuarial science of risk management. For insurance companies, deductibles help to filter out minor incidents that would otherwise incur significant administrative costs relative to the payout. Processing countless small claims for minor dents or scratches, where the repair cost might only be a few hundred dollars, would quickly make an insurance company unprofitable. By setting a deductible, typically ranging from a few hundred to a couple of thousand dollars, insurers ensure that only claims exceeding a certain threshold are submitted, focusing their resources on more substantial losses.

This mechanism directly impacts how insurance premiums are calculated. When an individual chooses a higher deductible, they are signaling to the insurer that they are willing to accept more risk. In return for this increased self-insurance, the insurer reduces the premium, as their potential payout per claim is lower, and the likelihood of them paying anything at all for minor incidents decreases. Conversely, a lower deductible means the insurer takes on more risk, which is reflected in a higher premium. This delicate balance allows policyholders to tailor their insurance costs to their financial comfort level and risk tolerance.

Moreover, deductibles instill a sense of accountability in drivers. Knowing that a portion of the repair cost will come directly from their pocket can encourage safer driving habits and a greater sense of responsibility for their vehicle’s upkeep. This behavioral aspect indirectly contributes to a reduction in claims across the insured population, benefiting all policyholders through potentially more stable or lower average premiums over time.

Deductibles in the Age of Digital Transformation and Telematics

The traditional concept of a fixed deductible is undergoing significant evolution with the advent of advanced digital technologies and data analytics. The rise of telematics and Usage-Based Insurance (UBI) models is particularly reshaping how deductibles are understood, chosen, and applied in auto insurance.

Telematics and Personalized Risk Assessment

Telematics systems, often utilizing devices plugged into a vehicle’s OBD-II port or smartphone apps, collect real-time data on driving behavior. This data includes metrics such as speed, braking habits, acceleration, mileage, and even the time of day a vehicle is driven. Insurers leverage this granular information to create highly personalized risk profiles for individual drivers, moving beyond broad demographic categories.

In this data-rich environment, deductibles can become more dynamic and reflective of actual driving performance. For example, some UBI programs offer discounts on premiums or even on deductibles for consistently safe drivers. A policyholder who demonstrates exemplary driving habits over a period might qualify for a lower deductible at renewal, or in some innovative models, their deductible could even decrease over the policy term as a reward for continuous safe driving. Conversely, risky driving behavior, while not necessarily increasing a fixed deductible mid-term, could lead to less favorable deductible options or higher premiums at renewal. This shift allows for a more equitable distribution of risk, where those who drive safely are financially rewarded, directly impacting their deductible choices and costs.

AI-Driven Claims Processing and Expedited Deductible Application

Artificial intelligence (AI) is revolutionizing the claims process, leading to faster, more accurate assessments and a streamlined application of deductibles. Traditionally, claims adjusters would manually inspect vehicle damage to estimate repair costs and determine the deductible’s role. Today, AI-powered image recognition and machine learning algorithms can analyze photos and videos of vehicle damage submitted by policyholders, providing rapid and precise estimates.

This technology significantly expedites the claims cycle. AI can quickly compare damage estimates against the policy’s deductible, instantly informing the policyholder of their out-of-pocket responsibility. This transparency and speed reduce uncertainty for claimants and significantly cut down on administrative overhead for insurers. Furthermore, advanced AI models can detect fraud with greater accuracy, ensuring that deductibles are applied fairly and effectively, protecting the financial integrity of the insurance system for all policyholders.

Autonomous Vehicles and the Evolving Deductible Landscape

The impending widespread adoption of autonomous vehicles (AVs) introduces unprecedented complexities to auto insurance, fundamentally challenging traditional notions of liability and, by extension, the application of deductibles. As driving control shifts from human to machine, the question of who is responsible in an accident becomes far more intricate.

Shifting Liability and Deductible Responsibility

In a world dominated by AVs, accidents might no longer be solely attributed to driver error. Instead, liability could shift to the vehicle manufacturer, the software provider, or even the fleet operator. This paradigm shift directly impacts the concept of the deductible. If a fault lies with the vehicle’s autonomous system, should the vehicle owner still be responsible for the deductible? Or should the manufacturer, whose technology failed, bear that cost?

Insurance products for AVs are still in nascent stages, but it is clear that deductible structures will need to adapt. We might see new types of deductibles specifically for system failures, or perhaps manufacturers will offer guarantees that waive deductibles for incidents proven to be due to their technology. This evolving landscape could lead to a decoupling of the deductible from the policyholder in certain scenarios, placing the burden on the entities responsible for the autonomous technology itself. This will necessitate close collaboration between insurers, vehicle manufacturers, and regulators to define clear frameworks for liability and deductible application in this new mobility ecosystem.

Predictive Analytics and Proactive Deductible Design

Autonomous vehicles, by their nature, are equipped with a plethora of sensors, cameras, and sophisticated AI that constantly monitor their environment and internal systems. This technology generates vast amounts of data that can be used for predictive analytics to forecast potential failures or accident risks with extreme precision.

Insurers could leverage this data to implement proactive deductible designs. For highly autonomous vehicles that demonstrate an exceptionally low risk of accidents due to their advanced safety features and predictive capabilities, deductibles might be significantly lower or even structured differently. For example, a deductible might only apply in very specific, rare scenarios not covered by the vehicle’s inherent safety systems. The goal would be to reflect the dramatically reduced risk profile of these vehicles, potentially leading to a future where traditional high deductibles for collision or comprehensive coverage become less common for fully autonomous fleets. This futuristic approach to deductibles would be entirely data-driven, emphasizing prevention and the inherent safety provided by advanced driving technologies.

Choosing Your Deductible in a Technologically Advanced World

Selecting the right deductible remains a critical financial decision, even as technology transforms the insurance landscape. While the fundamental trade-off between premium cost and out-of-pocket expense persists, new technological integrations add layers of consideration for policyholders.

Balancing Risk, Technology Integration, and Personal Finances

Policyholders must continue to assess their financial capacity to pay a deductible if an incident occurs. However, in a world of telematics, their driving habits can now directly influence their deductible options or potential rewards. Engaging with UBI programs might offer pathways to lower deductibles over time for safe drivers, making higher initial deductibles more appealing. Conversely, individuals who recognize their driving habits might be riskier could opt for a lower deductible, accepting a higher premium but securing greater financial protection in a claim.

The integration of advanced driver-assistance systems (ADAS) in modern vehicles also plays a role. Features like automatic emergency braking or lane-keeping assist can significantly reduce accident frequency and severity. While these don’t directly change a fixed deductible, they lower the likelihood of needing to pay one, making higher deductibles a more viable option for some.

Future Trends: Dynamic Deductibles and Personalized Policies

Looking ahead, the evolution of technology points towards even more dynamic and personalized deductible models. Imagine a future where your deductible is not a static figure but one that adjusts based on real-time factors: traffic conditions, weather, or even how alert you are while driving (monitored by in-cabin sensors). In such a scenario, technology could proactively mitigate risk and adjust the deductible to reflect the immediate exposure.

Furthermore, blockchain technology could enable smart contracts that automate the entire claims and deductible process. Upon verification of an accident through tamper-proof data, the deductible could be automatically debited and the remaining claim paid out, offering unprecedented transparency and efficiency. This level of automation and personalization signals a future where deductibles are not just a static policy term but an intelligent, responsive component of a truly personalized auto insurance experience, deeply integrated with the vehicle’s technology and the policyholder’s behavior.